By Bill Hornbarger, Chief Investment Officer at Moneta

Looking at trailing returns through the end of Q3, equities had a remarkable decade. Using the S&P 500 as a benchmark, the stock market has an annualized return of 13.2% since the third quarter of 2009. Calendar year 2019 saw more of the same, with the S&P 500 gaining 20.6% through three quarters with most of that gain accumulated in the first half of the year. However, while the trailing returns are impressive and interesting, this information is of little use in making future decisions.

While we embrace strategic asset allocation and focus on building durable, goal-oriented portfolios unique to each client’s risk and return appetites and objectives, we do spend a significant amount of time looking at the investment environment and market valuations. Last month, we wrote about the challenge of persistent low bond yields and the very rich valuations of the bond market. This month, we take a quick look at equity valuations.

There are multiple ways to look at market valuations. As an allocator, we like to look at them in two different manners: relative to other investment options and relative to history.

Allocators think about how to choose which asset classes to invest in and to what degree. For the purpose of this discussion, we will just focus on stocks (the S&P 500) and bonds (the 10-year Treasury). While we all know stocks and bonds play different roles in portfolios, there are different ways to “compare” the two markets.

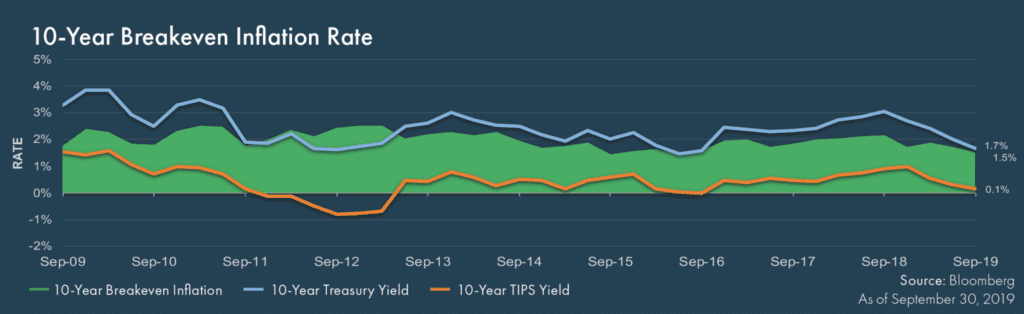

The so-called “Fed model” compares the yield of a fixed income instrument to the earnings yield of stocks (defined as the inverse of the price/earnings ratio). For much of the period from 1980 to 2002, the 10-year Treasury produced a higher “yield” than stocks (basis earnings yield, as previously defined). After the Tech Wreck, that relationship flipped and then widened in the wake of the Global Financial Crisis. While not at the widest levels, the differential between the earnings yield of equities suggests stocks are attractive relative to bonds (the current yield of the 10-year Treasury is 1.77% and the earnings yield of the S&P 500 is 5.2% using price/earnings ratio of 19.33). This is no surprise after a decade of extraordinary monetary policy.

One other measure currently suggesting equities are attractive relative to bonds is the fact that the dividend yield for the S&P 500 is higher than the 10-year Treasury yield. Historically, this is rarely the case. It is important to remember that these valuation metrics suggest nothing about absolute returns. They are just a way to evaluate markets relative to each other.

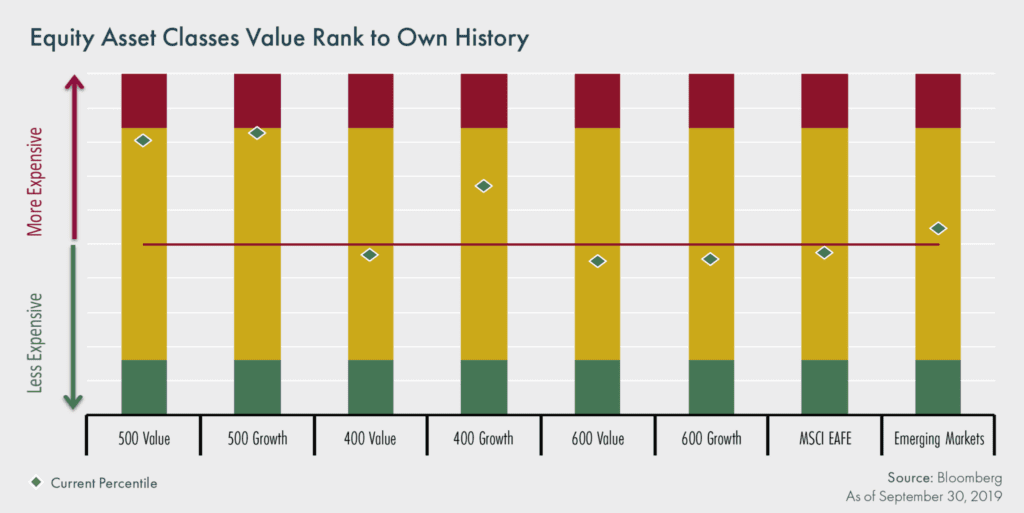

Many investors use the price/earnings ratio to evaluate how a market is priced relative to its own history and for some gauge of expected forward returns. When the P/E ratio is low, the market is considered less expensive and forward returns are expected to be better – and vice versa. Instead of just simply looking at the P/E ratio, we combine four equally weighted factors – price/earnings, price/book, price/sales and price/cash flow – and compare this metric for each market to its own history. When it is lower, forward returns for subsequent periods have historically been better and vice versa. Current valuations (see chart) show that after 10 years of a bull market and persistent outperformance of US large cap stocks, they are at a level we consider fully valued – with other market sectors less so.

