By:

Randy Stauder, Portfolio Strategist

Tim Burford, Investment Specialist

Words such as “bubble” and “peak” are being used to describe today’s residential real estate market. To put it simply: the housing market has been red hot since the end of April 2020. It is common to hear about all-cash offers or buyers waiving inspection contingencies, among a host of other tactics used to sweeten purchases. While the COVID-19 pandemic provided a unique catalyst for the residential real estate market, most would agree that there are a handful of forces which influence the housing market with supply and demand at the top of the list.

Supply

During the two-month period of March and April 2020, residential real estate collapsed alongside the sharpest economic downturn in modern history. Uncertainty was abundant for investors and homeowners alike. The supply of houses for sale, however, was far from abundant. As the world shut down in an attempt to slow the spread of COVID-19, countless jobs were lost or furloughed and many homeowners were hesitant to sell. Homeowners were also reluctant because selling meant they would be a buyer in the same challenging market. Additionally, many households had the opportunity to refinance their mortgage rather than sell given historically low interest rates, which further limited the supply of homes.

The new-build segment of the housing market also faced tremendous disruption. In a segment that many believe did not keep up with demand after the end of the Great Financial Crisis in March 2009, housing development faced an entirely new set of obstacles. Laborers were required to stay home, and construction sites halted. Once stay-at-home orders were lifted, labor shortages and supply chain issues followed. These factors triggered unprecedented spikes in building costs. For example, the price of lumber soared to more than three times previous record highs. Builders, retailers, and others worried about running out of materials and in turn hoarded the supply they had on-hand. Builders raised home prices to maintain their margins, and many stopped selling houses before the studs were installed to avoid misjudging costs and losing money. Paired with the countless other material bottlenecks and an already short supply of land, new home prices were primed to jump, regardless of the demand, if builders were to earn a profit.

Demand

The housing market has rarely, if ever, been this competitive. Bidding wars are common, and listings in some areas sell within a matter of days. As COVID-19 forced businesses and schools to close their doors, the shift to remote work and learning happened overnight. Suddenly, the whole family found themselves at home all day, sending buyers scrambling to find bigger homes for both work and play. Location and commute became an afterthought, particularly in larger cities, as buyers cared more about space than proximity.

The Federal Reserve acted swiftly and cut interest rates to help stabilize the economy. Already historically low mortgage rates declined further, and the average 30-year mortgage rate decreased from 3.65% in March 2020 to 2.67% by the end of the year[1] thus giving many homebuyers more buying power than ever before.

