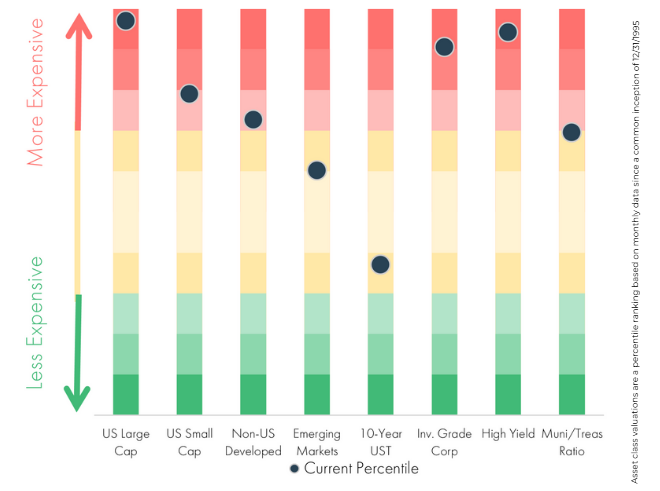

August Observations

Broadening the Rally

U.S. equities rose in August, but leadership shifted from tech to smaller-cap and cyclical stocks. The Russell 2000 (+7.1%) led the way, while the S&P 500 (+2.0%) and Nasdaq Composite (+1.6%) posted more modest gains. Q2 earnings supported sentiment, with S&P 500 earnings per share up approximately 12% year-over-year and a broad set of companies beating expectations. Sector rotation was evident as Materials and Healthcare topped the leaderboard, while Technology and the “Mag 7” lagged amid growing skepticism about lofty AI-driven valuations. Developed markets posted modest gains, with Europe lagging U.S. peers on weak earnings and political headwinds, while Japan outperformed on strong cyclical leadership and macro tailwinds. Emerging markets fared better, led by China’s sharp liquidity-driven rebound and strength in Asia broadly, though Korea was a notable laggard. Yields continued to edge higher, weighing on bonds, as markets digested fiscal and geopolitical risks alongside evolving central bank expectations.

Economic Data: Mixed Signals Continue

Labor market weakness dominated headlines in August, with July payrolls sharply disappointing and prior months revised lower. Still, growth concerns eased as Q2 GDP was revised higher to 3.3% and PMIs beat forecasts, led by manufacturing. Inflation stayed in focus as a sharp jump in producer and import prices reignited tariff-driven worries by month-end.

Fed Strikes Dovish Tone at Jackson Hole

At the Fed’s annual Jackson Hole meeting, Fed Chair Jerome Powell noted that both labor market supply and demand have softened. While Powell stated that the labor market “appears to be in balance”, he cautioned that downside risks to employment were rising. With inflation risks tilted up and jobs risks tilted down, Powell emphasized the challenging situation, but indicated their restrictive policy may no longer be warranted, keeping rate cuts in September firmly on the table.

Asset Manager Commentary

Private Capital Manager

Over the first half of the year, the contribution to GDP growth from data center investments was roughly the same as the contribution from consumer spending. The contribution from consumer spending has been decreasing, and the contribution from data center construction has been increasing.

Real Estate Manager

REITs have improved in Q3 after a mixed first half, with defensives leading early and growth themes later. This manager’s outlook favors a slowdown scenario (40% probability), where REITs could outperform equities, though recession and stagflation (25% each) remain notable risks.

Infrastructure Manager

Global nuclear power currently supplies about 9% of electricity, with the U.S. at nearly 18%, and the existing fleet of ~440 reactors is projected to grow to ~500 by 2030, alongside 400 more planned. Looking ahead, small modular reactors (SMRs) represent the most promising innovation: with smaller, flexible designs (20–300 MW), they can open new markets, reduce construction risks, and serve high-demand sectors, though they still face cost and commercialization challenges.

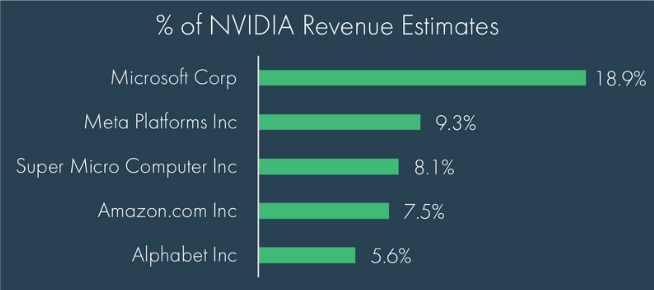

Chart of the Month

NVIDIA’s recent earnings report confirmed that spending on artificial intelligence is alive and well, though estimates for future growth were tempered by uncertainty on access to China. Concentration of revenue sources remains significant, with the company noting 39% of last quarter’s revenue came from two unnamed customers.

© 2025 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.