Quarterly Letter

The country hit, People are Crazy, was written by two musicians trying, over drinks, to think of three things you cannot argue about. Our guess is there are some who may argue over the first two, but not the last. At times, people truly are crazy. In today’s modern world every foolish thought, utterance or performance is on full display thanks to the internet and modern communication. It makes one pine for simpler days of black and white television and a telephone with an attached cord.

Against the backdrop of such a world, however, economic news remains a bright spot. Both stocks and bonds are enjoying strong returns year-to-date. Even September, historically the worst month for stocks, recorded impressive gains. Capping it off, one could almost picture Fed Chair Jerome Powell as a modern-day Moses, complete with tablets, walking to the podium in late September to announce a 50-basis point (one-half percent) interest rate cut.

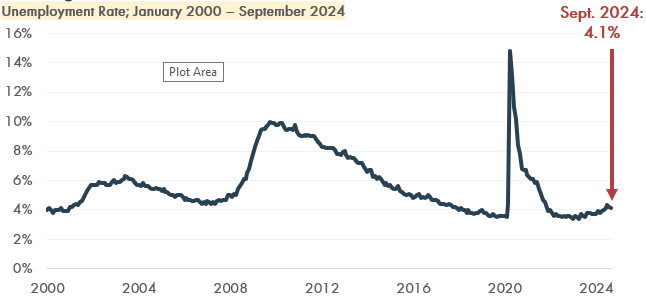

That announcement confirmed what most suspected. The Fed is recalibrating, believing they have been successful in reducing inflation close enough to their two percent target. (One only hopes they are not premature in declaring victory.) Apparently, the new focus is to be on the weakening employment side of their mandate with the goal being to keep the unemployment rate close to 4.0 percent, historically regarded as full employment.

The primary index for large U.S. stocks, the S&P 500 Index, reflects the good news. It is now up close to twenty percent year-to-date, and currently trades around twenty times next year’s projected earnings. That is on the high side of a comfortable range for stocks, but not scary-high. It is probably about right if the Fed continues to reduce short-term interest rates over the winter, as most suspect. Importantly, the stock market, driven significantly by companies embracing technology and artificial intelligence (AI) in recent quarters, has over the past several months rotated more into defensive or value names. This broadening of the market bodes well for upcoming quarters.

As we write this, the closing days of the U.S. Presidential election cycle approach. Does it matter to the markets who wins? While the brain says yes, the data says no. We cannot help but note our concerns over policies of both candidates. Both seem to have what we call economic amnesia, and what the Wall Street Journal editorial page recently termed economic illiteracy.

Fortunately, if the polls are correct, continued gridlock has a good chance of being the real winner in November. In other words, neither side will likely receive more than a small portion of their wish list. That is probably what markets would prefer. Indeed, historical studies confirm that the U.S. stock market can do just fine under any administration. Businesses adapt quickly to changing landscapes.

Given that we know people are, at times, a little crazy, and that there is a lot going on in the coming weeks, what should we expect for the fourth quarter of 2024 and beyond? Unfortunately, our crystal ball, which works so well in the long-term, is pretty foggy about the short-term. Unexpected events can, and do, create short-term havoc from time-to-time. Thus, we would be happy to let the stock market consolidate some of its recent gains; treading water for a time, if you will. Nonetheless, we will stay fully invested. Fidelity great, Peter Lynch, put it best when he said, “The real key to making money in stocks is not to get scared out of them.”

In other words, neither side will likely receive more than a small portion of their wish list. That is probably what markets would prefer.

Market Commentary

– Randal Stauder, CFA – Portfolio Strategist

After a period of volatility early in the third quarter, markets stabilized and rebounded with the Federal Reserve’s long-awaited rate cut in September. It has been a strong year for investors with all major stock, bond, and commodity indices posting positive returns.

