by Andrew Kelsen – Head of Alternative Investments

Setting expectations for alternative investments

2019 through 2022 were not normal times. The combination of COVID, war in Ukraine, sharp episodes of inflation, white hot deal markets and volatile equity and fixed income markets created an unprecedented set of challenges and upsets.

2023 has seen a return of cautious optimism. The economy is finding its sea legs, inflation, at least by the headline number appears to be retreating and the much-feared recession has been postponed by the forecasters until 2024 if at all.

There are still clouds on the horizon. The Fed tightened until something stopped breathing, then resuscitated it. Credit is tight and staying tight. We have an inverted yield curve (typically a harbinger of a recession) that is playing havoc with investors’ asset allocations and corporate balance sheets. Commercial real estate is facing serious challenges in certain sectors like CBD office, while other spaces like industrial, multifamily housing, data centers, senior housing and grocery are having good years. Venture capital broadly is still challenged, but we have seen 51 new unicorns this year.

So where does that leave us today as we think about our asset allocation plans and committing capital to alternative investments?

The honest answer is it leaves us where we are every year. Right here with our eyes wide open. We cannot predict the future. There is no crystal ball.

In the space below we will offer some thoughts on how to think about where we are across private equity, private credit, real estate and real assets.

Private Equity

Our discussions with our peers, bankers, managers and partners about the current environment have led to some common themes.

- Capex (“Capital Expenditure”) has slowed, companies are cautious about allocating capital.

- A large majority of companies hit EBITDA targets.

- Companies are very mindful of signs of inflation and recession.

- Returns will be driven by fundamental growth, not growth at any cost

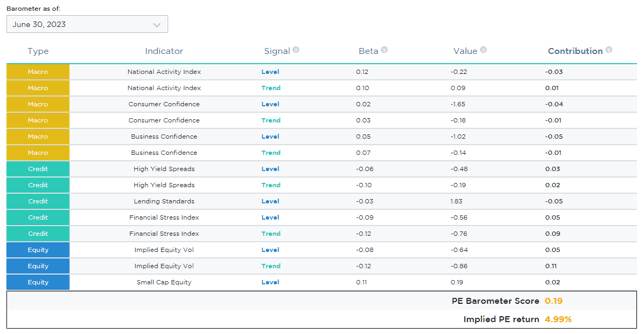

When we think about the macro, equity and credit inputs that drive broad, median private equity returns, one tool we use is the Pitchbook PE Barometer that attempts to factors all of these into the calculation.

Based on this tool, using the quarterly model above, we see that going forward, median PE returns should be somewhere in the 20% annual range. We certainly are hearing that firms are going to try to pay lower purchase prices and multiples to generate the same returns. The cost of debt from January 2022 to today has increased from roughly 5.0% to 11.5%. We would expect to see the amount of debt used to decrease and the amount of equity increase. Operational expertise and the ability to bring resources to bear will be very important. Doing it the way it was done 2018-2021 will almost certainly lead to a decrease in IRR and multiple.

Outlook: We expect top quartile buyout returns to continue to deliver low to mid 20% net IRR’s and 2.0X-2.4X net multiples of capital.

Private Credit

For the purposes of this report, we will be focusing on the direct lending segment of private credit.

Direct lending has provided some of the highest yields seen in decades. 10%-12% is easily attainable with very conservative capital structures. It is a great time to be a provider of new debt capital. Borrowers are continuing to turn to nonbank lenders to provide debt financing. The certainty of execution and deal specific terms cannot be matched by banks. As banks continue to pull away from traditional lending businesses, the opportunity set will only grow. Wall Street syndicated loans are expensive, slow and unattractive. The monopoly hold they had on financing has come to an end, certainly in the middle and lower middle market.

Transaction wise, we are seeing deals done with better terms, lower leverage, higher equity cushions and more attractive pricing. This is not to say all direct lending is easy and all managers will have great outcomes. In the parts of the direct lending market where we prefer to focus, lower middle market and some middle market, companies with EBITDAs up to $60 million, using managers with strong credit underwriting, covenants, financial tests and a focus on first dollar out, top of the capital structure deals, we believe the outlook remains strong. Moving higher in transaction sizes and into more complicated capital structure adds unnecessary risk.

Outlook: We expect conservative lower middle and middle market direct lending to deliver 10%-14% net.

Real Estate

Location, location, location is now equally as important as structure, structure, structure. No space is facing more challenges and presents more opportunities than real estate. COVID, the changing downtown city work environment and rising interest rates have created chaos in the core business district (CBD) office market. Higher interest rates and supply shortages have created imbalances in the home ownership and rental market. The workplace has rapidly changed post-COVID. There is a very measurable demographic shift from North to South. Supply chains have evolved to meet changing consumer needs. The digitization of everything has created demand for massive data facility capacity.

All of this is to say, in many ways, the shape of the real estate market has changed, while the way money is made in real estate has stayed the same.

It is impossible to cover all sectors and all markets here. We do believe there are specific sectors that have tailwinds.

