Chris Kamykowski, CFA, CFP® – Head of Investment Strategy and Research

Howard Cosell’s immortal words during the January 1973 heavyweight championship fight between Joe Frazier and George Foreman are an apt – if not overly dramatic – way to react to Friday’s announcement of the US losing its last AAA-rating. After taking “blows” from other ratings agencies (Standard & Poors in 2011 and Fitch in 2023), the third major rating agency, Moody’s Ratings, removed the world’s leading super power, largest economy, and the most dynamic market from the upper echelon of credit quality. In this blog post, we will go through why Moody’s downgraded the US, what it means for the US, potential political reactions, and perspective on market reaction.

Moody’s Downgrade

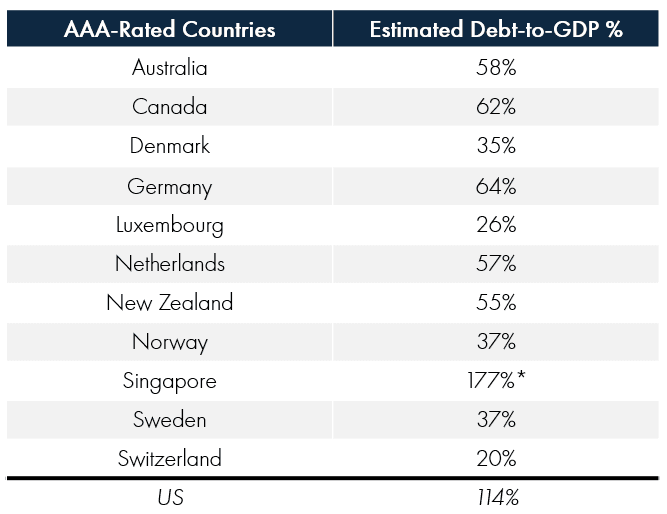

Rating agency, Moody’s Ratings, downgraded the US government debt from Aaa to Aa1, citing concerns about the future trajectory of enormous fiscal deficits and increasing interest rate cuts relative to similarly rated sovereigns. Moody’s was the last of the major ratings agencies to downgrade the US from AAA, following S&P in 2011 and Fitch in 2023. For those less familiar with credit ratings, specifically Moody’s, Aaa long-term ratings means the obligations (US Treasuries, for instance) are “judged to be of the highest quality, with minimal risk”. Aa1 is “judged to be of high quality and are subject to low credit risk”. Therefore, the US is still far and away essentially a risk-free credit although 11 other countries* now claim the highest of AAA ratings now.

Despite any consternation about the formal change in rating, Moody’s action should not be a surprise. In November 2023, Moody’s changed its outlook for the US ratings to negative and earlier this year, it noted the fiscal strength of the US appeared headed for weakness under most scenarios That said, their recent announcement noted the outlook for US debt was judged as “stable” given the US Treasury market’s “size, resilience and dynamism of its economy and the role of the U.S. dollar as global reserve currency.” [1]

What does it mean for the US?

It is more of an embarrassment (and warning) to the US to see its credit rating fall versus suggesting a major implication for investors or the US Treasury market. Investors – domestic and foreign alike – will still buy Treasuries. Importantly, this downgrade is not related to a pending default which would see immense turmoil in Treasuries and equity markets as the risk-free rate would likely move significantly higher, shifting borrowing costs higher across the world for other consumers, sovereigns and credits. The move will likely result in a degree of Treasury repricing with rates already moving higher. Yet for now, while the fiscal trajectory Moody’s reacted to continues, the US is still the premier destination for “risk-free” investment for investors.

How are markets faring?

On that note, this occurs as markets are recovering quite strongly since the lows of April on the back of “Liberation Day” with negotiations bringing forth reasonable expectations of deals to thwart the potential negative economic implications of a major tariff/trade war. Recently, the United States and the United Kingdom announced a framework aimed at reaching a comprehensive trade agreement Additionally, the US will roll back its 125% reciprocal tariff rate on China to 10% but leave in place the 20% additional tariffs that were applied on all Chinese goods in February and March for a period of 90 days, beginning May 14. This provides a bit of relief to markets as recession risks have fallen on the back of the news.