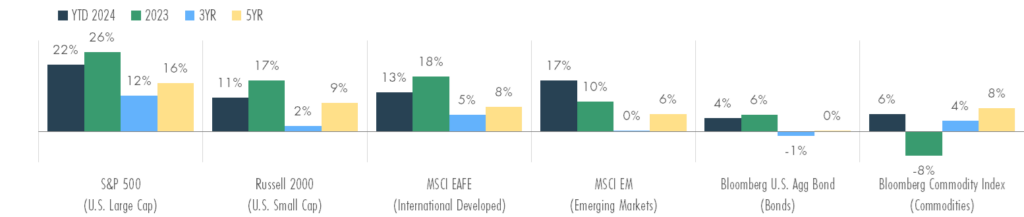

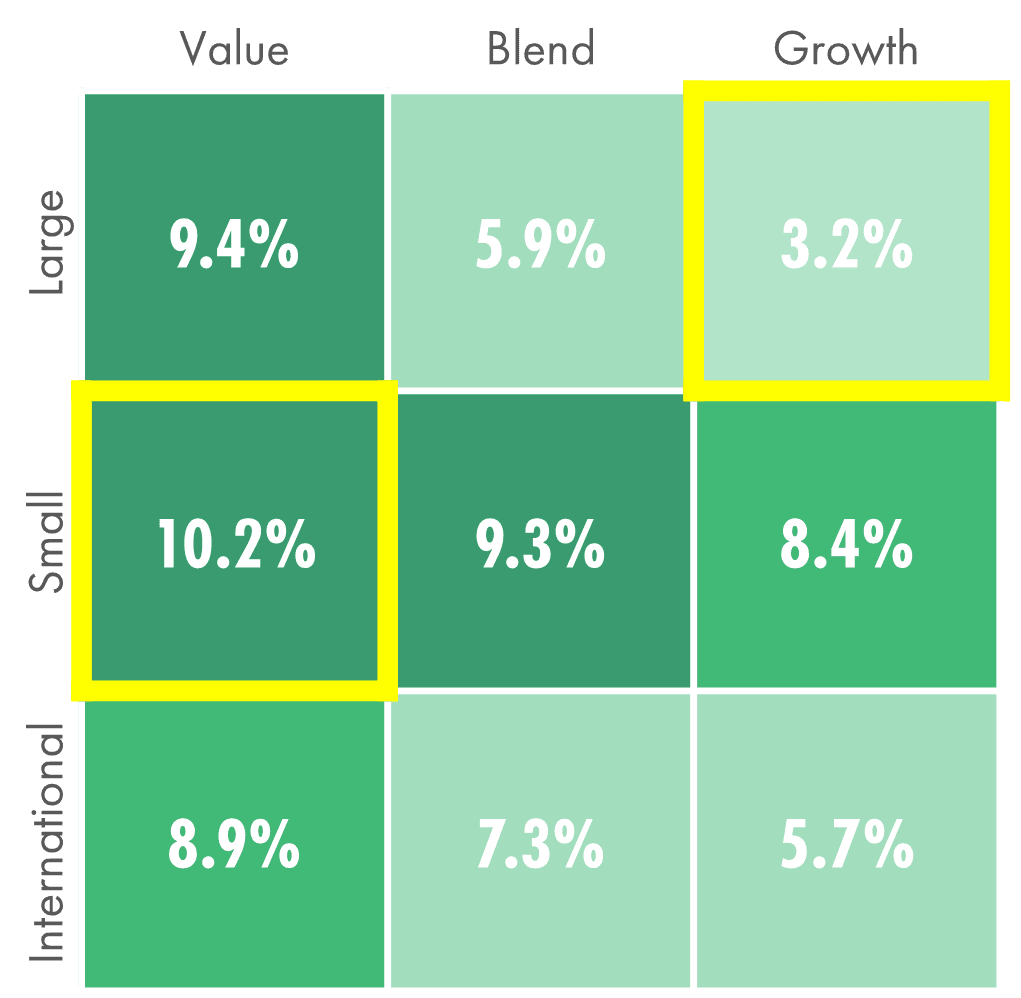

- Overall, U.S. Large Cap stocks are up 22% year-to-date and U.S. Small Cap stocks are up 11%. U.S. Large Cap Growth stocks, led by the “Magnificent 7,” saw momentum slow in the third quarter, gaining 3.2% after strong first half performance. In contrast, Small Cap Value stocks surged 10.2% in the third quarter after a weak first half, benefiting from lower interest rates and increased investor interest in undervalued sectors.