Current valuations suggest the story remains unchanged. Equities remain attractive relative to bonds; international equities remain attractive relative to US stocks and large cap is expensive relative to other segments. For investors still in the accumulation stage, stocks continue to provide the best opportunity for returns in excess of inflation over the long term. However, after 10 years of better-than-average returns, it would not be surprising to see returns more muted for a period going forward.

Market Snapshot

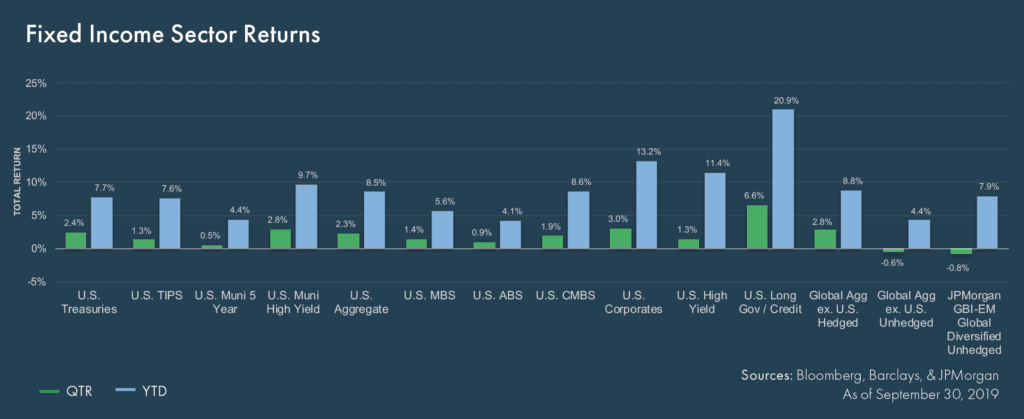

Fixed Income

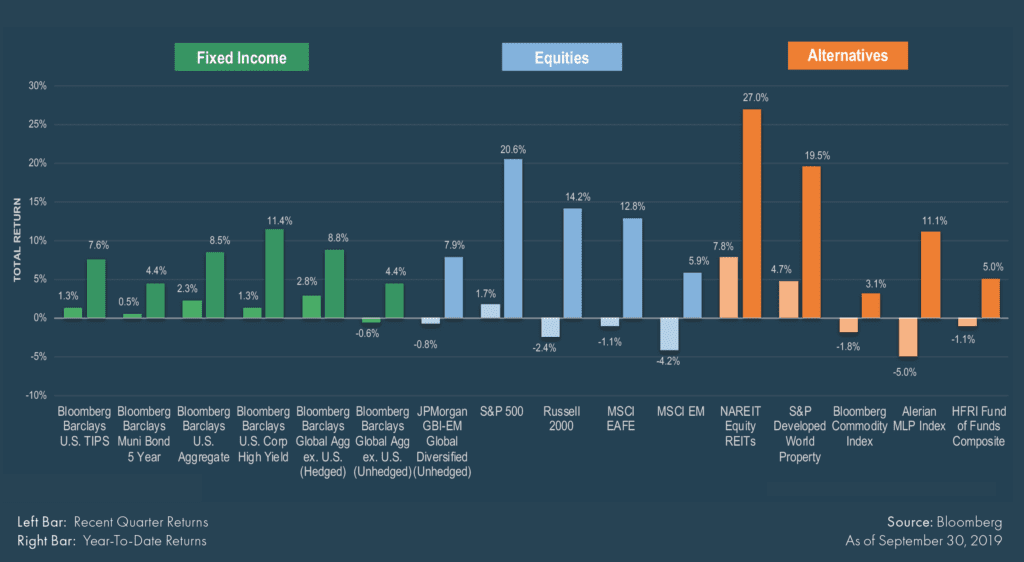

- Fixed income markets posted strong returns, led by international developed currency-hedged debt and longer-maturity U.S credit, which benefited from central banks loosening monetary policy and a broad appreciation in the U.S. Dollar.

- Investment grade credit and longer-dated bonds outperformed as central banks adopted more accommodative policies. The Federal Open Markets Committee (FOMC) cut the target Federal Funds rate by 25 basis points at its July and September meetings.

