Last week, Israel launched a direct attack on Iran, targeting key military assets including senior leadership, defense systems, and nuclear facilities. While this most recent escalation has yet to escalate into a significant market moving event (as we write), given the potential magnitude of the situation we thought it prudent to provide a brief update to the developing situation.

In Part 1 of our 3-part geopolitics series published in late 2023, we noted that “All told, the relative calm of the last three decades (pre-Russia’s invasion of Ukraine) is more likely to be an anomaly rather than a new normal. While we don’t advise extrapolating current events into perpetuity, it does seem prudent to expect military tensions to remain elevated for the foreseeable future.”

Earlier this year, Moneta had the opportunity to speak with The Carlyle Group’s, Admiral James Stavridis, who provided some perspectives on the current geopolitical environment (a full summary of the conversation can be found here). Regarding the Middle East, the Admiral noted: “Israel has really established “escalation dominance” over the last year with the Houthis in Yemen the only legitimate adversary at this time. Iran is reeling from losses incurred by Hezbollah in Lebanon and the regime change as Syria’s Assad was ousted by a rebel group. This portends lower risk of additional escalation and less appetite for Iran to respond especially with President-elect Trump to take office shortly. Iran itself is in an interesting domestic situation which its government and leadership will have to address or events may do it for them. The country is demographically very youthful and with over 52% of its ~90 million people under the age of 35. There is clear discontent by younger generations with the theocracy that Iran operates under.”

The Admiral’s comments were clearly informed and credible back in January. However, since then, Israel’s risk calculus clearly changed significantly with the International Atomic Energy Agency (IAEA) finding Iran in breach of its Non-Proliferation Treaty obligations and ongoing intelligence assessments of Iran’s nuclear program. This prompted Israel to take full advantage of Iran’s losses and domestic vulnerabilities by directly attacking the nation, in hopes of eliminating Iran’s nuclear program that Israel views as an existential threat to their nation’s existence.

From a market perspective, a disruption to the supply of oil remains the key risk, though this is somewhat contained as Iran’s oil exports are estimated to be around 1.7 million barrels per day, almost entirely going to China given strict economic sanctions on Iran. Any reduction in Iran’s supply could likely be brought back online quickly, given significant stockpiles from nearby Saudi Arabia and the UAE. More importantly, Iran has the potential ability to shut down the Strait of Hormuz, a key chokepoint in the global distribution of oil, though this is generally seen as a last-ditch effort as it would likely pull the US into the conflict and quickly alienate key allies, such as China, who depend on the route for oil supplies.

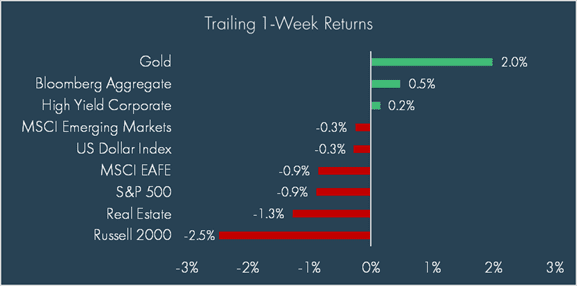

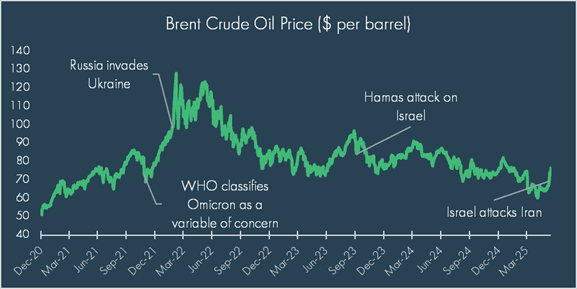

As we write, markets have largely brushed off these risks. While oil remains elevated, up more than 8% since June 12th, the absolute level is relatively low compared to recent history and only marginally higher from where it started at the beginning of the year.

Why is this a big deal? There are deep cultural roots in this conflict that cannot be overlooked. Persian Iran is broadly seen as the standard bearer for Shia Islam, backing (financially and militarily) multiple allied state and non-state actors in the broader region, including groups in Syria, Lebanon, Iraq, Yemen, and the Gaza Strip[1]. Additionally, Iran has generally been seen as an ally of Russia and China, though it is typically viewed as an “enemy of my enemy” situation rather than a like-minded alliance. The magnitude of the current situation and subsequent fallout will likely depend on whether Israel contains the escalation to “simply” destroying Iran’s nuclear capabilities or if they seek a complete collapse of the current Iranian regime – the former opens the door to potential treaties that allows the current government to “save face”, the latter could result in significant instability in the broader region. For investors, increased instability could lead to higher oil prices and supply chain disruptions leading to delays and higher shipping costs.