- International Developed and Emerging Markets extended their gains, up 13% and 17% year-to-date, respectively. Easing inflation, a slightly weaker dollar, and stabilizing economic conditions across major regions have contributed despite ongoing geopolitical challenges.

- Bond markets rallied as the Fed’s interest rate cuts pushed yields lower.

The U.S. economy has shown resilience, with GDP growing at an annualized 3.0% in the second quarter despite a softening labor market. Current data seems to suggest a gradual economic slowdown rather than a sharp contraction, alleviating some imminent recession concerns.

With inflation (as measured by the Consumer Price Index) at 2.5%, nearing the Fed’s 2% goal, the September interest rate cut marks a pivot in focus toward stabilizing the labor market. Fed Chair Powell emphasized that with inflation pressures easing, the Fed is now prioritizing measures to prevent further softening in the job market.

Asset Class Returns – As of September 30, 2024

The Long-Awaited Pivot

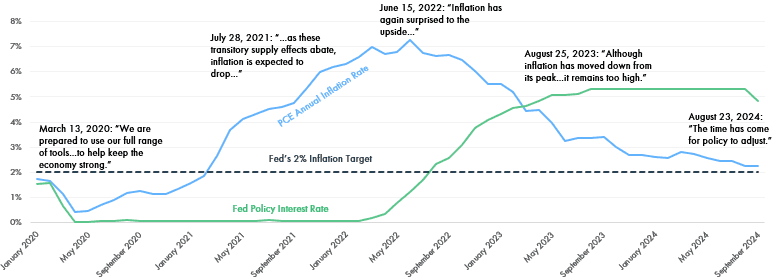

The Fed’s decision to cut interest rates by 50-basis points (0.50%) in September marks the first rate cut in four years, driven by data showing inflation is easing. The Fed is attempting to prolong the economic expansion while keeping unemployment from rising sharply.

Although job losses remain low, job openings have shrunk and unemployment has slowly climbed, signaling that the labor market, while still strong, might weaken without lower interest rates.

While the Fed, with the benefit of hindsight, clearly helped ignite inflation by keeping interest rates too low for too long, its actions in recent years have seemingly led to a “soft landing” for the U.S. economy, something few believed likely.

Shifting Focus to the Labor Market

The Fed’s Fight Against Inflation

Personal Consumption Expenditures (PCE) Annual Inflation Rate (Light Blue Line) and Fed Policy Interest Rate (Green Line)

Impact of Rate Cuts

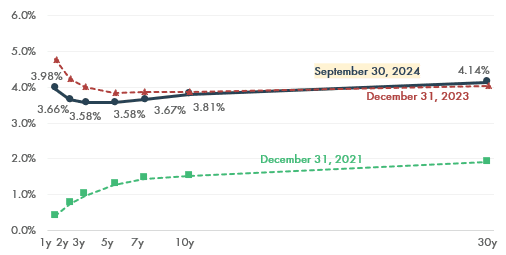

As the Fed reduces short-term interest rates, yields on shorter-dated bonds (like 2-year Treasury notes) tend to fall faster than those on longer-term bonds (like 10- or 30-year Treasuries). This causes the yield curve to steepen, or in today’s case, “un-invert” to a more normal curve. A normal yield curve is typically a positive sign for long-term economic growth, as it suggests that investors expect stronger long-term growth and healthier inflation prospects.

