Aoifinn Devitt – Chief Global Market Strategist

Illinois is currently in the middle of a 17-year cicada brood which is overlapping with the normal emergence of a regular brood. The last time this brood emerged was 2007. The experience of this phenomenon is quite divergent – in some areas tree barks are covered while sidewalks are littered with them, while other are relatively clear. In recent weeks they have been divebombing pedestrians and landing on them with their somewhat poor vision rendering them slow and sluggish in reactions. The noise, though, is pervasive. It is a buzzing that ebbs and flows in intensity like an electronic force. The interesting part is that it fades into the background easily, unless you decide to hear it, then it is hard not to hear it everywhere.

2007 seems a lifetime ago – as it was pre-great financial crisis, pre-credit crisis, pre-unprecedented bank failures and government bailouts. Just like the cicada life cycle, it is natural that thoughts have turned back to whether we are due another brood of credit defaults and, just like in Illinois currently, the background noise occasionally rises to a crescendo.

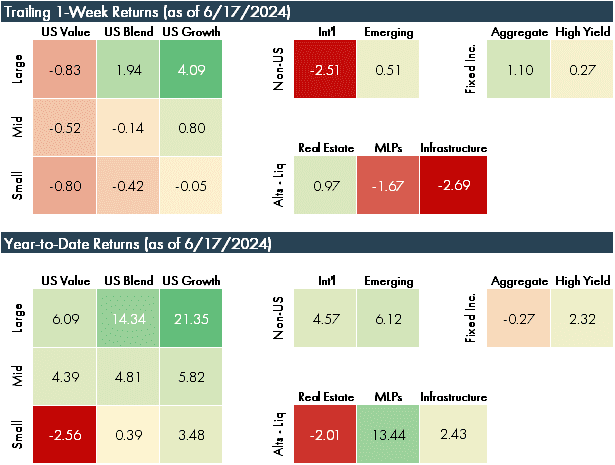

Last week the noise was that of the market breaking new records on the back of weaker inflation data and a Fed that clearly is signaling the way down from here. The mood is one of cautious optimism, as we move beyond the soft-landing thesis into contemplating the next phase of stimulus and growth. Around the world the starting gun has been fired on that growth – or at least damage control. After months of restrictive monetary policy there is concern – in Europe and Canada at least initially that consumers will start to buckle. Central banks are taking no chances now, and an initial rate cut is already in the bag for both the ECB and the Bank of Canada.

Meanwhile tech stocks continued their ascent and Nvidia is now the largest company by market value, surpassing Microsoft, and stock markets were otherwise buoyant as markets close for the Juneteenth holiday.

Election chatter is mounting, but the rhetoric can’t dampen the story being told by the numbers. Despite some fractures appearing in the shape of the employment numbers and the health of the consumer, the mood remains buoyant.

So what are some of these fractures? In the case of the employment numbers, the net additions are part time roles, while full time roles are actually falling, and while there are net job additions – the majority of these are in the healthcare and government sectors, and not more broadly across the board. The consumer, meanwhile, is experiencing some uptick in defaults in areas with floating rates – such as credit cards and consumer (e.g. car) loans.

As summer moves into full swing, we will continue to watch these fractures to see if they widen. Some say the cicadas have peaked. Time will tell if the consumer has too.

DISCLOSURES

© 2024 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.