by Chris Jordan, Director of Alternative Investments

With a seemingly endless supply of ominous global economic news, investing in gold has grabbed much of the media’s and investors’ attention. Many investors have become mesmerized by the luster of profit and safety. But are the touted expectations too lofty, only a sales pitch, pure sensationalism or are they reasonable? What are the risks and rewards associated with gold investments? Our intention in this article is to provide an unbiased perspective on gold built on an analysis of actual performance. The goal is to help manage expectations and to provide insight allowing investors to decide if gold is a worthy participant in a diversified portfolio.

Gold as a total return investment. Since the early 1970s when the United States dollar left the gold standard, gold has provided investors with significant return. Since August 1971, when President Nixon ended the direct convertibility of dollars into gold, the price of gold has appreciated from $42.73 to $1,282.55 per ounce (as of 7/31/2014). The appreciation is equivalent to an 8.2 percent annual return. Not bad considering the S&P 500 appreciated 10.5 percent (annualized return, assuming all dividends were reinvested) and inflation (CPI-Urban Consumer) was effectively 4.2 percent over the same time period. How dependable should a potential gold investor view these historical returns?

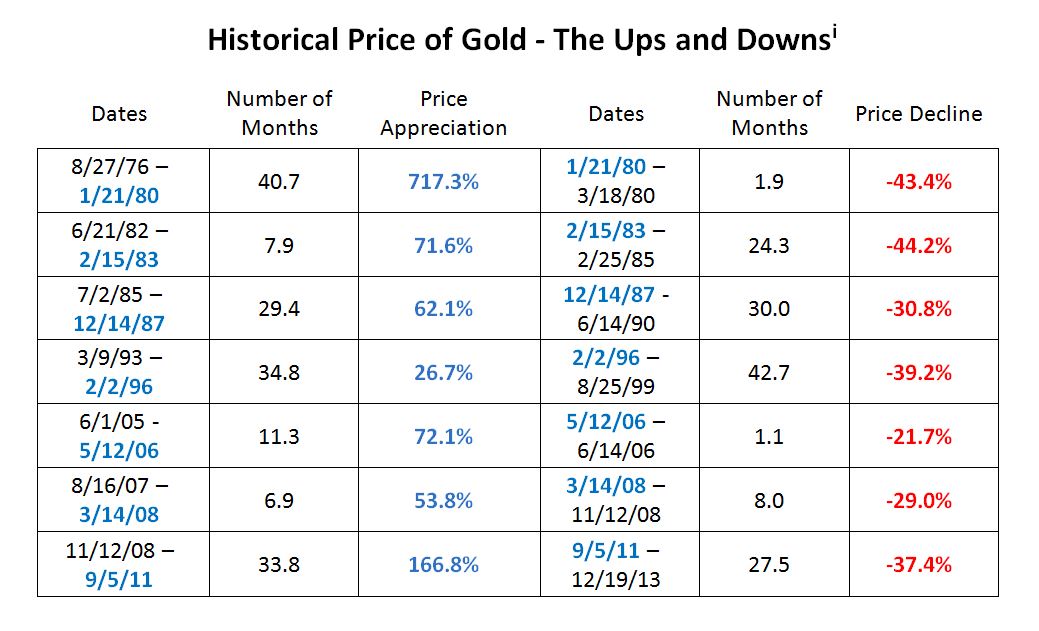

Since gold has very limited real economic value/demand (except for jewelry and very few industrial applications), its price is largely driven by speculation and fear.Historically, large price appreciations were associated with fears of high inflation, a declining dollar or stressed market conditions. Once these fears subside, even modestly, the price of gold could plummet abruptly, as it often has. Consider the following data:

If an investor was fortunate—or lucky enough—to time the gold market perfectly, he/she could have achieved impressive returns. Caution! As the table above illustrates, each run-up was followed by a significant decline. Unfortunately, many investors buy gold far too late into its ascent, fail to achieve outsized returns, and then fall victim to the sharp decline.

It is true that long-term investors (over 40 years) would have enjoyed a very respectable return. However, the journey was far from smooth. Even when compared to the stock market, gold has been riskier. For example, the volatility of gold since August, 1971, has been 31 percent higher than that of the S&P 500total return index. Additionally, the maximum drawdown (potential compounded loss) was much larger as well, -61.7 percent versus -50.9 percent respectively.