Equities

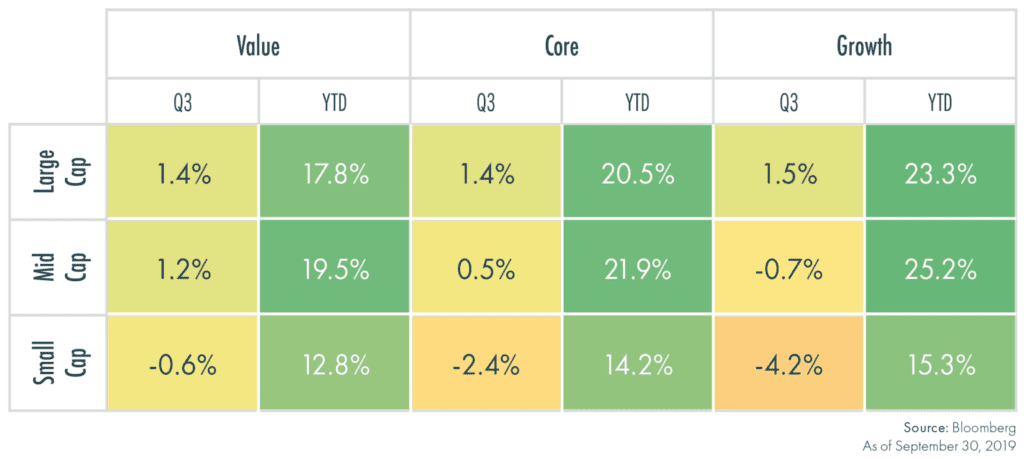

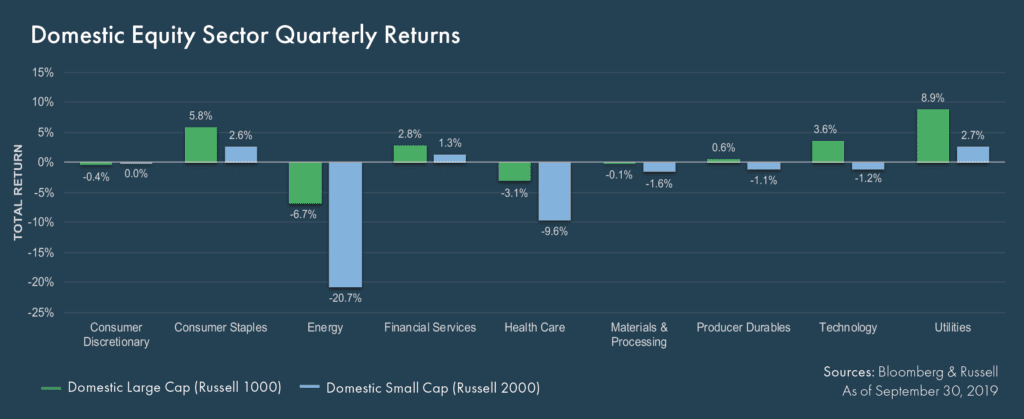

- Domestic equity markets generated positive returns during the quarter with large cap outperforming mid and small cap stocks. Value stocks broadly outperformed growth stocks except within large cap, where growth modestly outperformed value equities.

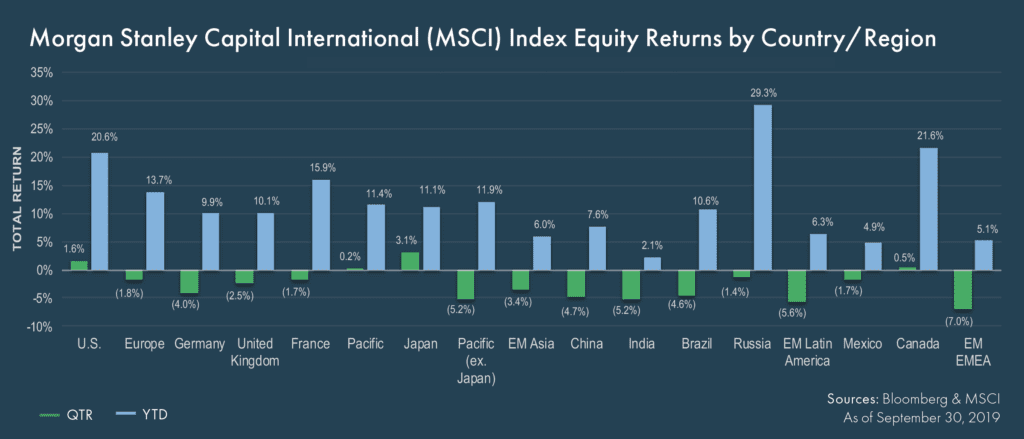

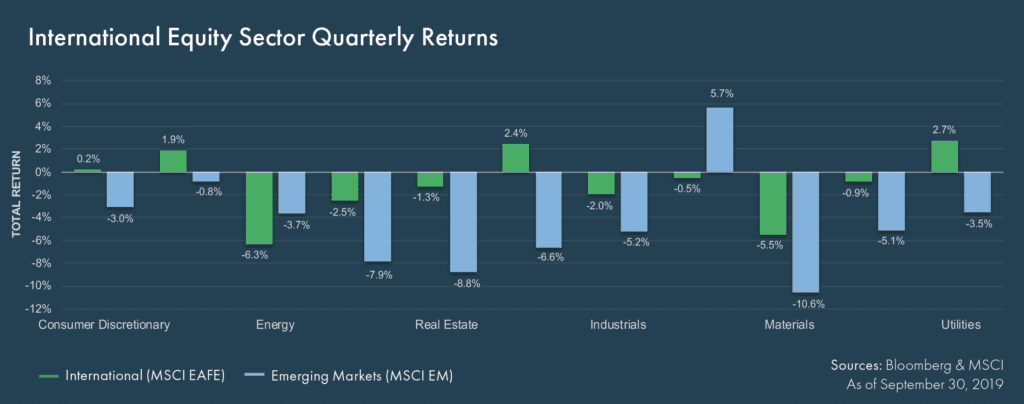

- International developed equities declined during the quarter but outperformed emerging market equities. Argentinian equities generated the worst returns within emerging markets followed by South African and Polish stocks.