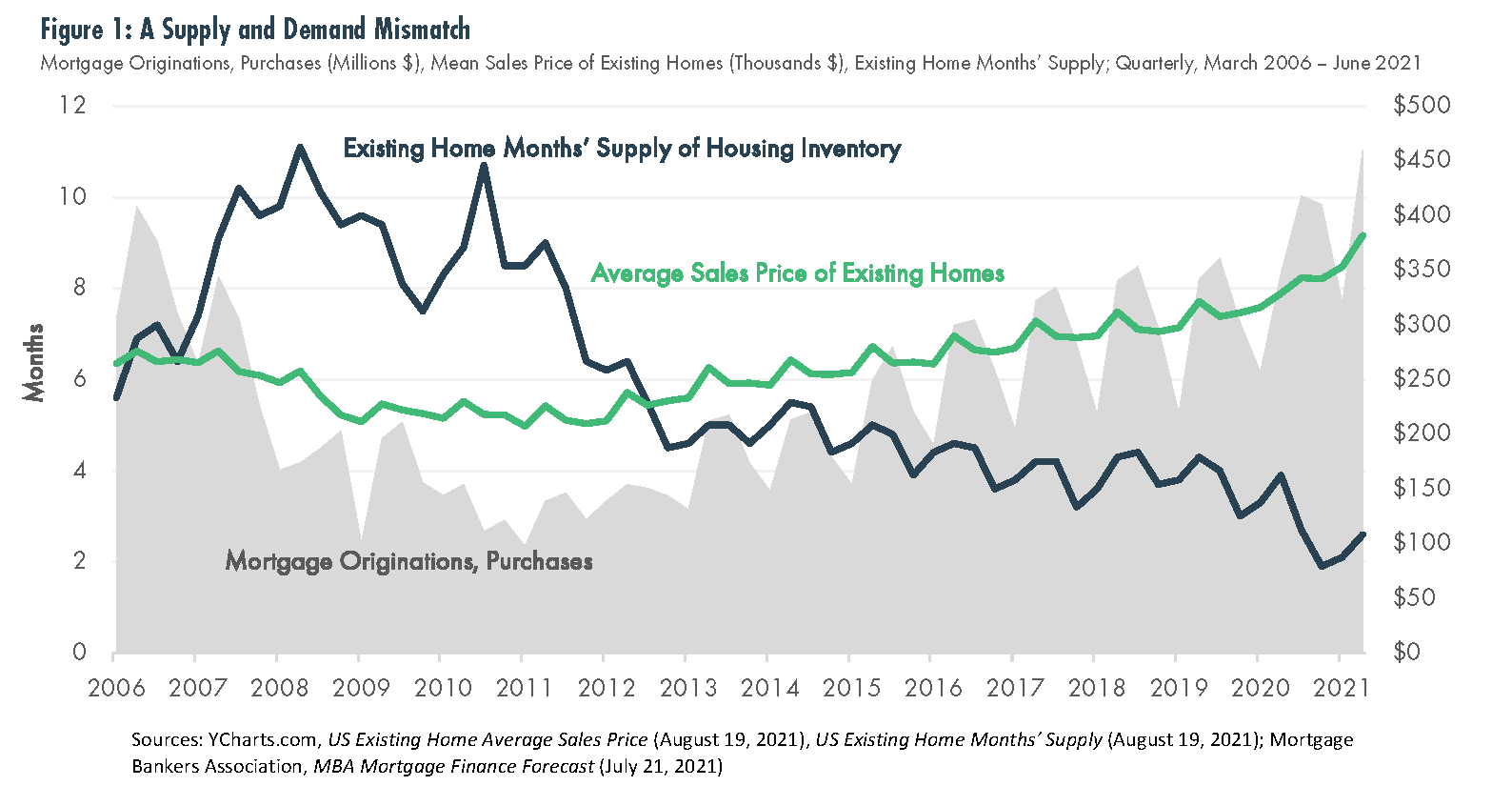

Conversely, high list prices and “sticker shock” caused some homebuyers to pause during the first half of 2021. Existing home sales declined for five straight months beginning in January 2021. They slightly increased in June 2021 but only by 1.4%[2]. Nevertheless, demand, as measured by purchase mortgage originations (see Figure 1), remains robust.

Today, the housing market remains a far cry from normal. Supply is 30% lower compared to a year ago[3], while demand has only shown brief signs of moderating. Given this severe imbalance, home values have increased in virtually every corner of the nation at a pace rarely seen before. The average home value continues to set all-time highs, which inevitably leads some to wonder if the housing market is due for a correction. While possible, many factors contributing to the boom still persist and future demand should be supported by long-term tailwinds.

Where could it go from here?

