One of the things that financial professionals have watched closely this year is the shape of the yield curve and, specifically, the flattening that has taken place. The yield curve illustrates the interest rates (or yields) of a series of bonds with equal credit quality (e.g., Treasuries), but different maturity dates. When short-maturity Treasuries have a similar yield to longer-maturity Treasuries, the yield curve is considered flat. In addition, under certain conditions, the yield curve can invert—an occurrence where short-maturity bonds have higher yields than longer maturities.

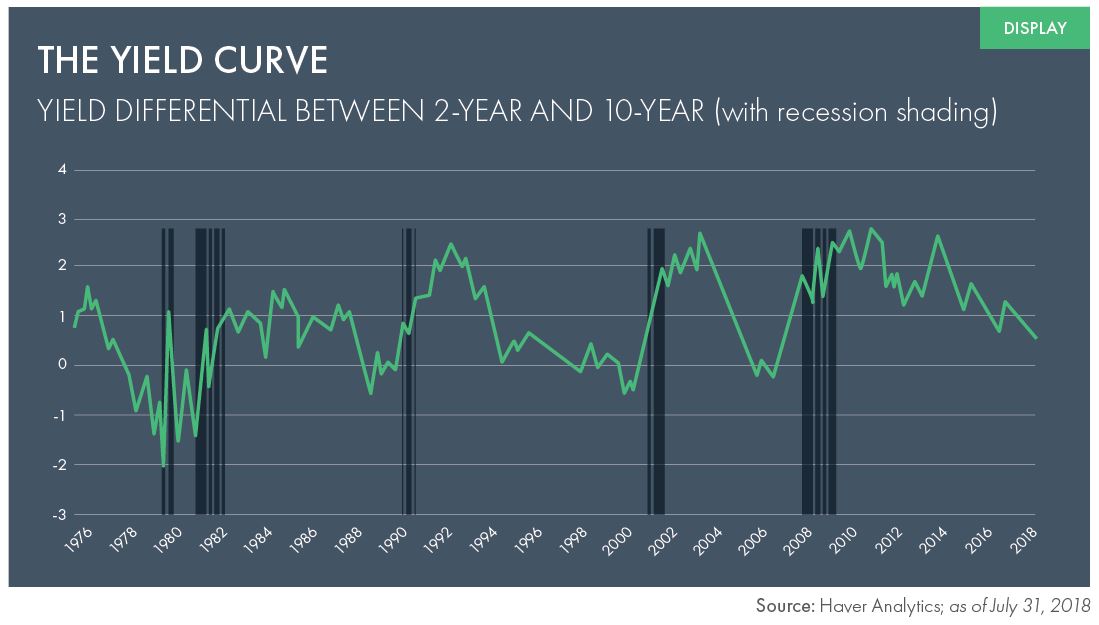

We’ve seen a pronounced flattening of the yield curve this year; for this piece we’ve defined the yield curve as the difference between 2-year and 10-year U.S. Treasury notes (Display). Yields have increased across the maturity spectrum, but shorter-maturity Treasuries have increased more than longer maturities. In early 2018, the yield curve had a positive slope of 78 basis points, and in recent sessions, it has traded as low as 24 basis points. Over the past five years, the slope has averaged 134 basis points and touched a high of 265.

The World’s Best Economist

The Treasury yield curve, in general, is often thought of as the world’s best economist. At any given point in time it reflects the views of all market participants on subjects such as liquidity, monetary policy, the economy, market sentiment and the future path of yields. The yield curve is regarded as one of the better economic indicators and, in fact, is one of the components of the leading economic indicators (LEI) that the Conference Board releases monthly. There are three commonly held explanations for the yield curve’s shape:

- Expectations Theory: Holds that the shape of the yield curve is purely a reflection of investors’ beliefs about the future path of bond yields. A steep yield curve indicates that investors have expectations of higher future rates, whereas a flat or inverted curve indicates lower future rate expectations.

- Liquidity Preference: Contends that yields on longer-term maturities are higher than those of shorter maturities. Known as a “term premium,” this differential is attributable to the principle that investors should generally receive compensation for the additional risk of holding longer-dated instruments.

- Market Segmentation: Explains the shape of the yield curve by the fact that different portions of the yield curve are impacted by different factors.

What Is the Yield Curve Saying Today, and Is It Relevant?

First, a brief history lesson. Prior to the Global Financial Crisis, the yield curve (2-year vs. 10-year Treasuries) inverted in early 2000, 1989, 1982 and 1980, and each time was followed by a recession. The yield curve also spent much of 2005 and 2006 slightly inverted, and the stock market peaked roughly a year later in late 2007 before the 2008-2009 financial crisis.

Estrella and Mishkin, two researchers from the U.S. Federal Reserve (the Fed), published a study in 1996 that concluded that the yield curve is a powerful predictor of a recession two to six quarters in advance. In fact, they found that the greater the inversion the higher the probability; however, their model currently puts the probability of a recession based solely on the shape of the yield curve at less than 20%. Another research study from the San Francisco Fed indicates every recession of the past 60 years has been preceded by an inverted yield curve.

While it is just one indicator, we believe the yield curve’s shape is reasonably explained by the market segmentation theory:

- Short-maturity Treasuries are being impacted by the Fed’s actions to date (notably seven increases in the

target fed funds rate) and rhetoric indicating more to come. - Longer-maturity Treasuries reflecting low global yields, a relatively benign inflation outlook and a desire for safe,

long-duration assets.

This theory will be the one to watch, even though it may shift due to the Fed’s multifaceted rate normalization process, which could take time to implement after years of zero-percent interest rate policy.

We will continue to monitor the yield curve as one leading indicator and will close with one additional, semi-rhetorical thought and a question: If bond yields were heavily influenced by the Fed’s extraordinary monetary policy in what some would call an almost irrational fashion, why would the path to normalizing rates be any different? Food for thought as we closely watch the spread between short- and long-dated bonds.

Bill Hornbarger | Chief Investment Officer

These materials were prepared for informational purposes only and were developed based on sources deemed to be reliable. These materials are subject to change at any time without notice. The information contained herein does not take into account your individual circumstances, financial or otherwise, and this is not an offer or recommendation to sell or purchase securities. Past performance is not a guarantee of future return. You should consult with an appropriately credentialed professional prior to making any investment related decision.