We often hear people say life insurance isn’t a very good ‘investment.’ When you think of life insurance in the context of wealth accumulation, insurance really should not be considered an investment vehicle. So what purpose does it serve? Life insurance is perhaps one of the most effective wealth transfer vehicles and planning tools.

Let’s try to demystify what life insurance really is. Whole Life, Universal Life, Modified Endowment Contracts, Quick Pay, Level Term, Vanishing Premium, Indexed Life, Variable Life, Accumulation Universal Life, Secondary Guarantee Life are all buzz words and product types used in the sale of life insurance. This jargon can be very confusing and muddy the waters as to what is really important.

Let’s set the jargon aside and take a look at the economics of life insurance and how this can be an effective tool for wealth transfer.

For the average person or even moderately affluent individual, paying large life insurance premiums represents an expense and a choice between committing to a wealth transfer strategy for the next generation, or generations to come, and enjoying the money themselves for current lifestyle desires. However, for many of our clients, the decision is really about how to best invest the excess funds that are currently includable in their estate. For these people, funding insurance as part of a wealth transfer strategy does not typically infringe upon their current lifestyle; therefore, it becomes a very emotionless decision.

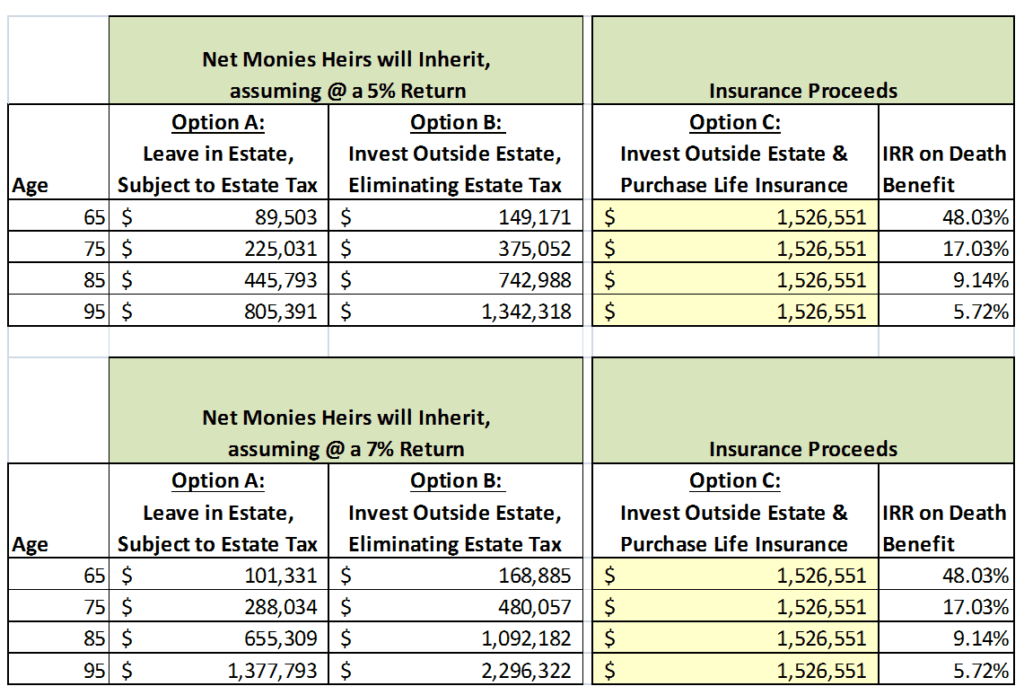

If one has sufficient money to maintain their current lifestyle, the question then becomes what do you do with the excess dollars beyond what is used to meet your needs? If your goals include transferring wealth to the next generation, or even funding charitable commitments, life insurance might be the answer. Let’s imagine we have a 55 year old couple with $10,000 of ‘excess cash’ each year to be invested. For illustrative purposes, let’s assume that the clients have a growing estate above the estate tax exemption limit. They are faced with the several options, including the following, for investing their excess monies:

- Option A: Do nothing, and simply let the excess funds compound inside one’s estate and likely be subject to taxes on amounts above the estate tax exemption limit.

- Option B: Employ one of many estate planning techniques to ‘freeze’ the current value of one’s estate and invest the excess funds outside of the estate.

- Option C: Take these excess dollars and use them to purchase (invest in) life insurance utilizing an Irrevocable Life Insurance Trust (ILIT).

The Math

The charts below show the impact of deploying this $10,000 annual investment in the three strategies mentioned above:

The top chart shows a 5% return on the investment and the bottom shows a 7% return on the investment.

As you will see, insurance can be an extremely effective hedge in your wealth transfer planning and it is highly unlikely you will find anything as effective.

Some of the wealthiest and most affluent people purchase enormous life insurance policies because to them, it’s just like moving pieces around on a chess board. Once you stop looking at the premium component as a cost, but view it as a part of your wealth transfer strategy, you are able to look at this strategy objectively and insurance compares very favorably.

Life Insurance as an Asset Class

Life insurance has a dynamic ability to serve as one of the best hedges in your portfolio. Looking inside a 20-25 year investment time horizon, insurance can serve as an attractive and viable financial option that, on a guaranteed basis, can provide a rate of return that can meet or exceed the rate of return of other investments (for example, in the above illustration, insurance yielded a rate of return of 13%-18%).

If you happen to live beyond this, you have bought yourself more time to allow the other investments in your portfolio the time they need to have stronger performance, and you will be that much better off.

Here is another way to think about insurance: put simply, taking some of your bond portfolio to purchase life insurance just might result in a return that is several times greater than the return that your bond portfolio will produce. For example, a 30-year treasury bond today is yielding 2.94%, which is significantly lower than the internal rate of return of a life insurance policy after 30 years (9.14%, as shown). Conceding to the fact that we are in a low fixed income interest rate environment today, and even when we consider that the historical 30 year average of a treasury bond is 6.05%, these returns are significantly lower than the internal rate of return on the life insurance policy. Let’s be honest with ourselves and admit that we’re not all going to live to be 100 years old. If you die between 70-85 years old, then your rate of return on life insurance is going to be between 10-30%.

The Benefits

There are many additional benefits to investing in life insurance. Life insurance is less risky than other asset classes. In the event of an untimely death, life insurance offers immediate liquidity, which means that if your family needs money, they do not have to disrupt other investments that are less liquid by cashing them out and potentially incurring penalties or taxes. Liquidity from insurance just might give other investment strategies time to perform and maximize returns in other areas of your portfolio.

In addition to liquidity, life insurance proceeds (if owned properly) are income and estate tax free, creditor proof, and divorce proof.

So, don’t be distracted by the jargon; instead, talk to your Family CFO to help sort through these issues and determine if life insurance belongs in your portfolio.

Disclaimer: It is important to note that the quoted rates above are based on a survivorship life insurance policy and are used simply for illustration purposes. Actual rates and policy terms are subject to underwriting and will vary by product.