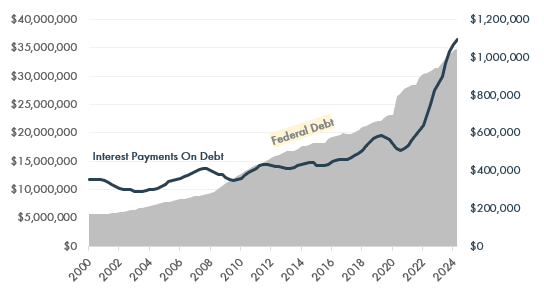

Lower interest rates would benefit any corporation which finances some operations with debt (i.e., bank loans). This can particularly benefit Small Cap stocks, as those companies tend to rely more heavily on shorter-term debt financing. In other words, lower borrowing costs can directly boost earnings by reducing interest expenses.

At the federal level while lower interest rates provide some temporary relief on the cost of servicing federal debt, this does not solve the long-term problem. The U.S. government’s enormous debt burden continues to rise, and even with reduced interest payments, future borrowing needs will likely offset any interest savings.

Yield Curve

U.S. Treasury Notes

Soaring Federal Debt a Rapidly Growing Problem

Federal Debt Held by the Public (Shaded, Left), Interest Payments on Debt (Blue, Right); USD Millions

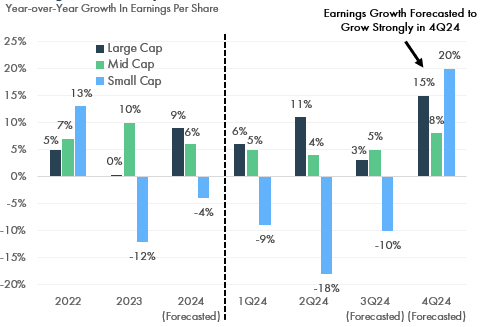

Earnings Growth Expected to Broaden Out

Year-over-Year Growth In Earnings Per Share

Source: JPMorgan (September 30, 2024)

The Bull Market Charges On

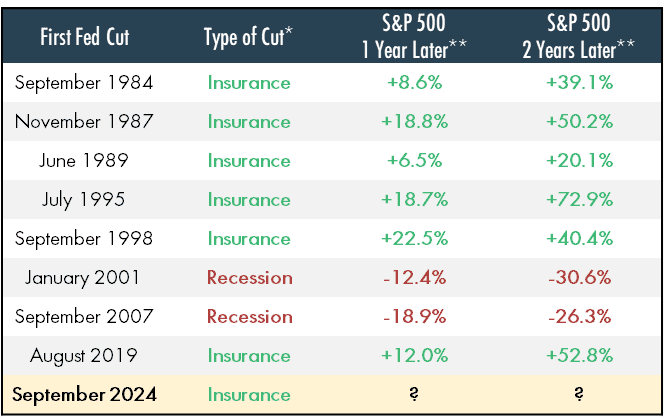

In the past eight interest rate-cutting cycles, the S&P 500’s performance going forward has been largely dependent on the economic backdrop which necessitated the interest rate cut.

- As shown to the right, when the Federal Reserve cut rates as a form of “insurance” during a healthy economy, the S&P 500 delivered strong positive returns over the following 1- and 2-year periods.

- In contrast, when the Fed cut rates as a response to a recession (as in January 2001 and September 2007), S&P 500 performance struggled, posting negative returns for both 1- and 2-year periods following the cuts.

