Aoifinn Devitt – Chief Investment Officer

The US CPI data for January was not exactly a sweet-smelling Valentine’s Day bouquet. Although it showed a seventh consecutive month of lower inflation than the previous month, it still came in above consensus expectations and confirmed that we are not “out of the inflation woods” yet. Some observers were concerned at the stickiness of certain core components, mostly related to services, while the persistence of a strong US labor market continued to stoke fears of more wage inflation to come.

Markets received the news in a subdued fashion, and the probability of further rate hikes increased, with the possibility of a higher terminal rate and ultimately a “higher for longer” approach by Central Banks around the world. Stocks initially fell in response but then stabilized, indicating that we don’t really have much in the way of new information now – six weeks in to 2023. We are back to worrying about the cocktail of higher inflation, higher interest rates and low unemployment – and the lack of a playbook to navigate it. It is almost like Groundhog Day, another February milestone that passed last week (although we failed to note it here).

A warmer than usual winter continued in parts of the US (not unwelcome here in Moneta’s Chicago office), while in Europe, the same weather phenomenon has taken much of the edge off there. As some of the strain around expected energy shortages has eased, energy prices have subsided and growth in the region has surprised on the upside. Companies that had been braced for margin pain could breathe a little easier, and consumers, too, came back from the brink. This is partly due to the fact that Europe continues to enjoy an unemployment rate at multi-decade lows. Despite this, however, according to economic surveys, consumer sentiment continues to be weak.

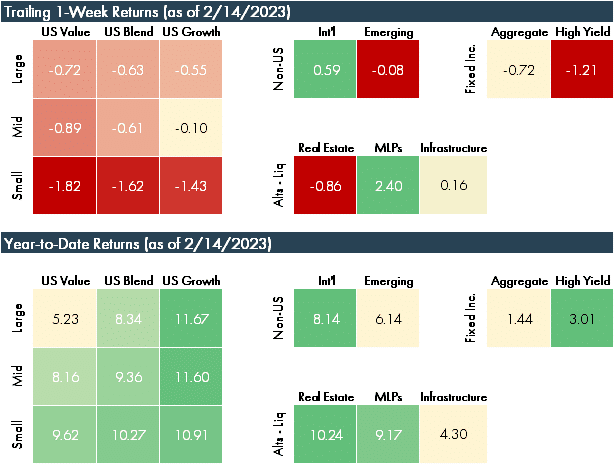

As earnings seasons wind down, the year-to-date numbers in markets look strong. Many commentators are scratching their heads as to why a broadly disappointing earnings season – particularly from tech stocks – did not get punished (the Nasdaq is up over 14% year to date). This period will now attract much analysis – some around what the downward trajectory of revenues will mean for margins and earnings in the months to come, and some around deciphering why investors are holding their nerve.

And, finally, this appeared yesterday in the European Central Bank’s Twitter account1:

Roses are red

Violets are blue

We will stay the course

And return inflation to 2

Who knew that Central Bankers had a sense of humor?

© 2023 Advisory services offered by Moneta Group Investment Advisors, LLC, (“MGIA”) an investment adviser registered with the Securities and Exchange Commission (“SEC”). MGIA is a wholly owned subsidiary of Moneta Group, LLC. Registration as an investment advisor does not imply a certain level of skill or training. The information contained herein is for informational purposes only, is not intended to be comprehensive or exclusive, and is based on materials deemed reliable, but the accuracy of which has not been verified.

Trademarks and copyrights of materials referenced herein are the property of their respective owners. Index returns reflect total return, assuming reinvestment of dividends and interest. The returns do not reflect the effect of taxes and/or fees that an investor would incur. Examples contained herein are for illustrative purposes only based on generic assumptions. Given the dynamic nature of the subject matter and the environment in which this communication was written, the information contained herein is subject to change. This is not an offer to sell or buy securities, nor does it represent any specific recommendation. You should consult with an appropriately credentialed professional before making any financial, investment, tax or legal decision. An index is an unmanaged portfolio of specified securities and does not reflect any initial or ongoing expenses nor can it be invested in directly. Past performance is not indicative of future returns. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.