Real Assets

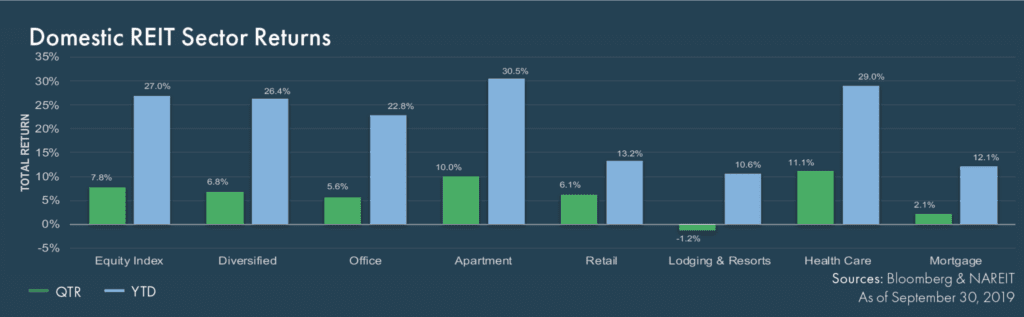

- Real assets posted mixed returns for the quarter. REITs increased sharply, benefiting from falling interest rates and strong fundamentals, while MLPs and energy-related assets underperformed during the quarter.

- Domestic REITs outperformed international, driven by strong returns in the healthcare and multi-family residential sectors.

- Hedge funds declined during the quarter, underperforming equities, fixed income and REITs while outperforming MLPs.

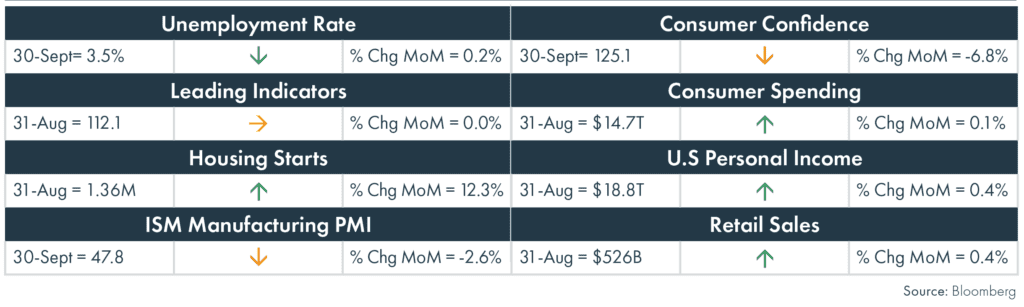

U.S. Economic Update

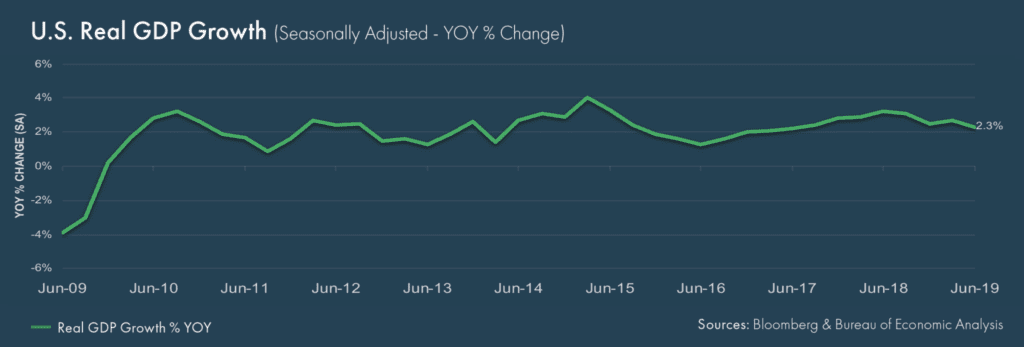

- Second quarter real Gross Domestic Product (real GDP) increased at an annualized rate of 2.0% on a quarter-over-quarter, seasonally-adjusted (QoQ, SA) basis according to the Bureau of Economic Analysis, a decrease from the 3.1% growth rate realized in the first quarter.

- The FOMC voted to cut its benchmark interest rate by 25 basis points at its July and September meetings, lowering the target Federal Funds rate to a range of 1.75% to 2.00%. In September, the Federal Reserve (“Fed”) began a series of interventions in short-term funding markets; the Fed repeatedly injected liquidity into the U.S. repurchase (“repo”) market to ease a cash shortage caused by dwindling bank reserves in the financial system.

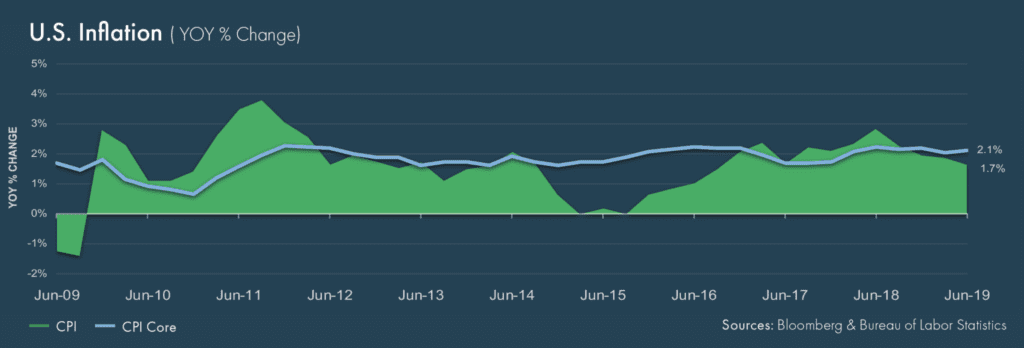

- The Core Consumer Price Index (CPI) rose 2.4% on a year-over-year, seasonally-adjusted (YoY, SA) basis in August while Core PCE, the Fed’s preferred measure of inflation, increased 1.8% (YoY, SA) in August, falling short of the Fed’s 2.0% target.