War brings with it many scenarios of how things could ultimately play out. Many well-informed pundits are watching each and every move of Iran, Israel and the US – militarily and diplomatically – to assess likely outcomes, knowing full well the “fog of war” reigns supreme even in these early stages. Many questions abound on the ultimate end game of Israel, capacity of Iran to continue its attack on Israel, it’s populace’s willingness to support its theocratic regime and importantly, the US’s appetite and willingness to participate more fully in this conflict.

While the range of scenarios are too numerous to detail, below are some of the “more likely” potential outcomes:

- Under mounting losses and internal pressure, Iran capitulates fully to the West’s demands for complete dismantling of existing and planned pursuit of nuclear weapons.

- Would Iran “surrender” their nuclear ambitions this easily and will it allow its current leadership to maintain power and legitimacy?

- Israel ends its military campaign following a thorough destruction of Iran’s current nuclear bomb producing capabilities and eliminating any threat via direct action against facilities, knowledge base, and supplies.

- Can Israel afford to judge success as degrading the nuclear ambitions and capabilities of Iran even without fundamental regime change?

- US enters the war by targeting a key Iranian uranium enrichment underground site – Fordow – to degrade Iran’s weapons-grade enrichment capabilities and destroy the suspected stockpile.

- Is another Middle East intervention by US military assets, which risks widening the conflict, something US government or its populace is willing to stand behind?

Russian involvement seems unlikely given the war in Ukraine that rages on with no end in sight. Meanwhile, the success of Western technology on the battlefield in Ukraine, the fall of the Russian-backed Assad region in Syria, and the decimation of Iran’s allies and defenses has not gone unnoticed by China. As we write, Chinese involvement in the situation has been extremely limited and aside from the slow and steady increase of pressure on Taiwan, the military tensions with China remain largely unchanged with conflict remaining in the economic realm of tariffs and sanctions.

Conclusion

Despite continued geopolitical consternation, markets have remained resilient. Recent strength has gone to non-US equity markets, yet even so, the S&P 500 is just shy of its all-time high reached in mid-February. Military conflicts have very real, life and death consequences, especially for those in war zones. However, markets are cold and calculating; quickly assessing the risk and pricing that risk accordingly – often recovering quickly following the initial drawdown and supporting our approach to long-term investing. The current situation is highly volatile and near-term market movements could be sharp depending how it plays out. We will continue to monitor closely. Stay tuned.

[1] https://www.congress.gov/crs-product/IF12587

DISCLOSURES

© 2025 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

DEFINITIONS

The S&P 500 Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States.

The Russell 2000® Index is an index of 2000 issues representative of the U.S. small capitalization securities market.

The MSCI EAFE Index is a free float-adjusted market capitalization index designed to measure the equity market performance of developed markets, excluding the U.S. and Canada.

The MSCI Emerging Markets Index is a float-adjusted market capitalization index that consists of indices in 21 emerging economies.

The Bloomberg U.S. Aggregate Bond Index is an index, with income reinvested, generally representative of intermediate-term government bonds, investment grade corporate debt securities and mortgage-backed securities.

The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

The US Dollar Index measures the US dollar against six global currencies: the euro, Swiss franc, Japanese yen, Canadian dollar, British pound, and Swedish krona.

The FTSE Nareit All Equity REITs Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. Constituents of the index include all tax-qualified REITs with more than 50 percent of total assets in qualifying real estate assets other than mortgages secured by real property.

The Dow Jones Commodity Index Gold is designed to track the gold market through futures contracts.

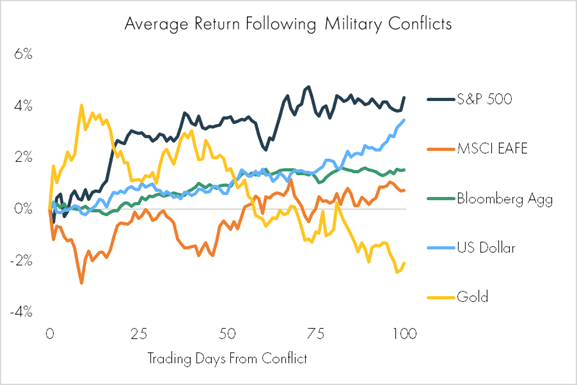

The Average Return Following Military Conflicts examines market reactions following 12 different military escalations: Hamas Attack on Israel (2023), Russia Invasion of Ukraine (2022), Crimea Conflict (2014), US Invasion of Iraq (2003), September 11 Attacks (2001), Kosovo War (1999), Iraq Invasion of Kuwait (1990), Iran-Iraq War (1980), Arab Oil Embargo (1973), Cuban Missile Crisis (1962), Pearl Harbor Attack (1941), German Invasion of Poland (1939). Due to data limitations, certain indexes do not have returns for all the noted conflicts.