Aoifinn Devitt – Chief Investment Officer

As the 22nd FIFA World Cup kicked off in Qatar, it is not just the seasons that seemed upside down. Some early upsets in the first round of games, such as the defeat by Saudi Arabia of Argentina, seemed par for the course for 2022’s propensity towards surprise.

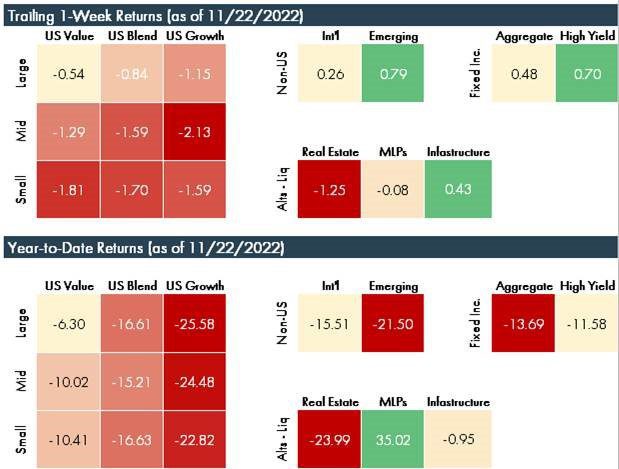

Last week, market action was more subdued than the previous week – as investors seemed more sober in the face of the prospect of further rate rises and the fallout from the FTX bankruptcy continued to be felt. Oil was significantly softer amid concerns for economic growth (briefly falling below $80 per barrel for the first time in three months) and October PPI data was below expectations.

Source: Morningstar as of 11/23/2022

Earning surprises were fewer than expected, although corporate fortunes continue to diverge. There was a split between tech stocks, on the one hand, who continue to shed staff and recalibrate their plans for growth (now including hardware manufacturers such as HP and Dell) and retailers who note the still-resilient consumer who continues to beat the odds.

Just as import price indices were showing four months of steady declines, it is clear that the dollar is showing some meaningful weakness now. So far in November,the dollar has fallen by more than 4% from its 20-year high, with all eyes on the prospects for inflation to decelerate, representing another upset to long-held trends this year.

Meanwhile, the complex web of governance failures behind FTX’s bankruptcy continued to unravel, with poor accountability and a lack of controls emerging as the culprits at this stage. In the forum of Twitter, the drama following the Elon Musk takeover continues to unfold with the company apparently facing a mix of high debt levels, falling revenues and persistent costs. Over the course of this week, there were rumors it would “go dark” and then it did not, but the situation echoes that of FTX in terms of the risk of key person reliance.

As Thanksgiving approaches, the week is somewhat quiet, with investors perhaps putting their feet up as an exhausting and turbulent year nears an end. It is to be hoped that Thanksgiving dinner conversation doesn’t turn to house prices – existing home sales fell for the ninth straight month in October, declining a further 5.9% month on month. The national median home price has been rising though, but higher mortgage rates are placing a limit under demand.

We wish all of our readers a happy and peaceful Thanksgiving break, and look forward to the build to year end when we return next week.

© 2022 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.