By Aoifinn Devitt, CFP® – Chief Investment Officer

Just as the weather started to cool down, inflation has been picking up. The latest inflation figures released this week showed a small uptick in month-on-month inflation, largely attributable to energy price rises. Geo-political wrangling around oil supplies has led to a creep upwards in pump prices and consumers, and corporates, are again likely to see a squeeze. A consumer squeeze comes amid a time of mortgage rates at 22-year highs and a perception of affordability in retreat. It is the latest in a series of mixed data which can be read in many ways. The consensus response to the inflation data is that it is not “severe enough” to cause the Fed to experience alarm. So a pause in rate rises is likely to continue.

It is a reminder, however, that “it ain’t over ‘til it’s over”. The ride down from our recent inflationary peaks will be that precarious descent that we spoke about a few weeks ago – the danger of losing one’s footing and of moving too fast is real. We shouldn’t, perhaps jump to conclusions about inflation being controlled, the landing being “soft” or the housing crisis being averted. Or even around the changing structural backdrop of employment, participation and the new gig economy. Maybe none of these is an “emphatic” change such that things are different this time. It is a reminder that economic contexts, like fire itself, are complex and volatile.

The European Central Bank also knows it “ain’t over” even if the Fed may feel it is. The ECB just raised its rates by 25 bps this week and the Euro actually fell – the loss of confidence in economies outside the US has continued and this has been somewhat perplexing. This may be, in part, the absence of tech as a key driver of most European stock market indices, and the proximity to Ukraine is definitely a factor. The result, therefore, is an imbalanced global recovery and a somewhat skewed global stock market picture.

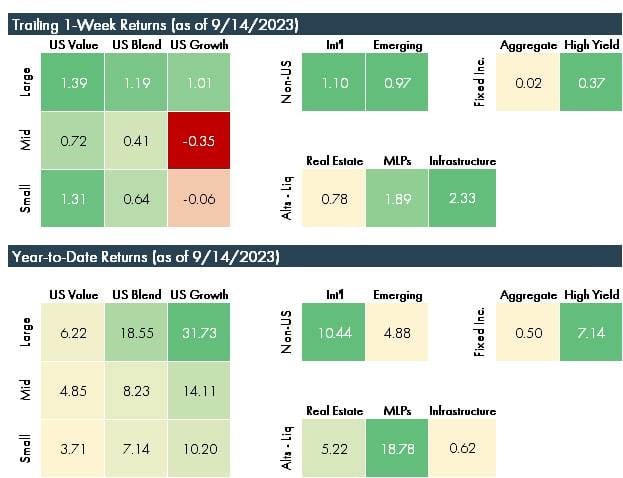

Equities have been largely sideways in the past week, and many investors have looked at the traditional status of September as a poor month for market performance. The “September effect” has apparently been getting worse in recent years, but the market has been softer in 26 out of the last 30 years in the week after September 15 options expiration and the run up to October tax year selling.

A Fidelity strategist notes that “It is the only month of the year in which there have been fewer rising months than falling ones since 1950. The average return over the 73 years is also the worst of any month at -0.8%.”[1]

As the days shorten and the leaves start to turn, we are poised to look for narratives and economic theses that also take on a new hue. Bonds, decent returns on cash, the “magnificent seven” stocks and a buoyant consumer . . these are all narratives that may not hold. A freak fall storm might just blow them all away.

[1] https://www.fidelity.co.uk/markets-insights/markets/global/is-september-really-the-worst-month-for-investors/

© 2023 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.