Tim Side, CFA® – Investment Strategist

“Prediction is very difficult, especially if it’s about the future.”

-Niels Bohr[1]

The current environment is rife with uncertainty. Following two seismic events, the COVID-19 pandemic and the first ground war in Europe since World War II, investors have also had to grapple with the most rapid rate hiking cycle from the Federal Reserve since 1980, deteriorating relations between the United States and China, the two largest economies in the world, a downgrade in the credit rating of the U.S., the country behind the global reserve currency, and a war in the Middle East. As we enter 2024, a major election year for many countries around the world, the heighted geopolitical consternation appears poised to continue.

For this reason, we have embarked on the difficult task of providing some context and insights into the current macroeconomic environment. To ensure the subject receives the necessary amount of attention while staying at a manageable length, we will be breaking this piece up into three separate blog posts over the next several weeks:

- Part 1: Where are we now? A review of the current geopolitical environment to determine whether things are different today and to help set the stage for an understanding of how geopolitics affects markets.

- Part 2: Where are we going? A review of long-term trends potentially forming.

- Part 3: What should we do? A practical guide on how to invest around geopolitical uncertainty.

Part 1: Where are we now?

On January 24, 2023, the Science and Security Board of the Bulletin of the Atomic Scientists moved the hands of the Doomsday Clock to 90 seconds to midnight.[2] This clock was originally created in 1947 by a group of scientists, including Albert Einstein, “using the imagery of apocalypse (midnight) and the contemporary idiom of nuclear explosion (countdown to zero) to convey threats to humanity and the planet.” The clock’s current reading is the closest to midnight that it has ever been, highlighting an extreme view that we are on the verge of a worst-case scenario and perhaps providing summation of the feeling that things are bad.

Why do things feel so poor? Despite the commonly used term ceteris paribus (all other things being equal) in Economics 101, macroeconomics does not exist in a vacuum and all other things are rarely held constant. In other words, it is complicated.

However, as we look at the current environment, many of the issues investors face today can be, at least in part, explained by three prominent themes: deglobalization, the political environment, and a resurrection of superpower military tensions. These themes are neither all-inclusive nor independent of each other, but they can be used to give us a framework on how to think about the current environment.

Deglobalization

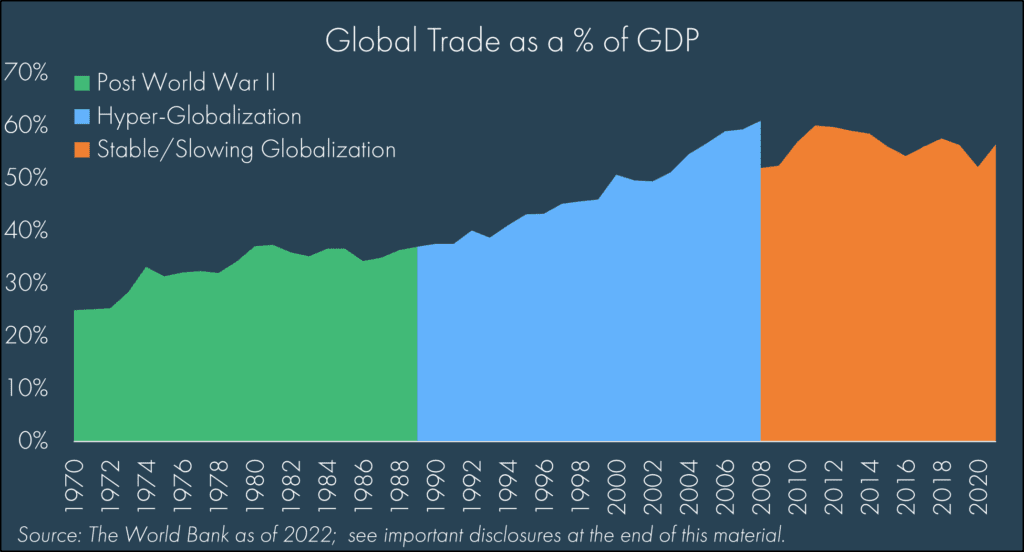

Economic globalization[3] has gone through several phases over the past 150 years. The first phase of globalization occurred from 1870 to 1914 and has been described as the “first golden age of globalization.” During this phase, trade openness[4] increased by more than 75%. World War I decimated this progress, with trade openness declining to levels lower than 1870 and lasting through World War II. The third phase began after World War II, as transportation costs declined and the Bretton Woods agreement in 1945 provided a global system of order, reducing barriers to trade. The gains in trade openness did not happen overnight though, as pre-World War I levels were not seen again until the 1970s.[5]