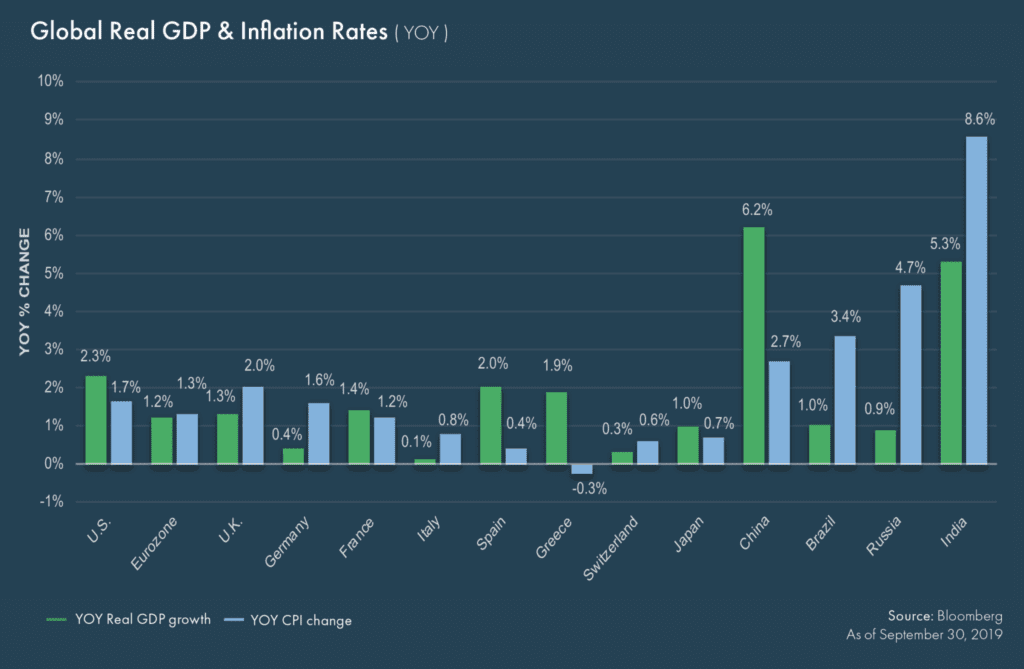

Global Economic Update

- China’s official Manufacturing Purchasing Managers’ Index (“PMI”) increased to 49.8 in September from 49.5 in August; the reading below 50 still indicated a contraction in China’s manufacturing sector. The unofficial Caixin/Markit Manufacturing PMI, a private survey focused more on small-and medium-sized businesses, increased to 51.4 in September from 50.4 in

August, largely driven by increased domestic demand. The U.S. and China failed to make substantive progress in trade negotiations during the quarter. - Second quarter real GDP increased at a 0.8% annualized rate (QoQ, SA) in the Euro Area, marking a significant decline in growth relative to the first quarter amongst a clouded economic backdrop. Germany, the Europe’s largest economy, continued to exhibit signs of weakness as its real GDP contracted at an annualized rate of 0.3% (QoQ, SA). German manufacturing orders declined 2.1% on a month-over-month, seasonally-adjusted basis (MoM, SA) in July and another 0.6% (MoM, SA) in August.

- The European Central Bank (“ECB”) maintained its main refinancing operations interest rate at zero and lowered the rate on its deposit facility by 10 basis points to -0.5% at its September meeting. The ECB also announced the continuation of asset purchases indefinitely in the amount of €20 billion per month in an effort to further stimulate economic growth.

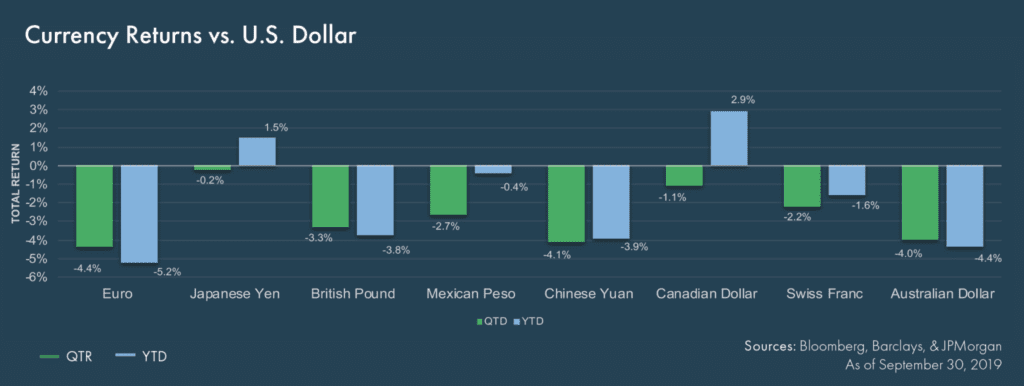

Global Fixed Income

- The FOMC cut rates following its September meeting to a target rate of 1.75% to 2.00%. The Fed cited slowing global growth and below-target inflation as justification for lowering rates.

