By Tim Side, CFA – Director of Investment Strategy

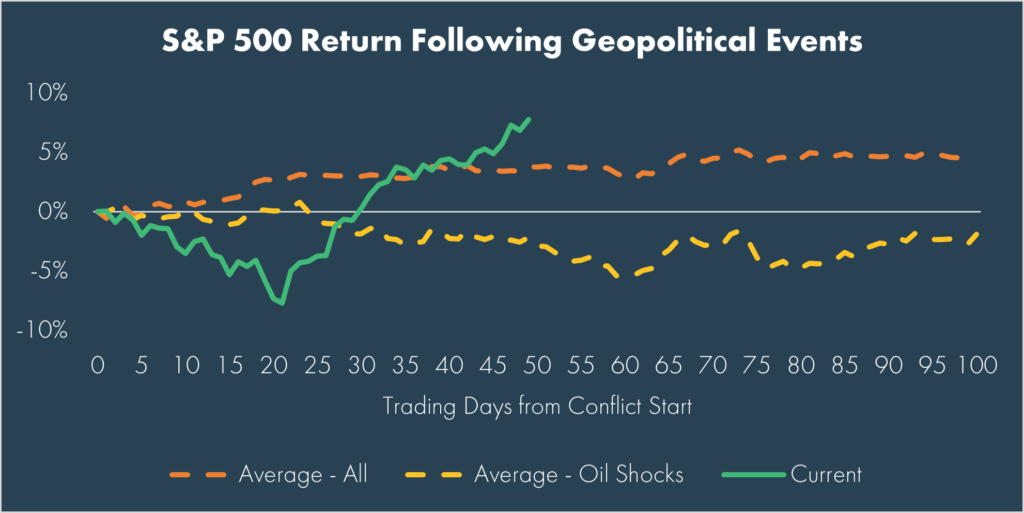

For many years, we’ve advised clients that while geopolitical events often cause short-term dislocations, they rarely have a lasting impact on markets and staying disciplined remains key to investor success. We don’t provide this advice because we are clairvoyant of how long or impactful geopolitical events such as the conflict in the Middle East events will be, but simply because that is historically how events have played out over the last century. In this case, while the initial decline was sharper than average, the speed and magnitude of the subsequent recovery quickly outpaced historical averages.

While the initial recovery at the end of March was, in many ways, justified by a ceasefire agreement that resulted in a sharp decline in oil prices, the sustained market rally has many scratching their heads, as the Strait of Hormuz effectively remains closed and, as we write, 1-month Brent oil futures are trading around $104 per barrel. While there are hopes that the US and Iran are nearing a deal to open the Strait, we’ve seen day-to-day changes to the negotiations and make no projection on how close both sides are to an actual deal, though we do see it as a positive signal that negotiations are continuing.

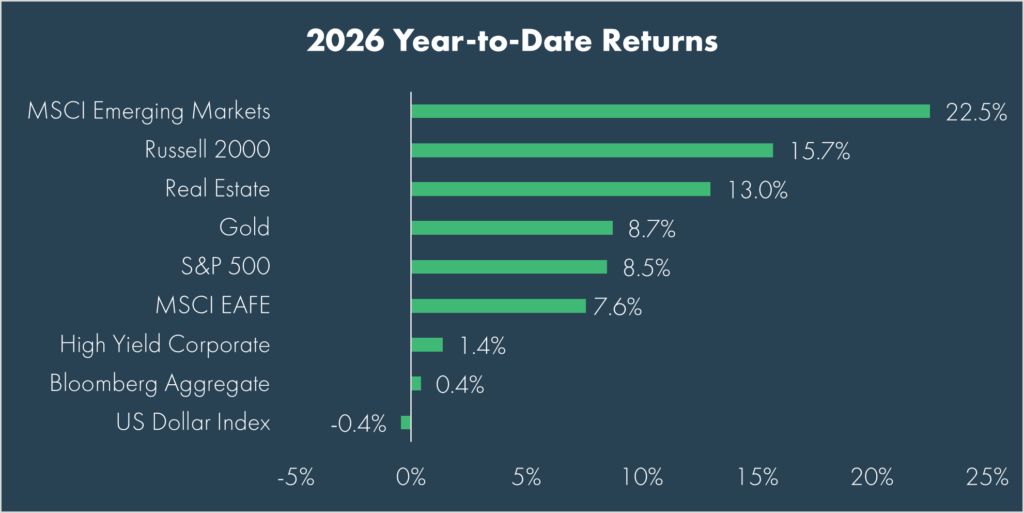

Clearly though, stocks have largely moved on from the war and the overall upward market bias has been sustained by exceptional earnings in the both the U.S. and abroad. There’s a lot to digest in the world right now, but for this blog post, we’ll aim to unpack what those earnings numbers look like and what are key areas to watch going forward.

Love it or hate it, artificial intelligence is driving a massive boom in infrastructure spending. The investments in AI infrastructure (chips, data centers, power, etc.) by the four major hyperscalers (Microsoft, Amazon, Meta, and Google) alone are mind-boggling, with capital expenditures coming in at $358 billion in 2025 and expected to exceed $600 billion 2026, $800 billion in 2027, and approach $900 billion in 2028. To put this in perspective, this level of annual spending is on par with the individual GDPs of Belgium, Sweden, Ireland, and Taiwan.

Setting aside concerns about the profitability of these investments, the accounting nature of capital expenditures that reduces the impact on earnings, the circular nature of some of these investments, and AI all-together, these investments are having a real impact on companies’ revenues, especially semiconductor companies.

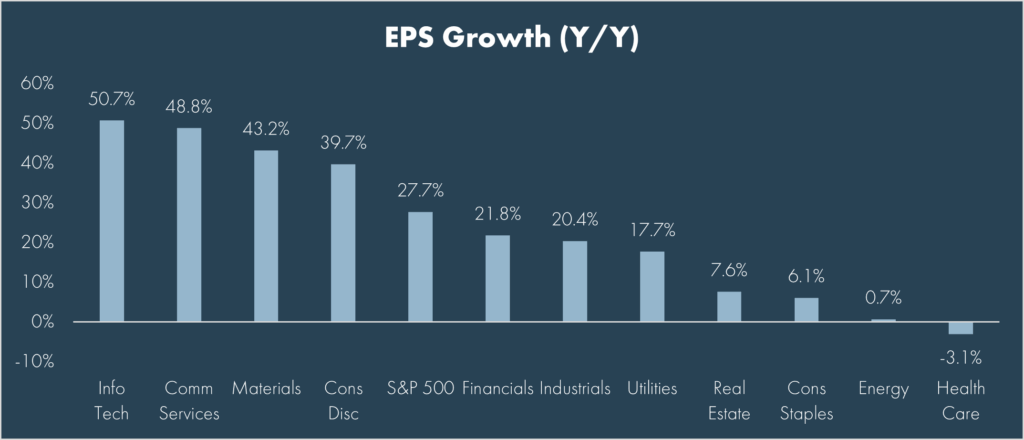

Through last Friday, the S&P 500’s blended Q1 earnings growth rate is 27.7% according to FactSet. 27.7%! That is relative to an expected 13%-14% at the start of earnings season. As of the report, 89% of companies had reported results so while the final Q1 number is subject to change, we are on track for a massive boost in earnings; a key driver behind recent performance.

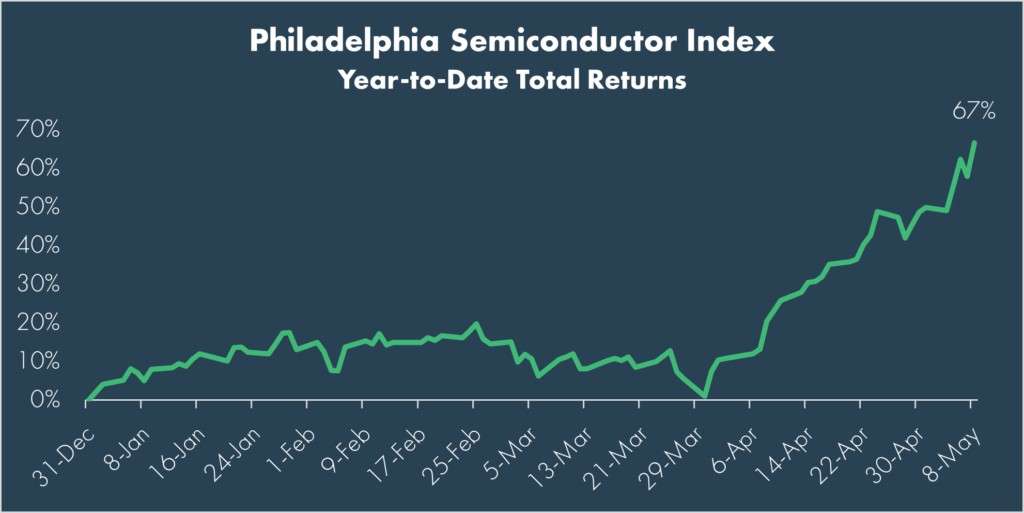

As seen in the chart above, the overall earnings growth rate has primarily been driven by tech sectors, particularly within semiconductor stocks, a direct beneficiary of the massive AI spend. These semiconductor stocks have been in focus for investors as earnings estimates are expected to double from 2025 to 2027, sending chipmaker’s stocks soaring in recent weeks:

In fact, within the S&P 500 index, more than 25% of net income growth on a year-over-year basis has been driven by semiconductor stocks. Additionally, FactSet estimates that if NVDIA (est) and Micron earnings were excluded from Q1, the blended earnings growth rate for Information Technology would fall to “only” 28.5% from the current 50.7%.