The need for senior housing is acute. The wall of baby boomers and beyond is massive and the supply of housing is nowhere near enough. Everyone is talking about the Cloud and AI. The cloud resides on servers, not the sky. Those servers live in data centers. The need for data centers is great and only growing. Grocery anchored retail has survived the idea that Amazon and Instacart were going to bring people their groceries. What we found was, people still want to see their produce and proteins before they buy them. An adjacent effect of constrained housing is that student housing is in great demand. Parents still want their kids to go to school and kids still want the college experience.

In the more traditional sectors of Industrial, Multifamily and Office the focus is going to have to be on strong operators, good capital structures and conservative balance sheets. Not every geography feels investable. Allocating capital where there are strong demographic trends and managers with an understanding of local markets will be very important.

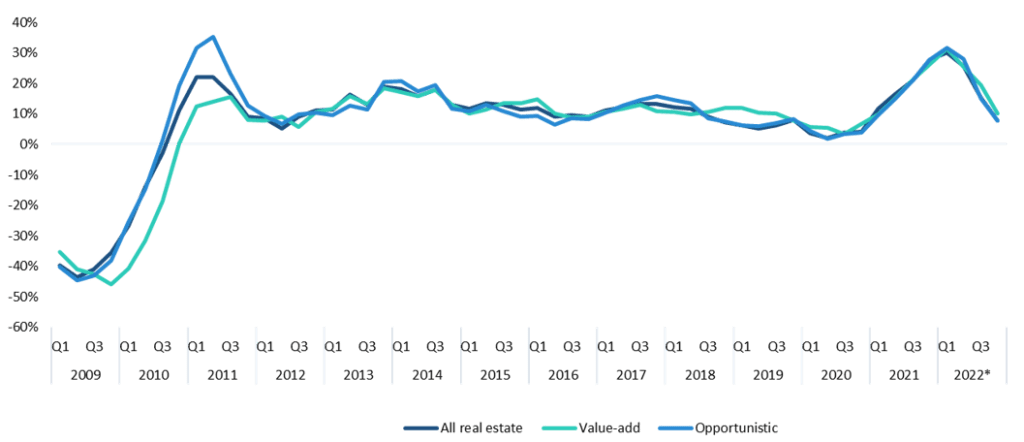

Outlook: We expect real estate to return to historical normalized returns. The above chart highlights the unrealistic and unsustainable return period we just exited from. Core should deliver 6-8%, value add should deliver 10%-14% with a 1.5-1.6x multiple and Opportunistic should deliver 15%-25% with a 2-2.5x net multiple.

Real Assets

For the purposes of this report, we will discuss Infrastructure, Farmland and Timberland.

Infrastructure- The capital needs for infrastructure only grows as the target surface of Infrastructure expands. It is no longer just ports, bridges and tollways. Infrastructure is now Renewable Power, Data and Communications, Transportation and Water/Bio. 2022 was an extremely busy year from a deal perspective. We saw a large number of deals in the sub $500 million space, but the $1 billion plus size deal market is still where the majority of capital was deployed. Building out transmission and delivery capacity for the renewable energy space is a huge space. We discussed data centers in real estate, but this sector bridges RE and Infrastructure. Infrastructure investors focus on the larger data centers. The need in North America is great and it is even larger in Europe.

Outlook: As with other asset classes, as a result of higher financing costs, we expect to see deals done with lower leverage and lower purchase multiples. We also expect Infrastructure to continue to demonstrate an inflation resistant return profile with downside protected cash flow streams underpinned by contractually obligated recurring revenue. Core Infrastructure should deliver 6%-8% and a diversified portfolio of global infrastructure investments should deliver 8%-12% with great inflation resiliency.

Farmland- We focus mainly on high quality row crop opportunities in the US Midwest. This is a capacity constrained market and deploying capital requires skill and patience. Auction prices remain extremely solid. Appraisals continue to be very firm if not higher. Auxiliary income sources, especially solar lease options and leases continue to pay meaningful extra income. Farm/Land rental incomes continue to grind higher. We expect this part of the Farmland asset class to continue to deliver 10%-14%.

Timberland- 2022 was an active deal year for timberland properties. Pent up housing demand will continue to drive the lumber construction story. Whether it is new construction use or renovation/remodel use, lumber demand should see increased demand over the next three to five years. A growing increase in engineered wood products, especially cross-laminated timber (CLT) in low to mid rise construction, is extremely promising. The biggest problem is getting enough of it to market. From an ESG point of view, forest products demand has remained strong given that it is a carbon-negative building material and more environmentally friendly than cement and steel. Timberland supply/demand dynamics also continue to affect the return profile. We are seeing tight log supplies in the U.S Pacific Northwest, Chile and Australia. We expect a well diversified timberland portfolio to continue to deliver 8%-12%.

Summary

There is no way to predict the next virus, global conflict, election outcome, energy shock or other possible market disruption. We think this is a period where our North Star should be the basic ideas that we always focus on; Pacing, Portfolio Construction, Patience. At the investment level we will remain focused on capital structures, pricing, fund structures, manager experience and realistic expectations.

©2023 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.