- Falling interest rates led to positive performance across the majority of global fixed income indexes. Investment grade and longer duration assets generally outperformed riskier assets.

- The dollar rallied sharply across global currencies during the quarter. Despite the implementation of an asset purchase program by the ECB, the euro fell by 4.4% relative to the dollar.

U.S. Fixed Income

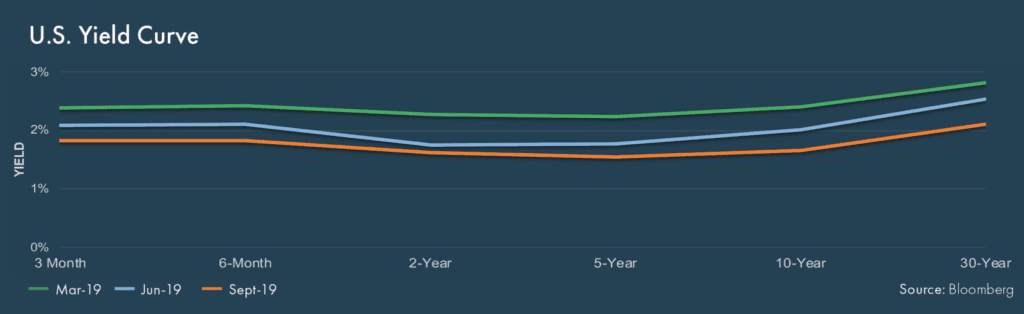

- Interest rates fell as the FOMC lowered its target rate, with the 10-year Treasury falling to 1.66% from 2.01%. Treasuries outperformed TIPS during the quarter as breakeven inflation rates fell to 1.50%.

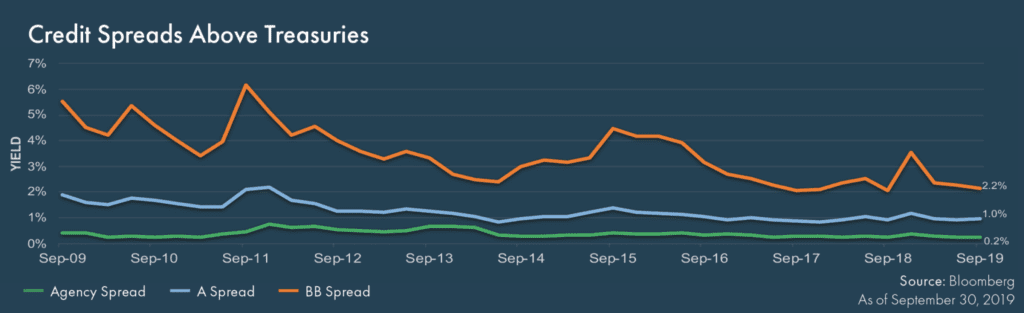

- Investment grade outperformed high yield assets, though high yield spreads continued to generate positive returns as

investors continue to search for yield. - Short-term money markets dislocated for the first time since the financial crisis as repo rates spiked to as high as 10% on September 17. The New York Fed responded by injecting more than $100 billion into short-term lending markets through the last two weeks of the quarter.

Global Equity Markets

- Within U.S. equities, the utilities and consumer staples sectors were the top performers while energy and healthcare were the worst performing sectors for the second quarter in a row. Large cap growth stocks slightly outperformed large cap value stocks, while value stocks outperformed growth stocks across the mid and small portions of the market capitalization spectrum. Large cap equities outperformed mid cap stocks, which outperformed small cap equities, across all investment styles.

- International stocks declined during the quarter, failing to keep pace with domestic stocks. Belgian and Japanese equities generated the strongest returns in developed markets while stocks in Hong Kong, Singapore and Germany underperformed.

- Emerging market equities lagged international developed markets during the quarter. Turkish, Egyptian and Taiwanese stocks generated the strongest returns in emerging markets while stocks in Argentina, South Africa and Poland generated the worst returns.

Quarterly Equity Sector Returns

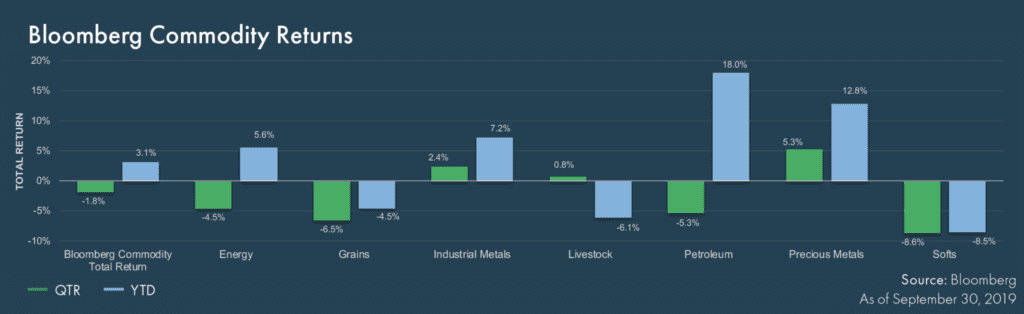

Real Assets

- Real assets finished the quarter mixed as REITs outperformed and energy-related assets lagged.

- Within commodities, oil fell despite a drone attack targeted at Saudi production facilities. While there was significant short-term turbulence following the event, production was restored more quickly than expected, creating less disruption in the global marketplace than initially expected.