The fourth phase of globalization began in the early 1990s, as global trade as a percent of GDP rose from 38% in 1990 to 61% in 2008. While still at elevated levels relative to history, globalization has never returned to its peak in 2008, with some referring to this period as the fifth phase of globalization.[6]

The Global Financial Crisis did not destroy global trade, pointing to a highly integrated global economy and policies designed to keep this structure intact. Instead, the formal deterioration in U.S. trade relations began in earnest with former U.S. President Donald Trump’s tariffs (a tax on certain imports or exports) on specific Chinese imports. This led to the infamous “Trade War” in 2018, as the U.S. expanded tariffs to include additional goods and countries and those countries subsequently responded with their own tariffs on the U.S.[7]

With a backdrop of declining trust and lower trade openness, the COVID-19 pandemic disrupted supply chains and shifted companies’ philosophy of “just in time” to “just in case.” This philosophy shift was further cemented following Russia’s invasion of Ukraine and an escalation in U.S.-China tensions.

The term “deglobalization” is intuitive, though a bit extreme, given its implication of a world reverting to a pre-Cold War or even pre-Bretton Woods era. The better terms, in our opinion, have been “nearshoring” or “friendshoring,” which imply a re-working of supply chains for better resiliency in the face of rapidly changing geopolitical dynamics. Some protectionism is to be expected, and some manufacturing is coming back to the U.S. specifically, as noted by a recent Wall Street Journal article.[8] However, what we at Moneta are consistently hearing from investment managers and was alluded to in the referenced Wall Street Journal article, is that companies are not necessarily shutting down factories in places like China; they are just not sending incremental expenditures to China. Instead of sending new projects to China, they are building plants in Poland, Vietnam, Indonesia, India, Mexico, and yes, the United States, too. This in and of itself does not destroy globalization; it simply reshapes it.

There is, of course, nothing simple about the great restructuring of the global supply chain. India’s culture is very different from that of China. Mexico’s culture is very different from that of Vietnam. Building resiliency is going to take a significant amount of time, expertise, patience, and money, ultimately informing expectations for higher costs going forward.

The Political Environment

Hyper-globalization created winners and losers. U.S. investors largely seemed to be winners, as the S&P returned an annualized 10% from 1990 to last month’s end (11/30/2023). U.S. citizens had mixed experiences, as the “average” U.S. worker saw real wages grow at an annualized rate of 0.4% from 1990 to July of 2023.[9] Western Europe had mixed responses; from 2001 to September 2023, the United Kingdom (UK) saw real wages decline at an annualized rate of -3.7% while Germany saw an annualized increase of more than 7%. Meanwhile, developing countries like China and India, though also mixed within their respective countries, saw significant gains in their standard of living.[10]

While not solely responsible, the mixed economic gains are at least partially responsible for the recent rise in populism.[11] 2016 was a notable year for the dual shock of the UK voting to leave the European Union and the U.S. electing Donald Trump as its 45th President. The narrow margins by which these critical events were decided cannot be dismissed, but nevertheless, both decisions went in favor of the “populist” movement. Over the next several years, support for populist candidates continued to grow, notably in European countries such as Italy, Hungary, and France.[12]

The pull towards “controversial” candidates across the political spectrum has created a highly polarized environment. The challenges facing policy makers around the world (rising interest costs, aging populations, immigration challenges, and climate change to name a few) have no easy solution. Add in the changing world order as the U.S. steps back (even if only marginally) from its military role, and the path forward can appear extremely uncertain. 2024 will be a monumental year as countries with more than half of the world’s population, including major players like the U.S., India, the UK, and Russia, head to the polls.

Escalating Military Tensions

Two defining moments in the post-World War II era include the Bretton Woods agreement of 1945 and the end of the Cold War in the early ‘90s. In short, the Bretton Woods agreement created the “system of economic order and international cooperation that would help countries recover from the devastation of the war and foster long term global growth.”[13] Supported by the military and economic strength of the United States, that system largely remains in place today.

