“Go Big or Go Home”

The Fed decided to go big this month by cutting rates by 50 basis points – fulfilling the expectations of the betting market but defying those of most pundits who had expected a modest start to coming down the mountain, instead of a bold one. So what does this mean for markets and what can we read behind the lines of this move?

Data: The Fed has stressed for months that any move will be data dependent – so clearly the data on employment and inflation is aligning to create confidence that the latter is vanquished, while employment is starting to look like a concern. Chairman Powell, in his speech, essentially acknowledged that the Fed could shift to the employment part of its mandate, citing reassuring data on inflation being subdued and stressing: “There is thinking that the time to support the labor market is when it is strong, and not when you begin to see layoff.”

Nothing to see here: Only 9/113 economists surveyed by Bloomberg anticipated a 50 bps cut, with the others expecting only 25 bps – which begs the question that what does the Fed see that they don’t? Are markets actually as resilient as they seem? We have recently seen a heightened interrogation of the veracity of the employment data – the recent revision only underscored this, and the large number of “quiet” redundancy rounds – often accompanied by non-disclosure agreements – are evidence of this, along with “noise” created in the numbers by a variable participation rate, recent migrants and a rising gig economy.

Is the Fed OK? The swift turnaround in approach, and the size of the cut, had commentators wondering if the Fed was scrambling and behind the curve again (bearing in mind that it had raised rates by four consecutive moves of 75 bps between June and November 2022) – but Chairman Powell provided assurance that this was more along the lines of a catch up cut rather than a drastic alarming signal.

The Political Angle: The other inevitable takeaway was that this cut was strategically timed to be politically opportune – particularly for the incumbent administration by boosting the economic mood. It could of course have the opposite effect – sowing seeds of doubt as to the state of the economy – if it wasn’t for the fact that it was delivered with such defiant cheer. Both campaigns have, predictably, seized upon these counter-narratives, and markets continue to digest what message should be ascendant.

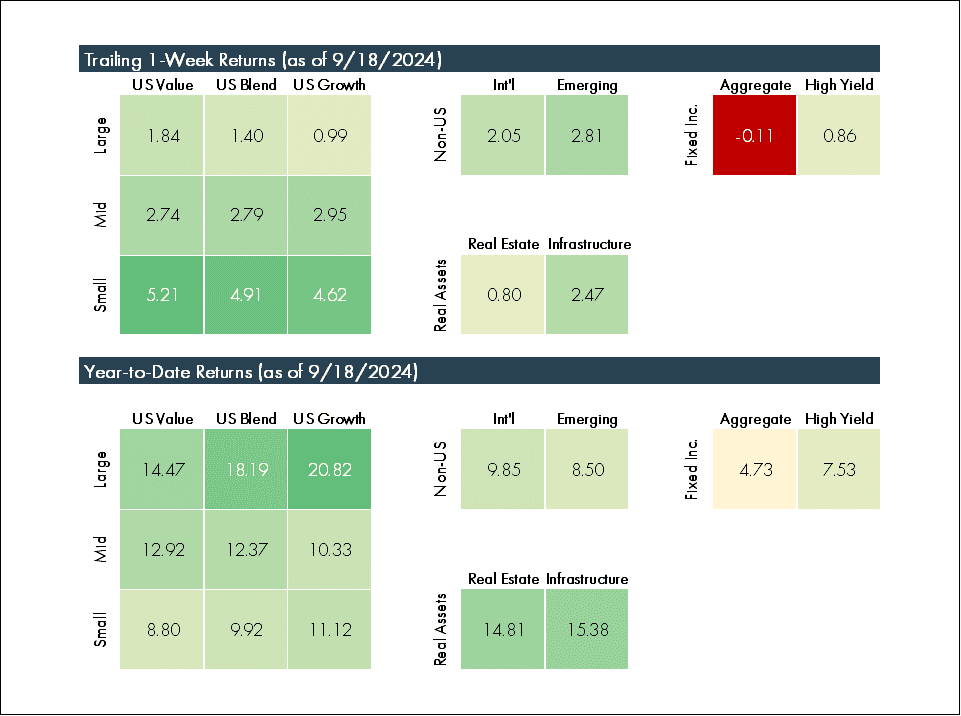

For investors markets are already receiving the data very positively:

Consumers now can look forward to lower mortgage rates, interest rates on loans and very likely a boosted economic environment and stock market momentum. We can expect more focus on what perceived “cracks” led to the Fed’s conviction on this occasion, and as the election countdown passes the 50 day mark, more noise and speculation around the likely outcome and its impact on the economy.

© 2024 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.