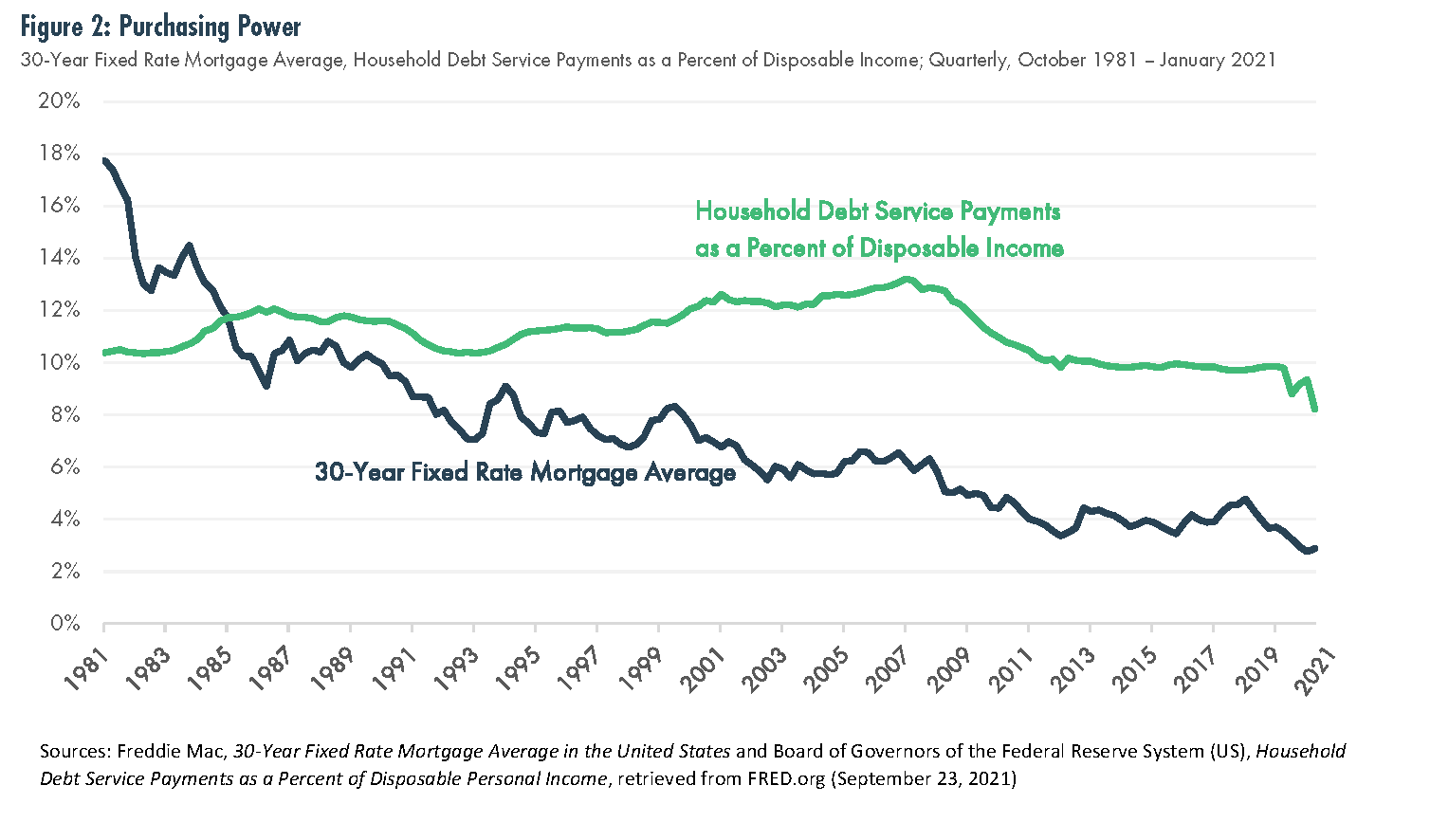

Buyers appear to be in great financial shape, as consumer balance sheets have seldom looked better. On average, U.S. consumers are now spending less on debt payments as a percentage of disposable income since the beginning of 1980 (see Figure 2). Because mortgage payments make up the largest portion of a household’s annual expenses[4], lower mortgage rates have helped homebuyers maintain their purchasing power even as home prices continue to rise.

A greater tailwind is the millions of millennials entering their thirties, the prime age for first-time home buyers. Many millennials not affected by layoffs/furloughs accumulated sufficient savings through stimulus checks, student loan forbearance, and far less spending on discretionary items to use towards a down payment. This new generation of homebuyers, the largest generation as a percentage of the entire U.S. population[5], will likely increase demand for years to come.

Today’s housing market looks to be on much firmer ground compared to 2007 – the only period on record (dating back to 1975) in which the entire U.S. housing market experienced a simultaneous downcycle – particularly in terms of fundamentals (i.e., healthier borrowers and lenders). A flood of new supply (both from sellers and builders) could cause home prices to cool off or even correct, but a systemic crisis on the scale of the Global Financial Crisis appears less likely today.

© 2021 Moneta Group Investment Advisors, LLC. All rights reserved. Moneta Group Investment Advisors, LLC is an SEC registered investment advisor and wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. Moneta is a service mark owned by Moneta Group, LLC. The information contained herein is for informational purposes only and is not intended to be comprehensive, exclusive, nor represent any recommendation.

[1] Freddie Mac: “30-Year Fixed Rate Mortgage Average in the United States” retrieved from FRED.org (August 19, 2021)

[2] National Association of Realtors: “Existing Home Sales Expand 1.4% in June” (July 22, 2021)

[3] YCharts.com: “US Existing Home Months’ Supply” (August 19, 2021)

[4] Bureau of Labor Statistics: “Consumer Expenditures – 2020” (September 9, 2021)

[5] Statista: “Population Distribution in the United States in 2020, By Generation” (August 19, 2021)