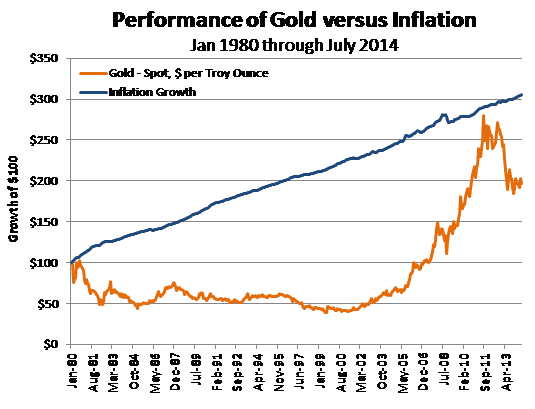

Gold as an inflation hedge. For many investors, it is a foregone conclusion that gold is a good inflation hedge. And during many periods in the past, gold performed exceedingly well when the fear and realized inflation were high. For example,in the mid to late 1970s, gold reached levels of annual appreciation of 30 to 150 percent when inflation reached close to 15 percent. However, it isn’t widely known that since 1971, gold’s price appreciation beat inflation (U.S.CPI Urban Consumers) only 53 percent of the time (any 12-month period). In other words, in any given year there was only a ‘coin flip’ chance an investment in gold would have maintained an investors’ purchasing power.

The following chart demonstrates how gold has under performed inflation for an extended period of time. It shows how the value of $100 dollars invested in gold would have performed versus $100 (as of 1980) appreciating at the rate of inflation. The beginning of the chart was the peak gold price in early 1980 (record high at that time).

Amazingly, even though gold has performed remarkably since mid-2001, it has yet to catch up with the $100 adjusted for inflation since 1980.

Gold in a diversified portfolio. Another widely believed ‘truth’ about gold is that it will provide your portfolio sharp positive returns if the capital markets are stressed. Similar to gold’s inflation protection, gold does indeed provide diversifying qualities on occasion. But there have been many occasions in the past where it unquestionably did not provide diversifying support.

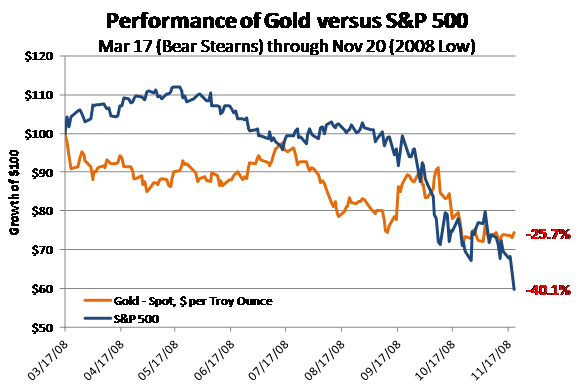

For example, in those months when the S&P 500 lost more than 5 percent in total return(considered stressed for this discussion), gold provided a positive return on average (+1.1 percent). Unfortunately, gold produced positive returns in stressed equity markets less than two-thirds of the time. The other third of the time gold also lost money (with the S&P 500). A recent example of this was the period from March, 2008, (Bear Stearns collapse) through late fall of 2008 (Lehman and credit market debacle). The chart below shows the compounded loss of the S&P 500 (including dividends) as compared with the compounded loss of gold.

In today’s environment, gold could very possibly provide an investor a phenomenal return if the global capital markets experience extreme turbulence and losses (e.g.collapse of the dollar). This would suggest that the remaining assets in the investor’s portfolio will likely decline very dramatically. To offset these losses, the necessary allocation to gold would have to be very large—imprudently large. A portfolio grossly over-weighted in any asset class or strategy is exposed to a tremendous amount of risk and/or underperformance. This is especially true of investments that historically have been highly volatile.

Conclusion

In the past, investing in gold has provided investors outstanding results—at times. Unfortunately, it has also damaged fearful investors permanently. It is our belief that a truly diversified portfolio is the best weapon for defending against the known and unknown market risks,and increases investors’ odds of reaching their desired financial destination. Anxiety and fear of what is possible, rather than what is probable, can be paralyzing and, in the long-run, very crippling to one’s financial security.

[i]Source: Bloomberg, Gold spot price as US Dollar per Troy ounce