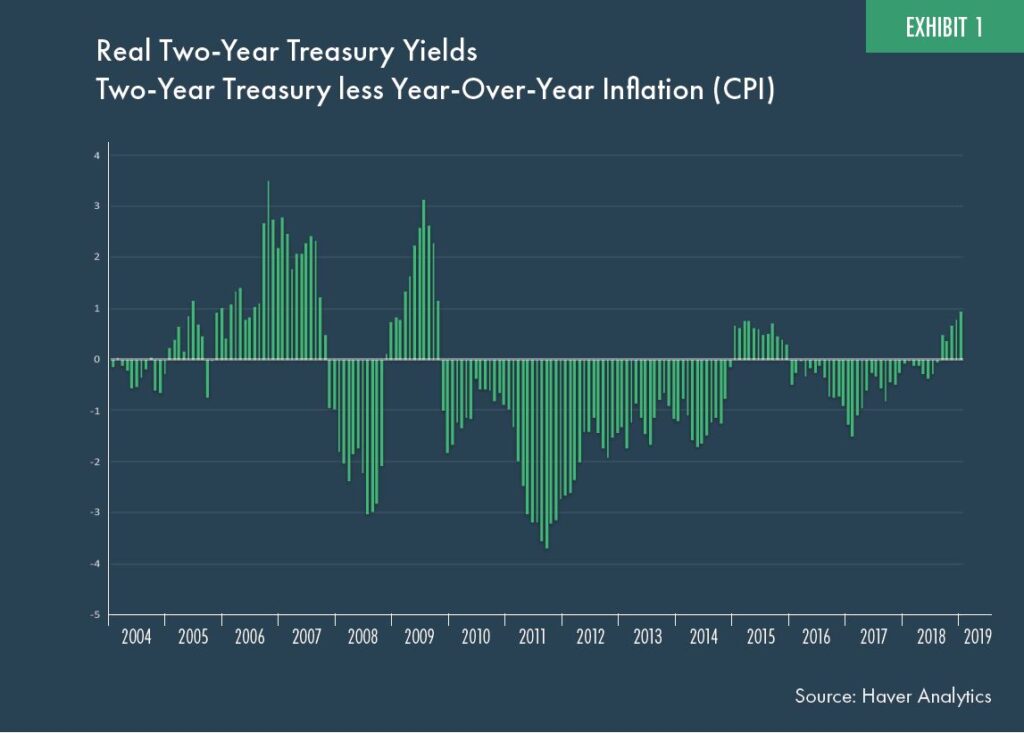

On December 16, 2008, the Federal Open Market Committee lowered the target Fed funds rate to 0% and this important financial market bellwether remained at that level for seven years. During that same period of time, the benchmark two-year Treasury bond yield averaged 0.54% and fluctuated between a high of 1.40% and a low of just 0.16%. During that span, the average real or inflation adjusted basis of the two-year Treasury was negative 0.83% as the Fed pursued extraordinary monetary policy in an effort to spur an economic recovery in the wake of the Global Financial Crisis (see Exhibit 1).

During that same period of very low bond yields, correlations across many of what are considered “riskier” asset classes (i.e. real estate, international vs. domestic equities, value vs. growth equities) increased at a time (post the Global Financial Crisis) that investors desired diversification in general and equity market risk mitigation in particular.

In response to this persistent and challenging investment environment, investors turned to alternative investment solutions and strategies seeking to augment portfolio returns in the wake of historically low bond yields and increased risk in the form of heightened correlations. Hedge fund strategies such as long-short equity and trend following became more readily available to individual investors in the form of 1940 Act registered mutual funds as opposed to the traditional limited partnership structure with very high investment thresholds. In 2015, the liquid alternative segment (1940 Act registered mutual funds) was one of the fastest growing areas of the market with more than 600 funds in the universe and reported net inflows totaling $6.5 billion for the calendar year.