Whether by necessity or ideological alignment, Bretton Woods pulled the majority of the major world players to the United States’ “side,” with the notable exception of the Soviet Union. Following the fall of the Berlin Wall in 1989 and the collapse of the Soviet Union in 1991, the world entered an unprecedented time of global peace, enjoying the so-called “peace dividend”. To be sure, there was never complete peace, most notably in the Middle East. Combined with rapid advances in technology leading to the advancement of technology and internet, the era of hyper-globalization was almost inevitable.

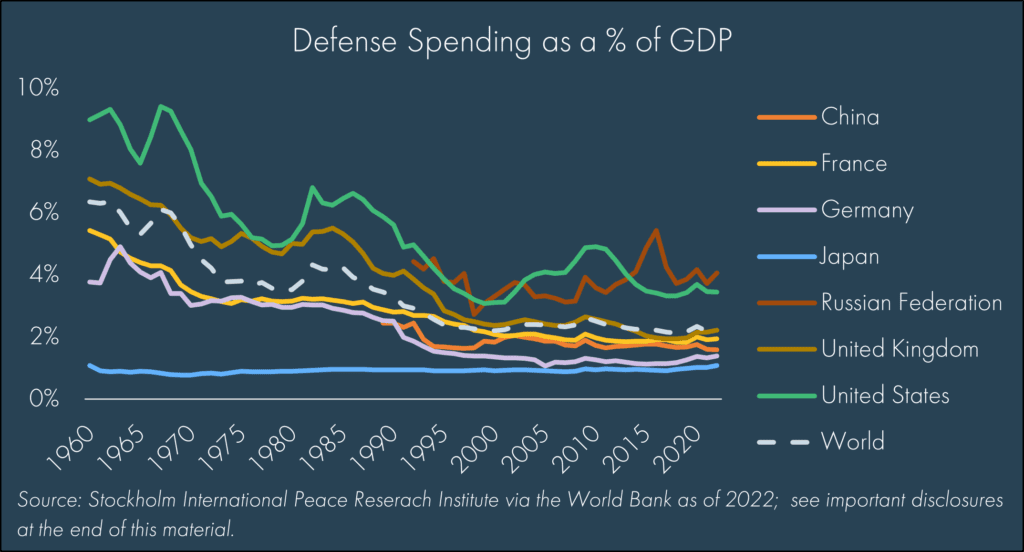

As we noted, “global peace” did not mean there were no military conflicts. A fact that the U.S. is acutely aware of, as their hegemon responsibilities forced them to maintain a heavy military presence around the world and intervene when necessary. The imbalance of military spending between the U.S. and their allies continued to grow over the last several decades, further exacerbated by costly wars in Afghanistan and Iraq. With no clear threat to world order (such as the Soviet Union back in the Cold War), the benefits of the U.S. shouldering the military burden of the world have become less clear to U.S. citizens, leading to calls for an increase in allied military spending and less support for the U.S. to engage in military conflicts.

Following Russia’s invasion of Ukraine, the U.S. emphatically backed Ukraine with military, financial, and humanitarian aid. While the U.S. provided the most aid, it is notable that many other countries, such as Germany, the U.K., and Norway, also provided military aid.[14] Following Hamas’ attack of Israel in early October, the U.S. is finding itself pulled into yet another war, although it has thus far avoided boots on the ground in both conflicts.

Amid both these wars, the elephant in the room has been China. The second largest economy in the world, China has emerged from the hyper-globalization era as a key “threat” to the U.S. As we discussed in our China review last December (link here), the flaw in the original thesis of investing in China was that to be economically successful, China would adapt and move closer to Western values. Recent, heavy handed regulatory actions from Chinese President Xi Jinping have all but eliminated that thesis, and there appears to be bi-partisan support in the U.S. for taking a strong stance against China from both a national security[15] and economic perspective.[16] Over the past decade, China has grown its influence via economic incentives, such as the Belt and Road initiative, and officially, China’s military spending has stayed relatively constant at roughly 1-2% of GDP, or approximately $290 billion in 2022. However, according to U.S. intelligence, the real military spending number is likely closer to $700 billion,[17] creating concerns around the next phase of China’s growth. The economic incentives for China to avoid a military escalation seem obvious, but it would be imprudent to assume that this would preclude them from at minimum strengthening their military capabilities.

All told, the relative calm of the last three decades (pre-Russia’s invasion of Ukraine) is more likely to be an anomaly rather than a new normal. While we don’t advise extrapolating current events into perpetuity, it does seem prudent to expect military tensions to remain elevated for the foreseeable future.