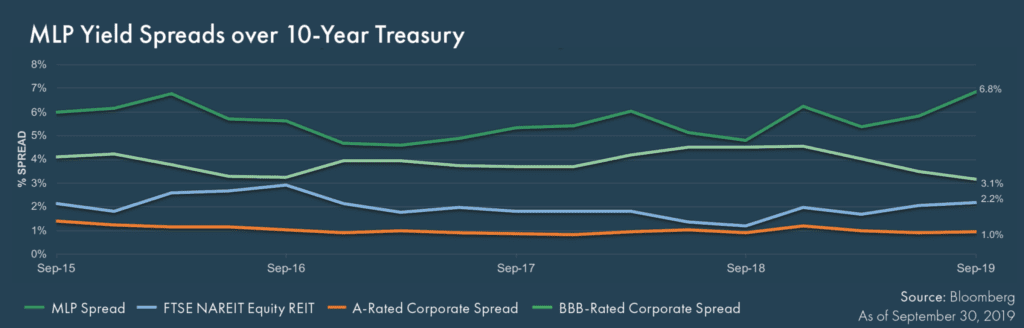

- The Alerian MLP Index largely moved in step with energy markets, declining 5.0% for the quarter. The price decline, in addition to continued EBITDA growth and declining fixed income yields, has resulted in the highest spread to Treasuries in over three years.

- REIT sectors rose sharply as declining bond yields, continued rent growth and limited supply were all beneficial. Healthcare and multi-family outperformed.

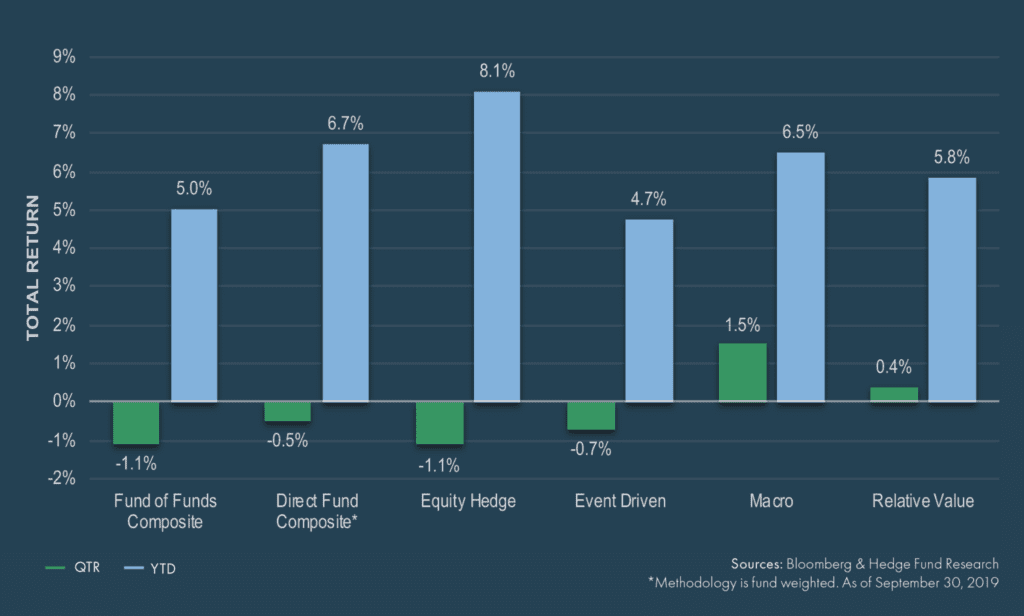

Hedge Funds

- The HFRI Fund Weighted Composite Index was slightly negative during the third quarter, underperforming fixed income indices but outperforming most equity indices.

- Equity Hedge strategies underperformed the broader hedge fund universe, with strong returns concentrated in market-neutral strategies and negative returns in growth-oriented strategies.

- Event Driven strategies were in-line with the broader hedge fund universe, with merger arbitrage and multi-strategy managers leading the group while special situations and distressed funds trailed the benchmark.

- Similar to the second quarter, Macro strategies were the strongest performer among the broader hedge fund universe as systematic, multi-strategy and currency managers all posted strong returns.

- Relative Value strategies outperformed the broader hedge fund universe, with fixed income asset backed and fixed income convertible arbitrage managers posting the strongest gains.