Yet, despite this concentration, it is notable that segments such as materials, financials, industrials, and utilities are also seeing double digit earnings growth rates. While much of the breathtaking rally can be attributed to AI spending, it is nice to see that that gains are not solely limited to those benefiting from the AI spend.

So where do we go from here?

First things first: the momentum trade is extremely strong right now, and betting against it can be a dangerous thing. As noted above, this is not a rally based on investors simply paying more for stocks (i.e. multiple expansion); companies, especially, but not exclusively, chipmakers, are improving profit margins and growing earnings. While there may be pockets of the market that have become stretched, there are strong fundamentals behind the current rally.

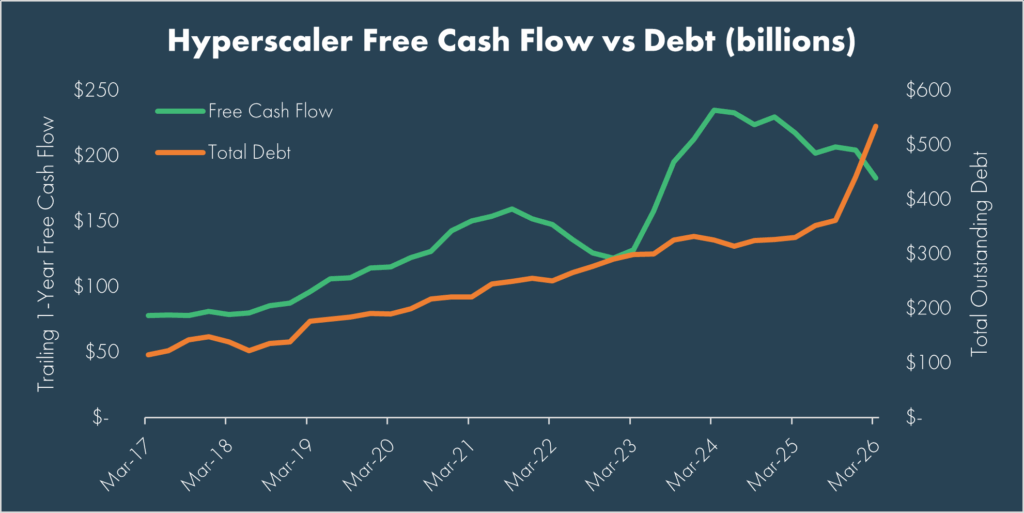

But, as always, risks remain. We somewhat passed over these above, but as prudent investors, we cannot ignore them. The hundreds of billions of dollars being spent by hyperscalers are being funded by a combination of free cash flow and debt – both of which remain key items to watch, as they are turning once immensely profitable and asset light companies into asset heavy companies making huge bets to ensure their profitability continues.

As with any investment, there is a risk that it fails to meet its return objective. Currently, the market has significant interest in these AI investments paying off. Not only are the billions in capex propelling broader earnings higher, these four hyperscalers alone make up 19% of the S&P 500 based on market cap – any hiccup in the success of these investments would have broad ramifications.

Is the rally overdone? Possibly, but “possibly overdone” is not the same as “time to step aside,” and this is where discipline and patience earn their keep. Two recent observations capture the tension well.

On one hand, Bloomberg’s John Authers notes that “when a rally is moving like this, it can be dangerous to try to stand in front of it“. On the other hand, Strategas’ Chris Verrone reminds us that “parabolic charts often correct with similar intensity (not sideways).” Momentum is a powerful force, and history is unkind to investors who try to time its end, but often, when these rallies do unwind, they tend to unwind quickly.

Both can be true at once. There are fundamental tailwinds behind the rally, but the timing of any reversal is unknowable. As long-term investors, we don’t pretend otherwise. We trust the process and maintain enough exposure to keep participating, without becoming so over-exposed to the trade that a correction of “similar intensity” would do lasting damage.

© 2026 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment adviser does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

Return data for geopolitical events used as available. Conflicts included are: Israel Iran War (2025), Hamas Attack on Israel (2023), Russia Invasion of Ukraine (2022), Crimea Conflict (2014), U.S. Invasion of Iraq (2003), September 11 Attacks (2001), Kosovo War (1999), Iraq Invasion of Kuwait (1990), Iran-Iraq War (1980), Arab Oil Embargo (1973), Cuban Missile Crisis (1962), Pearl Harbor Attack (1941), and the German Invasion of Poland (1939).