With year-end quickly approaching, taxpayers still have a few weeks left to plan ahead with strategies that could provide meaningful tax savings. We included below several planning opportunities to consider before December 31.

Gift Long-Term Appreciated Securities

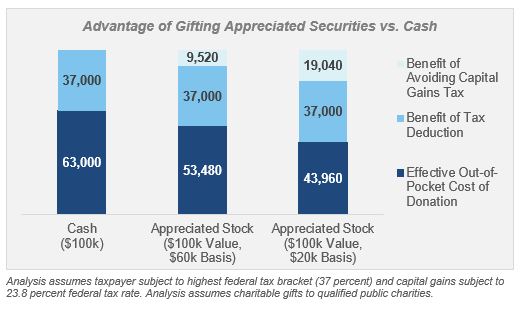

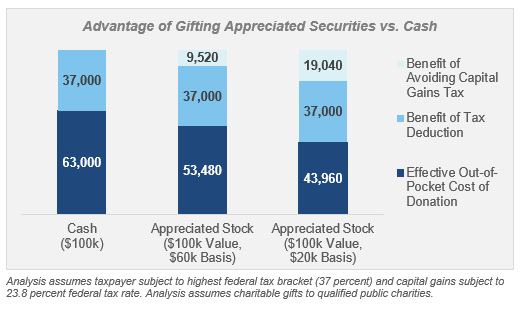

With equity markets near all-time highs, investors with taxable accounts may hold highly appreciated equity positions. From a tax planning standpoint, gifting long-term appreciated securities is an efficient charitable-giving strategy. With this, the charity receives the same economic benefit as a cash donation, while the taxpayer receives a tax deduction for the full market value of the gift and avoids paying capital gains taxes on the gifted security.

Investors with a portfolio overweight to equities, due to significant equity market gains, may use charitable gifting as a means to rebalance back to target weights. In doing so, an investor can meet philanthropic goals and avoid selling appreciated equities to return to a desired target allocation.

Keep in mind, gifts of long-term appreciated securities to qualified public charities are limited to 30% of adjusted gross income (AGI), while similar gifts to a private foundation are limited to 20% of AGI. Charitable gifts in excess of the AGI limits result in a charitable carryforward that can be used over the next five years.

Accelerate Charitable Giving (“Bunching”)

Itemized deductions have changed substantially due to the Tax Cuts and Jobs Act of 2017:

- The standard deduction has nearly doubled.

- Personal exemptions have been eliminated.

- The state and local tax (‘SALT’) deduction is now capped at $10,000.

- Mortgage interest is deductible on qualified residence debt up to $750,000 for new mortgages (post December 15, 2017) versus a previous $1,000,000 limit.

- Interest paid on a home equity line of credit (HELOC) not tied to home improvement is no longer deductible.

As a result of these significant changes, more taxpayers will now take the standard deduction rather than itemizing deductions. The Joint Committee on Taxation estimated the number of taxpayers claiming itemized deductions would fall from nearly 47 million in 2017 to 18 million in 2018.

Charitably inclined taxpayers may benefit from a “bunching strategy” whereby several years of charitable gifts are made within a single tax year to produce a large itemized deduction total with the standard deduction to be taken in subsequent years.

In the example below, a married couple has $19,000 of non-charitable itemized deductions and $30,000 of annual charitable gifts. As the standard deduction is $24,400 for married filing jointly taxpayers, the first $5,400 of charitable gifts in this example does not produce tax savings because it merely increases the itemized deduction total to equal the standard deduction (the remaining $24,600 of charitable gifts does produce a net tax benefit). Conversely, this couple could choose to “bunch” three years’ worth of charitable gifts into a single tax year. The couple would itemize deductions in year one and take the standard deduction in years two and three. As illustrated below, the “bunching” strategy produces a three-year deduction total that is $10,800 higher.

Accelerated charitable giving may also be beneficial for taxpayers who have higher-than-normal taxable income in a given year, as increased charitable giving shields a portion of income from otherwise being taxed at a higher rate.

In some instances, taxpayers may wish to utilize this strategy without necessarily giving this higher amount to charities all in the same year. In such cases, a donor-advised fund can be particularly helpful to get the current year tax deduction while allowing the donor to make grants at a pace of their choosing.

Satisfy Required Minimum Distributions (RMDs) using the IRA Charitable Rollover

Taxpayers older than age 70½ are required to take minimum distributions from retirement accounts (except for Roth IRAs). Under the Qualified Charitable Distribution provision, taxpayers older than age 70½ can transfer up to $100,000 each year from an IRA to qualified 501(c)(3) organizations (donor-advised funds, private foundations and supporting organizations are excluded).

The taxpayer must be at least age 70½ as of the date of the charitable transfer. A qualified charitable distribution neither counts as an itemized deduction nor as taxable income. This provision may be helpful to charitably inclined individuals who now receive a greater tax benefit from the increased standard deduction rather than itemized deductions.