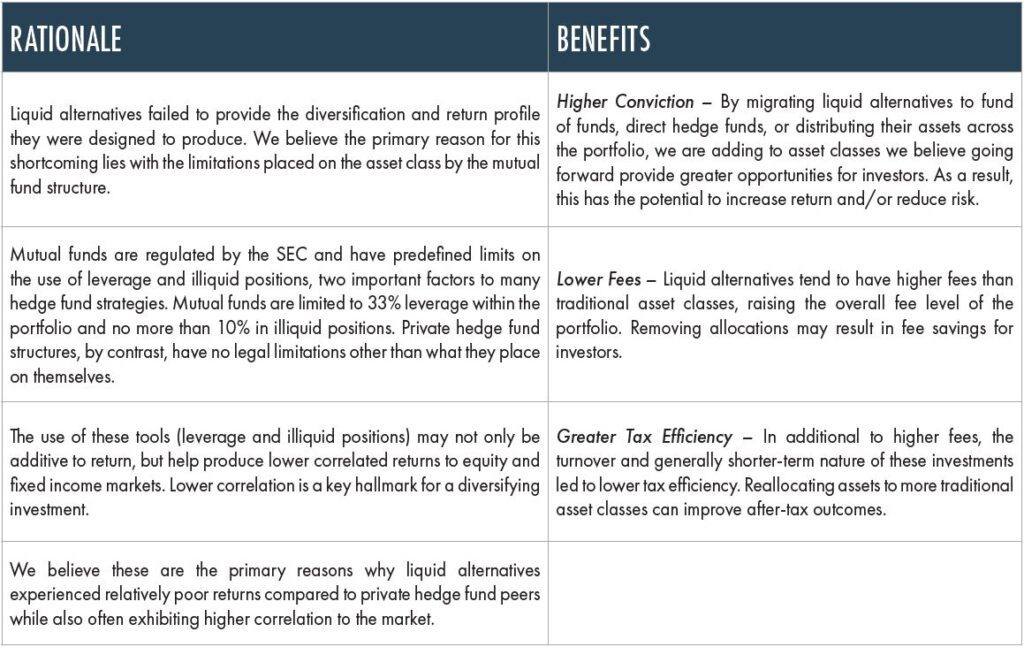

The most recent period has been a difficult time for most alternative strategies regardless of structure, and liquid alternatives in particular have not provided the expected returns or diversification benefits that they were designed to produce. Morningstar’s liquid alternatives peer groups have underperformed their comparable hedge fund indices with underperformance during the last five years (ending December 2018) ranging from -0.8% to -2.4% depending on the category. As a result, net flows reversed course for liquid alternatives, with net outflows of $26.4 billion during the past three years and the number of funds shrinking to approximately 500 at the end of 2018.

At the same time, overall market conditions have evolved. Cash and short-term bond yields increased from 0% to more than 2% and projected returns changed across asset classes. Investors also desire simplicity, and investment expenses are now a greater focus.

In response to these changes in the markets and after a thoughtful and deliberate analysis of all available options, we decided on the following: Plan to transition from liquid alternatives and reallocate assets throughout the portfolio or to other higher conviction alternatives to maintain a similar risk profile.

In making this recommendation, we want to stress that the assets in these strategies are not in any peril, but that with bond yields higher and managers unable to fully execute their strategies in a mutual fund structure, the desired portfolio attributes can be achieved in other, higher conviction asset classes.

In summary, the investing landscape has changed and the recommendation is made based on the following:

- Bond yields increased, particularly on cash and short-term instruments.

- Liquid alternatives have not provided the expected returns or diversification benefits.

- Investors desire simplicity.

- Markets evolved and projected returns changed across asset classes.

- Investment expenses compressed and have a more heightened focus.

© 2019 Moneta Group Investment Advisors, LLC. All rights reserved. These materials were prepared for informational purposes only. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. Past performance is not indicative of future returns. These materials do not take into consideration your personal circumstances, financial or otherwise.