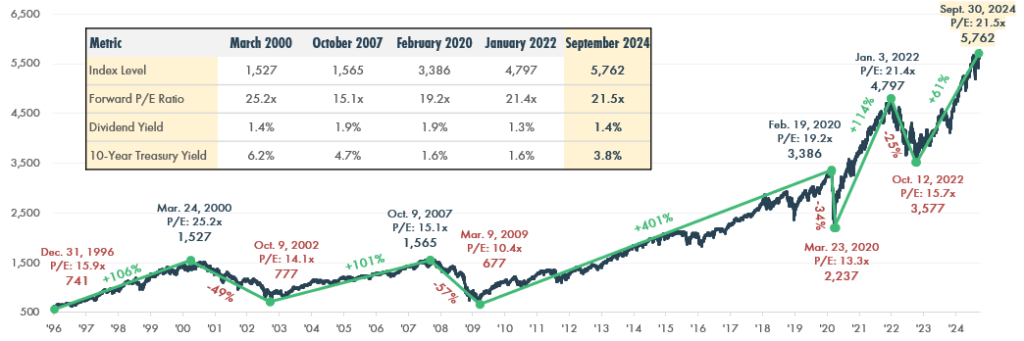

Historically, lower interest rates tend to boost stock valuations, as companies benefit from cheaper borrowing costs, resulting in higher future earnings. As rates decline, valuations (measured by metrics like the price-to-earnings ratio) typically expand. The S&P 500’s current valuation at 21.5 times next year’s projected earnings, however, is on the high side of normal, which may limit market growth for a time.

Some Insurance?

S&P 500 Return Following Start of Last Eight Easing Cycles

S&P 500 Inflection Points

Closing Price and Forward Price-to-Earnings Summary; January 1996 – September 2024

Market Rotation

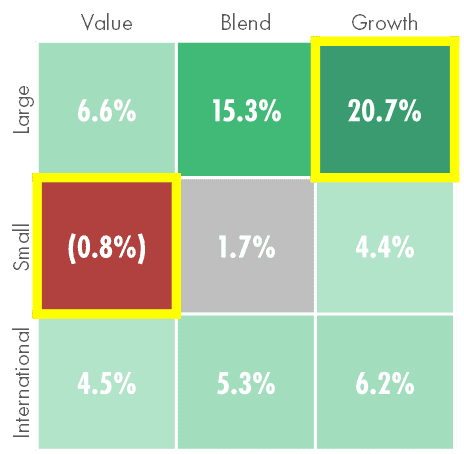

The third quarter marked a shift as Large Cap Growth stocks, which had surged by 20.7% in the first half, gained just 3.2%. In contrast, Small Cap Value stocks, down 0.8% in the first half, rose by 10.2% as investors rotated out of high-flying tech and into more undervalued, traditional sectors.

As many tech giants lost momentum, interest rate-sensitive sectors such as utilities (+19.8%) and real estate (+16.9%) led the market. Small Cap stocks, especially in Value sectors, gained traction from the prospect of lower interest rates, which would ease debt costs and improve earnings margins for smaller companies more reliant on external financing.

Investor enthusiasm for Artificial Intelligence (AI) stocks cooled somewhat in the third quarter as initial expectations for profitability faced reality. The slower-than-expected monetization of AI initiatives has led to a more cautious outlook, as companies work through the challenges of integrating and scaling AI technologies for meaningful revenue impact.

1st Half 2024 Returns

3rd Quarter 2024 Returns

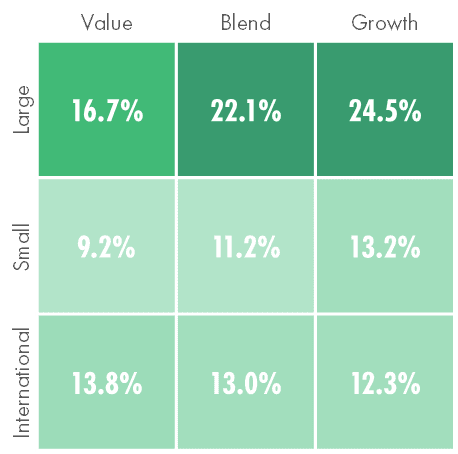

Year-to-Date Returns

Source: Morningstar Direct; Indexes used from top left to bottom right: Russell 1000 Value, S&P 500, Russell 1000 Growth, Russell 2000 Value, Russell 2000, Russell 2000 Growth, MSCI EAFE Value, MSCI EAFE, MSCI EAFE Growth

© 2024 The Finerty Team

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States. The Bloomberg US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.