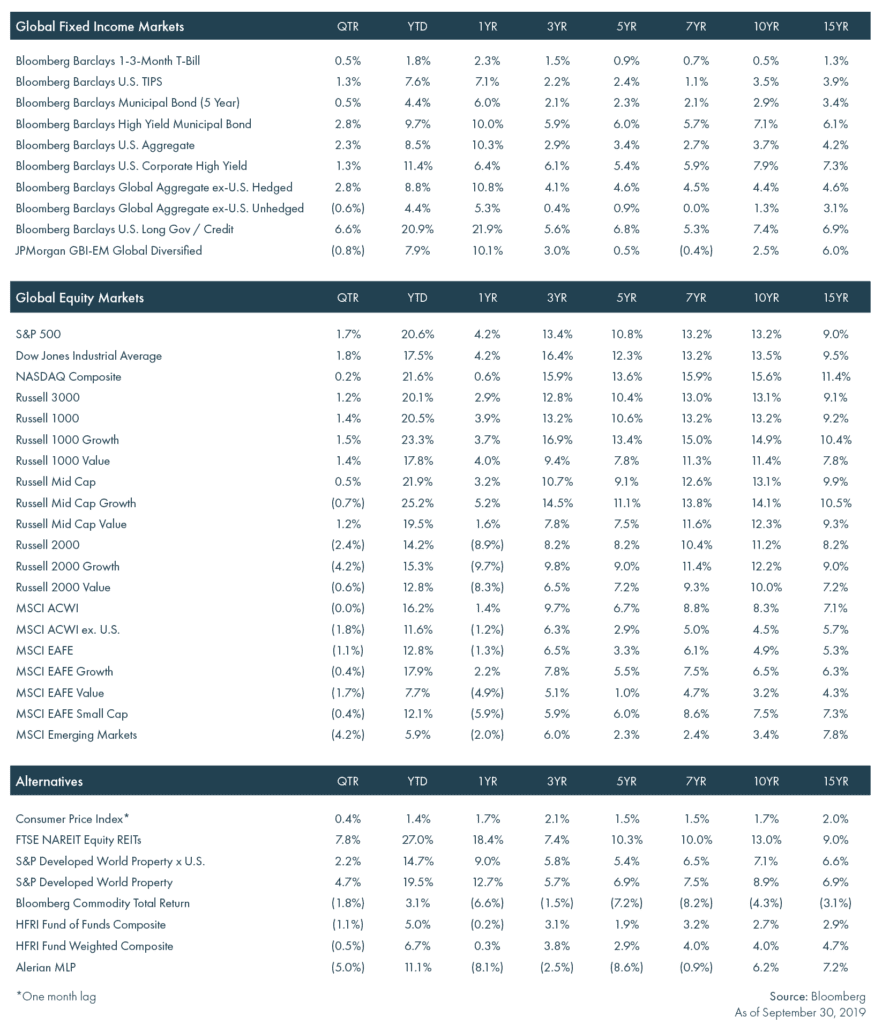

Financial Market Performance

Periods greater than one year are annualized. All returns are in U.S. dollar terms.

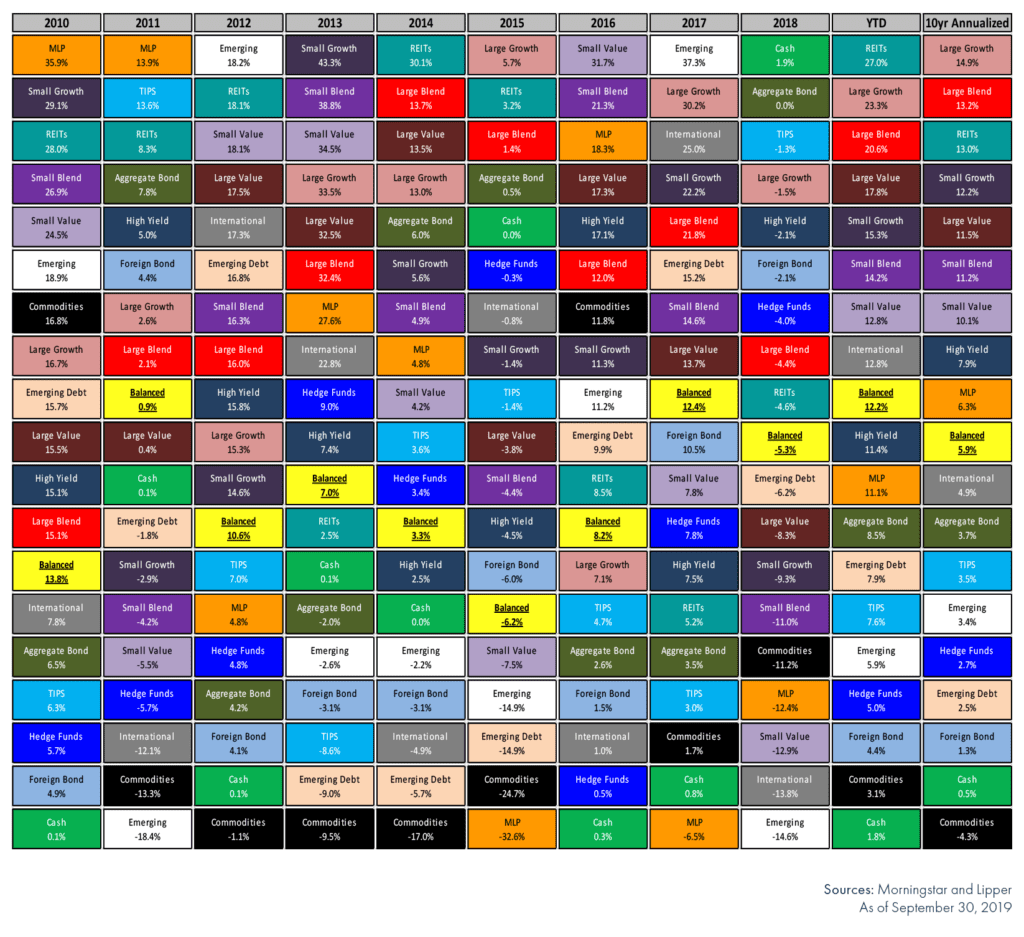

Why Diversify

Year-by-year performance rankings of asset classes:

© 2019 Moneta Group Investment Advisors, LLC. All rights reserved. These materials were prepared for informational purposes only. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. Past performance is not indicative of future returns. These materials do not take into consideration your personal circumstances, financial or otherwise.