Therefore, this backdrop, plus continuing strength in the economy, may allow for the downgrade to be manageable. Treasury markets are taking the news in stride on 5/19, with yields on the long end of the curve rising more than the short end; notably, the 30-Year US Treasury breached 5% earlier in the day before falling back below. Moves in the equity markets have the S&P 500 marginally lower to flat mid-way through 5/19, though the S&P has risen nearly 20% since its April 8th low.

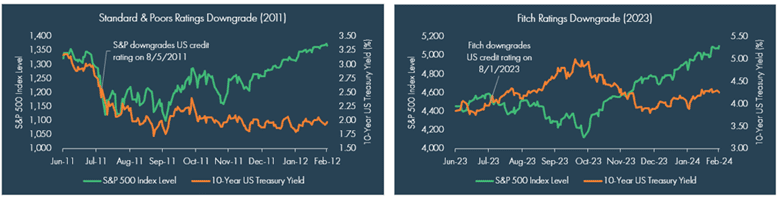

Past downgrades by S&P and Fitch shed light on how the markets may fare from here in the near-term but situations were very different for each at the time of the downgrades.

- Standard & Poor’s downgrade in 2011 came on the heels of the Global Financial Crisis with the US economy still working to fully recover from the damage from the crisis. The 10-Year Treasury fell 24 bps and the S&P 500 fell -6.6% the day following the announcement; however, six months later the 10-Year had fallen an additional 31 bps but the S&P was up 13.2%.

- Following Fitch’s 2023 downgrade, the economy was on much better footing and the Fed was in a monetary tightening cycle. The 10-Year Treasury rose 5 bps and the S&P 500 fell -1.4% one day after the announcement. Six months later the 10-Year yield was down an additional 20 bps while the S&P 500 was up 8%.

Is this the catalyst needed for elected representatives?

Interestingly, the downgrade comes in the midst of Congress attempting to slow the deteriorating fiscal situation in the US. The “one big, beautiful tax bill” is within Congress’s reconciliation process currently but faces an uphill battle. The House’s Budget Committee failed to advance the extension of tax cuts last week as a group of Republican fiscal hawks joined Democrat colleagues and voted against the legislation until more spending cuts were enacted. Yet, this morning comes news that the tax and spending packaged advanced through the Committee after compromises over Medicaid spending. The bill still faces an uphill battle, with more negotiations and more theatrics likely before Trump signs any legislation. Fixing the trajectory and forestalling the consequences of $2 trillion dollar annual deficits is an important endeavor. Can the downgrade be a catalyst for Congress and the President to avoid “kicking the can” for the umpteenth time? That is a question we will have to wait to see. Regardless, as we noted in our blog post in August 2024, “The fiscal problems are real, but solutions are possible – though real solutions will take immense fortitude by elected leaders.”

Conclusion

The fiscal situation has been spiraling south for many, many years and while it seems to have finally caught up with the US, a one notch downgrade from AAA is nowhere near the end of the world. There is pride at stake but to recover it means seriously addressing $2 trillion deficits, net interest costs of 18% of tax revenues, and debt-to-GDP levels of over 110%. Likely, no one wants the new trade to become “Sell America” or for us to relinquish the exceptionalism that has driven and buttressed the country since its founding. However, nothing in this world is guaranteed and Moody’s announcement is hopefully a clear warning concerning that. While Frazier did lose his title over 50 years ago to Foreman, the US may be down but it is not out. The capability to “get back on our feet”, turn around the fiscal situation and restore our AAA status is there, though it may behoove elected officials to drive for fundamental changes to our trajectory before others’ (a.k.a. the market) decide to ring the bell.

Sources:

[1] https://www.moodys.com/web/en/us/about-us/usrating.html

- Strategas

- JPMorgan

- Bloomberg

- Morningstar

- The Wall Street Journal

Definitions:

The S&P 500 TR Index is a free-float capitalization-weighted index of the prices of approximately 500 large-cap common stocks actively traded in the United States.

Disclaimer

© 2025 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.