Part 1 Conclusion

The geopolitical picture is a dynamic one today. Extreme indicators such as the Doomsday Clock would say these are worse now than they have ever been, yet our look around the world points to a shifting in world order, not necessarily a complete deterioration. As disciplined investors, we have to take things for how they are and not how we want them to be. To know how things are, it is helpful to understand how we got here.[18] Parts 2 and 3 of this series will address where we might be going and what we should do. At Moneta, we will continue to account for these geopolitical risks and re-underwrite our portfolio recommendations with them in mind. We can’t predict the future, but we can seek to build resilient, all-weather portfolios that give you a high probability of success in meeting your financial goals.

DISCLOSURES

© 2023 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

DEFINITIONS

Trade (% of GDP): Trade is the sum of exports and imports of goods and services measured as a share of gross domestic product. Source: World Bank national accounts data, and OECD National Accounts data files.

Military expenditure (% of GDP): Military expenditures data from SIPRI are derived from the NATO definition, which includes all current and capital expenditures on the armed forces, including peacekeeping forces; defense ministries and other government agencies engaged in defense projects; paramilitary forces, if these are judged to be trained and equipped for military operations; and military space activities. Such expenditures include military and civil personnel, including retirement pensions of military personnel and social services for personnel; operation and maintenance; procurement; military research and development; and military aid (in the military expenditures of the donor country). Excluded are civil defense and current expenditures for previous military activities, such as for veterans’ benefits, demobilization, conversion, and destruction of weapons. This definition cannot be applied for all countries, however, since that would require much more detailed information than is available about what is included in military budgets and off-budget military expenditure items. (For example, military budgets might or might not cover civil defense, reserves and auxiliary forces, police and paramilitary forces, dual-purpose forces such as military and civilian police, military grants in kind, pensions for military personnel, and social security contributions paid by one part of government to another.) Source: Stockholm International Peace Research Institute (SIPRI ) via the World Bank national accounts data, Yearbook: Armaments, Disarmament and International Security.

[1] While many attribute the quote to Danish Physicist and Nobel Laureate Niels Bohr, similar quotes have been attributed to Yogi Berra, Samuel Goldwyn, Robert Petersen, and Mark Twain.

[2] https://thebulletin.org/doomsday-clock/current-time/

[3] Defined by Oxford Dictionary as the process by which businesses or other organizations develop international influence or start operating on an international scale.

[4] A commonly used proxy for globalization is a measure known as “trade openness,” a simple calculation that divides the sum of global trade (imports and exports) by total gross domestic product (GDP).

[5] https://www.piie.com/publications/working-papers/hyperglobalization-trade-and-its-future

[6] https://www.capitalmarketassumptions.com/

[7] https://taxfoundation.org/research/all/federal/tariffs-trump-trade-war/

[8] https://www.wsj.com/articles/american-manufacturing-factory-jobs-comeback-3ce0c52c

[9] U.S. Bureau of Labor Statistics, Employed full time: Median usual weekly real earnings: Wage and salary workers: 16 years and over [LES1252881600Q], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/LES1252881600Q, December 4, 2023.

[10] https://am.jpmorgan.com/us/en/asset-management/protected/adv/insights/market-insights/guide-to-the-markets/

[11] Defined by Oxford Dictionary as a political approach that strives to appeal to ordinary people who feel that their concerns are disregarded by the established elite groups.

[12] https://www.pewresearch.org/short-reads/2022/10/06/populists-in-europe-especially-those-on-the-right-have-increased-their-vote-shares-in-recent-elections/

[13] https://www.worldbank.org/en/archive/history/exhibits/Bretton-Woods-and-the-Birth-of-the-World-Bank

[14] https://www.cfr.org/article/how-much-aid-has-us-sent-ukraine-here-are-six-charts#:~:text=Since%20the%20war%20began%2C%20the,Economy%2C%20a%20German%20research%20institute.

[15] https://www.npr.org/2023/02/28/1159132544/congress-zeroes-in-on-china-as-economic-and-security-threats-loom

[16] https://taxfoundation.org/research/all/federal/tariffs-trump-trade-war/

[17] https://www.congress.gov/118/crec/2023/06/01/169/95/CREC-2023-06-01-senate.pdf

[18] A few pages cannot fully do justice to the complexities of geopolitics. For those interested in an excellent historical perspective on geopolitics, we would recommend reading Henry Kissinger’s World Order (2014).