A step-by-step guide to the first 100 days after divorce

After months of negotiating, planning, and worrying, you receive that life-changing phone call from your attorney: your divorce judgment has been officially signed and entered by the court. It’s normal to feel relief, sadness, or uncertainty at this milestone, sometimes all at once.

While the emotional transition takes time, the financial steps you take in the first 100 days after divorce can have a lasting impact on your independence and security. This is a crucial window to protect what’s yours, avoid costly oversights, and begin building a new chapter with confidence.

Building new routines (physically, emotionally, and financially) can feel overwhelming at first. But by taking the right actions in the right order, you can set a strong foundation for your financial future.

In this guide, I break down the process into manageable milestones: what to address immediately, within 30 days, 60 days, and by day 90, plus a printable checklist you can reference anytime.

Why taking action during the first 100 days after divorce matters

Divorce is not just an emotional event, it’s a financial one. Income may change, accounts require separation, and matters like insurance, credit, taxes, and estate plans all need attention. Many activities are time-sensitive and small oversights early on can lead to unintended consequences later.

The goal of the first 100 days isn’t to have everything figured out. It’s to reduce financial risk, gain control, and create stability one step at a time.

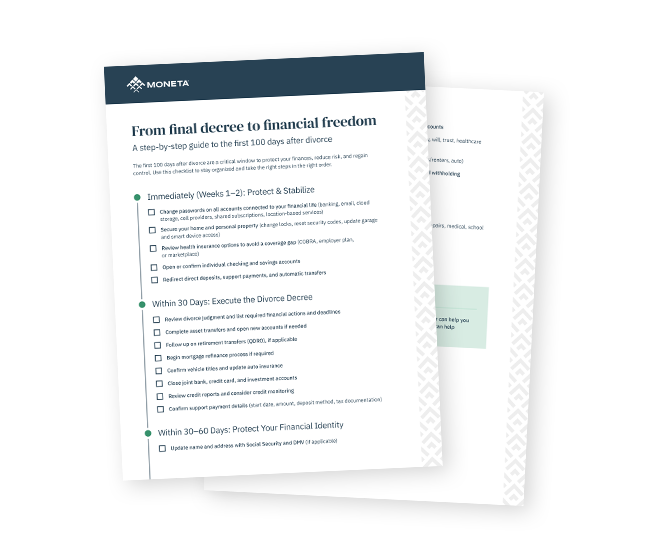

Immediately after divorce: Protect and stabilize your assets

In the first two weeks after divorce you might experience a lot of change. It’s important that your attention is on security, access, and continuity.

- Protect your digital privacy (and financial access). Review all online accounts tied to your financial life, from banking, email, and cloud storage to cell phone providers, shared subscriptions, and location-based services. Updating your passwords can help you maintain control over your accounts and give you peace of mind.

- Secure your home and personal property. If you haven’t already, change the locks on your home, reset security system codes, and update access to garages, storage units, and smart devices. In addition to safety, securing your physical property can help protect your assets and reduce risk.

- Review your health insurance to avoid a coverage gap. If you were on your ex-spouse’s plan, it’s important to consider your options right away. This may include COBRA coverage, an employer plan, or marketplace coverage. A financial advisor can assist in mapping out the cost tradeoffs and connect you to a qualified insurance specialist.

- Establish individual banking and cash flow. Confirm that all direct deposits, support payments, and auto-transfers move through these new accounts. Ensuring your cash flow is fully under your control is a key first step in gaining financial stability.

Within 30 days after divorce: Execute your divorce decree and reduce risk

It’s during the first month after a divorce is finalized that you’ll want to review your divorce decree and develop a clear understanding of your obligations.

- Review your divorce agreement through a financial lens. Carefully read the judgement and make a detailed list of the financial changes you need to make and their deadlines. Some of those changes could include:

- Asset division: A financial advisor can assist you in evaluating what assets must be transferred, what you will keep, and determining if you need to open new accounts to receive assets or to separate accounts.

- Retirement transfers (QDRO): If a Qualified Domestic Relations Order (QDRO) is required, follow up to be sure it’s completed, court-approved and accepted by the plan administrator.

- Housing: If you need to refinance your home to remove your ex-spouse from the mortgage, contact a mortgage broker to get started.

- Vehicles: Confirm the titles and registration match the agreement and update insurance accordingly.

- Close all joint accounts and review credit reports. Closing joint credit cards, bank accounts, and investment accounts as soon as the agreement allows can help protect you against charges or missed payments that can damage your credit. Reviewing your credit report and setting up credit monitoring can ensure you don’t have any joint obligations you’ve forgotten.

- Handle your support payment logistics. Support payments are often a big source of income, so it’s beneficial to quickly establish the parameters of those payments. Common considerations include acknowledging when the payments will start, understanding the amount of each payment and when you will receive it, establishing where they’ll be deposited, and knowing what documents you should retain for your taxes.

Within 30-60 days after divorce: Protect your financial identity

During the second month following your divorce, you can move toward addressing the next level of priority items.

- Update your name (if applicable). Contact the Social Security Administration to update your name and address, followed by the DMV to update your driver’s license. With new proof of identification, you can make changes with your employer and financial institutions. You’ll typically need a certified copy of your divorce decree for these updates.

- Update beneficiaries and estate planning documents. This is one of the most important and commonly overlooked steps after divorce. Your wishes may have changed and updating the following ensures they are honored moving forward.

- Beneficiary designations on retirement accounts, life insurance, and investment accounts

- Powers of attorney, will, trust documents, and healthcare directives

- Review insurance needs beyond health coverage. Evaluate what insurance you have and what types of insurance you now need such as life insurance (especially important if you have support obligations or children who depend on your income), disability coverage, homeowners/renters insurance, and auto insurance policies. Do you have policies that need to be separated or do you need to purchase policies?

- Address tax considerations early. Changes in filing status, dependents, withholding, and asset transfers can all have tax implications. Identifying these changes early can help you avoid surprises when tax season arrives.

Within 60-100 days after divorce: Build your new budget

You’ve already covered a lot of financial ground by day 60, so the final month can be spent turning all of the uncertainty you’ve likely been feeling into a concrete plan. A big step you can take is to set your personal post-divorce budget.

Look at your finances with fresh eyes and make a plan that’s realistic for you. Start with the essentials, like housing, childcare, insurance, and paying down debt. It’s important to account for irregular expenses like car repairs, school costs and medical bills, maybe even a vacation, especially if income is irregular. Working with a financial advisor can help you consider these factors.

Handling core priorities can reduce your financial risk

The first 100 days after divorce is a pivotal time. By handling the core priorities of protecting your accounts and your identity as well as executing the terms of the divorce decree, women can reduce their post-divorce financial risk. Taking these steps in a manageable timeline can help you regain control and move forward with confidence after a major life change. Seeking support from trusted professionals can make the transition smoother and help you protect your interests throughout the process.

FREE PRINTABLE CHECKLIST

First 100 Days After Divorce

Fill out the form to receive your financial freedom checklist.

© 2026 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified. Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.