Harvest Losses

Review unrealized gains and losses in taxable investment accounts and harvest losses where available. Realized losses can offset other realized gains. To the extent realized losses exceed realized gains, net realized losses can offset up to $3,000 of ordinary income with any remainder resulting in a loss carryforward to be used in future years.

Beware of the “wash sale rule” stating a loss cannot be realized for tax purposes if a substantially identical position was bought within 30 days before or after the sale. As a practical example, an investor could sell an actively managed equity fund and redeploy the sales proceeds to an equity index fund. In doing so, the investor recognizes a tax loss while also keeping similar, but not identical, portfolio exposure.

Admittedly, as 2019 has been a remarkable year for nearly all asset classes, investors may have limited opportunities for loss harvesting this tax year.

Analyze Mutual Fund Estimates for Year-End Capital Gain Distributions

Mutual funds are required to pass along capital gains to fund shareholders. Regardless of whether the fund shareholder actually benefited from the fund’s sale of underlying securities, the shareholder will receive the capital gain distribution if the mutual fund is held as of the dividend record date.

Mutual fund families typically provide estimates for year-end dividend distributions over the course of October and November, with such distributions most commonly paid in December.

Capital gain distributions can be either short-term or long-term. Short-term capital gain dividends are treated as ordinary income and thus cannot be offset by realized losses. In contrast, long-term capital gain dividends are treated as capital gains and can be offset by realized losses.

It is important to review unrealized gains and losses across mutual fund holdings in taxable accounts and to compare those figures against capital gain distribution estimates to determine if selling a mutual fund position before the year-end distribution would produce a tax savings.

Make Annual Exclusion Gifts

Taxpayers with assets in excess of the federal estate exemption should consider making annual exclusion gifts ($15,000 per person for 2019 and 2020), which do not count against the exemption amount.

In addition, payments for tuition and medical expenses made directly to the educational or medical institution do not constitute gifts. Utilizing annual exclusion gifts as well as direct payments for tuition and medical expenses can be beneficial for high net worth individuals as it effectively reduces the size of a taxable estate.

Additional Planning Considerations

Leveraging the Increased Estate & Gift Tax Exemption

In late November, the Treasury Department and Internal Revenue Service issued final regulations that taxpayers taking advantage of the increased estate and gift tax exclusion amount from the Tax Cuts and Jobs Act would not be adversely impacted after 2025 when the exclusion is scheduled to revert to pre-2018 levels. Previously, there had been some question as to whether the IRS might apply a “clawback” for taxpayers utilizing the higher lifetime gifting exemption, should the estate exemption in the future fall below current levels.

In light of the recent IRS notice and clarification, individuals with assets well in excess of the “applicable exclusion amount” ($11,400,000 per person for 2019, $1,580,000 as of 2020) might consider gifting additional assets to loved ones prior to 2026. Should the estate exemption revert back to a $5,000,000 base amount in the future, gifting assets now out of an otherwise taxable estate could yield significant estate tax savings.

Keep in mind that gifts in excess of the annual gift exclusion – currently $15,000 per person – should be properly documented in a gift tax return.

Filing for Social Security Retirement Benefits

Individuals nearing eligibility for Social Security retirement benefits should give proper consideration for when to start benefits. A recent study1 estimated only 4% of retirees start their Social Security benefits at the most optimal time, with retirees effectively forfeiting a collective $3.4 trillion in potential retirement income. A review of 2016’s new Social Security recipients2 showed nearly 60% of individuals collected benefits before their full retirement age (FRA), with only 10% waiting beyond full retirement age; nearly a third opted to begin receiving benefits at age 62 (the earliest one can collect) despite the significant benefit reduction. While general guidance is to wait until age 70, if possible, to collect a higher benefit, there are a number of important factors to consider: anticipated life expectancy, income needs for the interim years when benefits would be delayed, availability of spousal benefits, etc.

Contemplating a Change in State Residency

Changing your primary state of residency is not as simple as spending more than half the year in a new state. With many states more aggressively contesting such residency changes, individuals should take extra precaution to ensure “facts and circumstances” support the case for changing resident states. Some of the factors supporting a new domicile include:

- days spent in the new state for the year

- driver’s license registration, voter registration

- medical and dental care providers

- church attendance and membership, country club or social club memberships

- official mailing address to which mail and bills are sent, location of family heirlooms and artwork, etc.

1United Income, “The Retirement Solution Hiding in Plain Sight” (June 2019)

2“It’s Tempting to Take Social Security at 62. You Should Wait.” By Peter Finch. The New York Times. August 31, 2018.

These materials have been prepared for informational purposes only based on materials deemed reliable, but the accuracy of which has not been verified. Past performance is not indicative of future returns. These materials do not constitute an offer or recommendation to buy or sell securities, and do not take into consideration your circumstances, financial or otherwise. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision.