By Aoifinn Devitt | Chief Investment Officer

Highlights

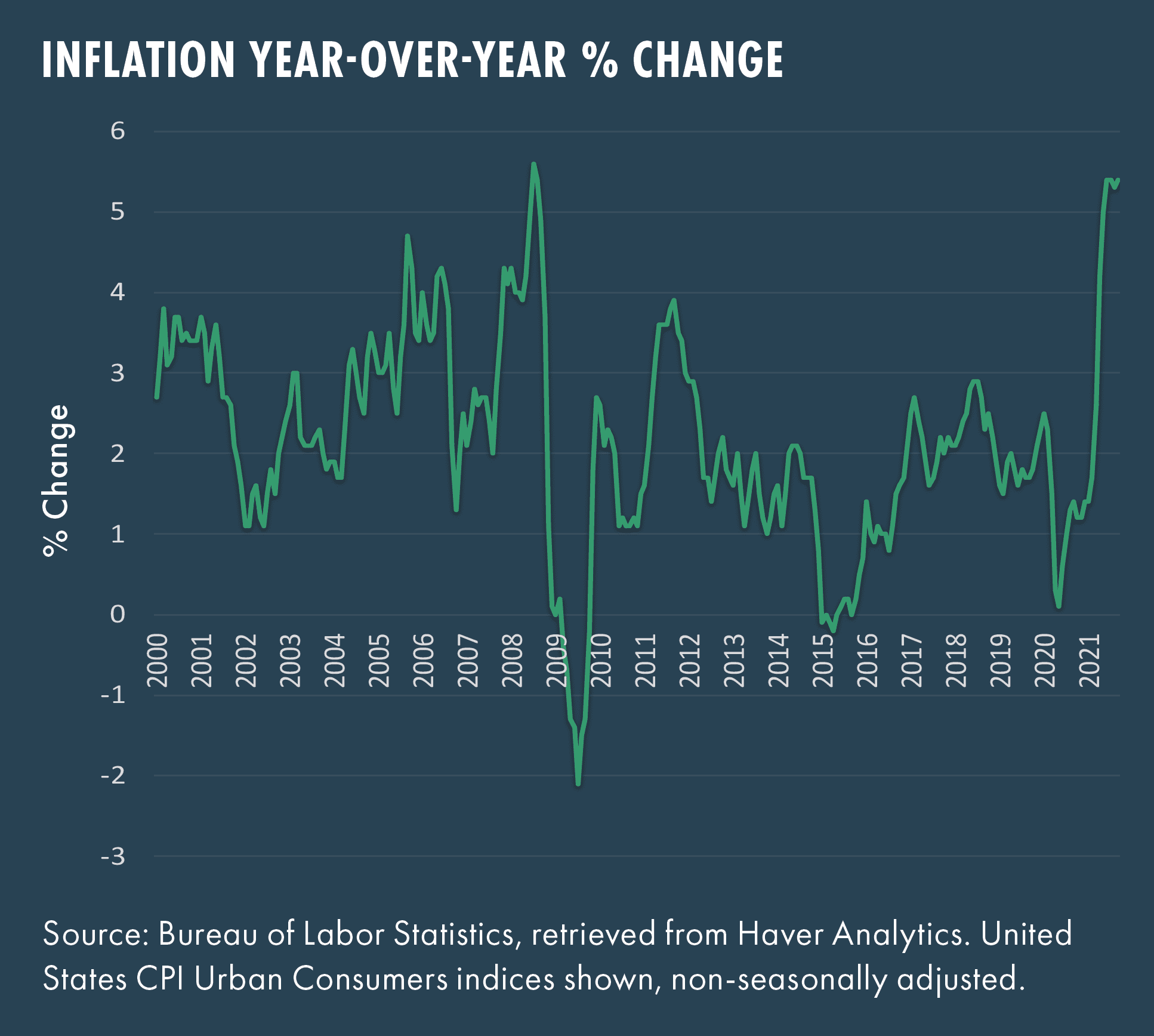

- The third quarter was dominated by talk of inflation as the September Consumer Price Index (CPI) showed a 5.4% increase from September 2020, representing a 13-year high(1). These sowed further seeds of doubt that the current inflationary wave was indeed “transitory.” Among the key drivers of the higher price level were higher energy costs, which were partially impacted by Hurricane Ida’s effect on Gulf production, the Organization of Petroleum Exporting Countries (OPEC) holding back increased production and ongoing supply constraints leading to increased shipping costs.

- Markets faltered in September, which resulted in a 0.58% return for the S&P 500 in Q3 2021. Non-US markets, particularly Emerging Markets, were negatively affected by ongoing surprise regulatory change out of China. Within the US, on a sector basis, financials and utilities outperformed while industries and materials struggled. While almost all sectors underperformed in September, energy was an exception as ongoing supply constraints drove oil prices to recent highs.

- Expectations for interest rates were little changed over the month, although the Fed has slowly de-emphasized its conviction that inflation is “transitory” and appears to be still on track to taper their bond-buying program. They are expected to reduce their purchases by $15 billion a month until no purchases are made by mid-2022, although interest rate rises are not likely until the end of 2022. Fixed income returns remain muted. With the current levels of inflation, many bond issues are delivering a negative yield after inflation is considered.

- Supply chains have been the focal point for many businesses as constraints and elevated costs in shipping have created issues. For example, according to the Freightos Baltic Index, the cost to ship a 40 ft. container from China to Los Angeles has increased 363% since the beginning of the year to nearly $18,000. Increased demand alongside decreased supply could see those costs passed on to end consumers.

Macro Stories

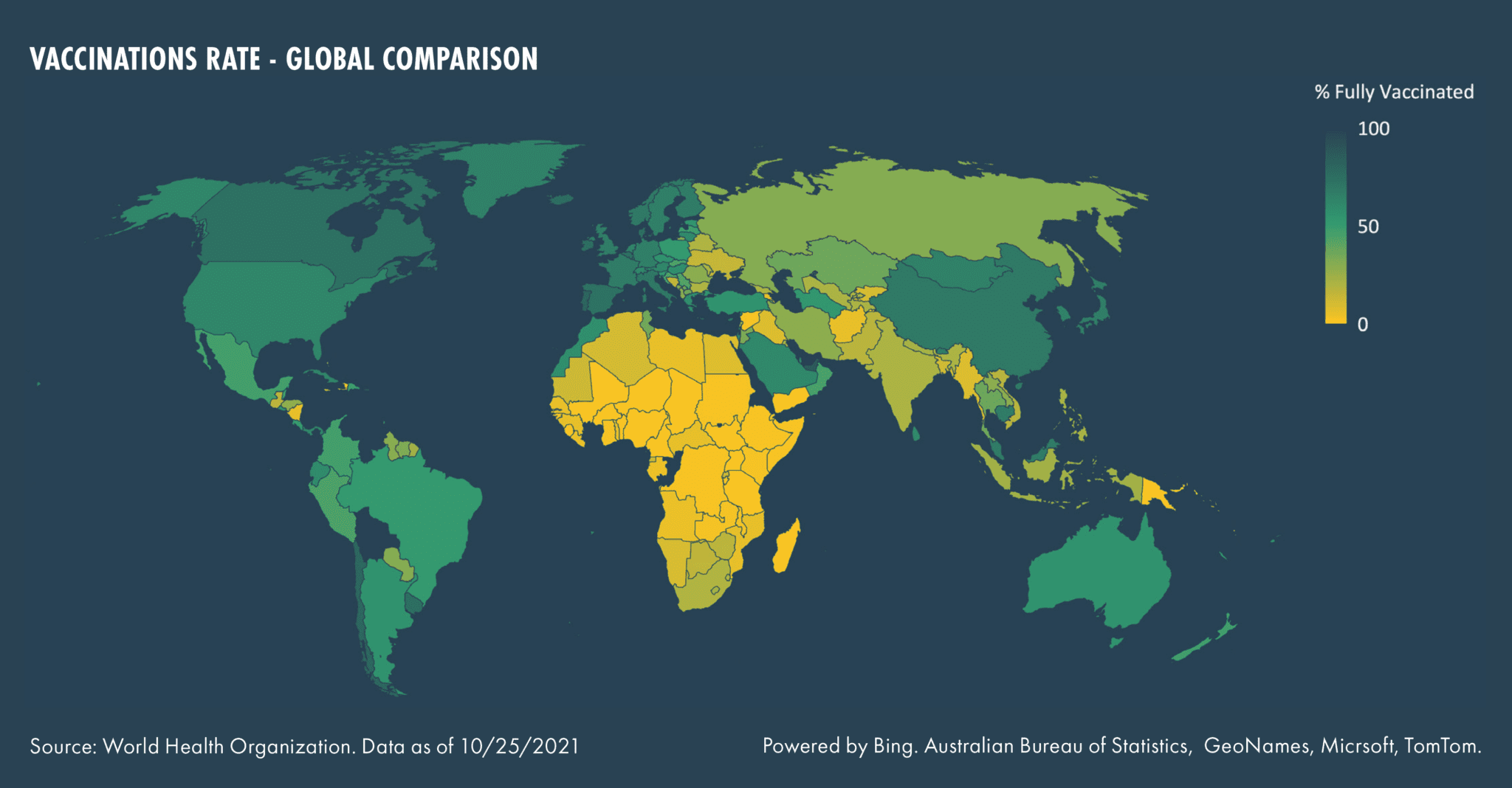

The summer continued the narrative of economies and GDP growth clawing their way out of the Covid-19 induced slump as vaccination levels continue to tick upwards globally (with the notable exception of the African continent). This has proven in the past to be the key to expectations of full economy re-openings, but the disparity in evidence regionally does suggest ongoing divergence in recovery rates between developed and emerging markets.

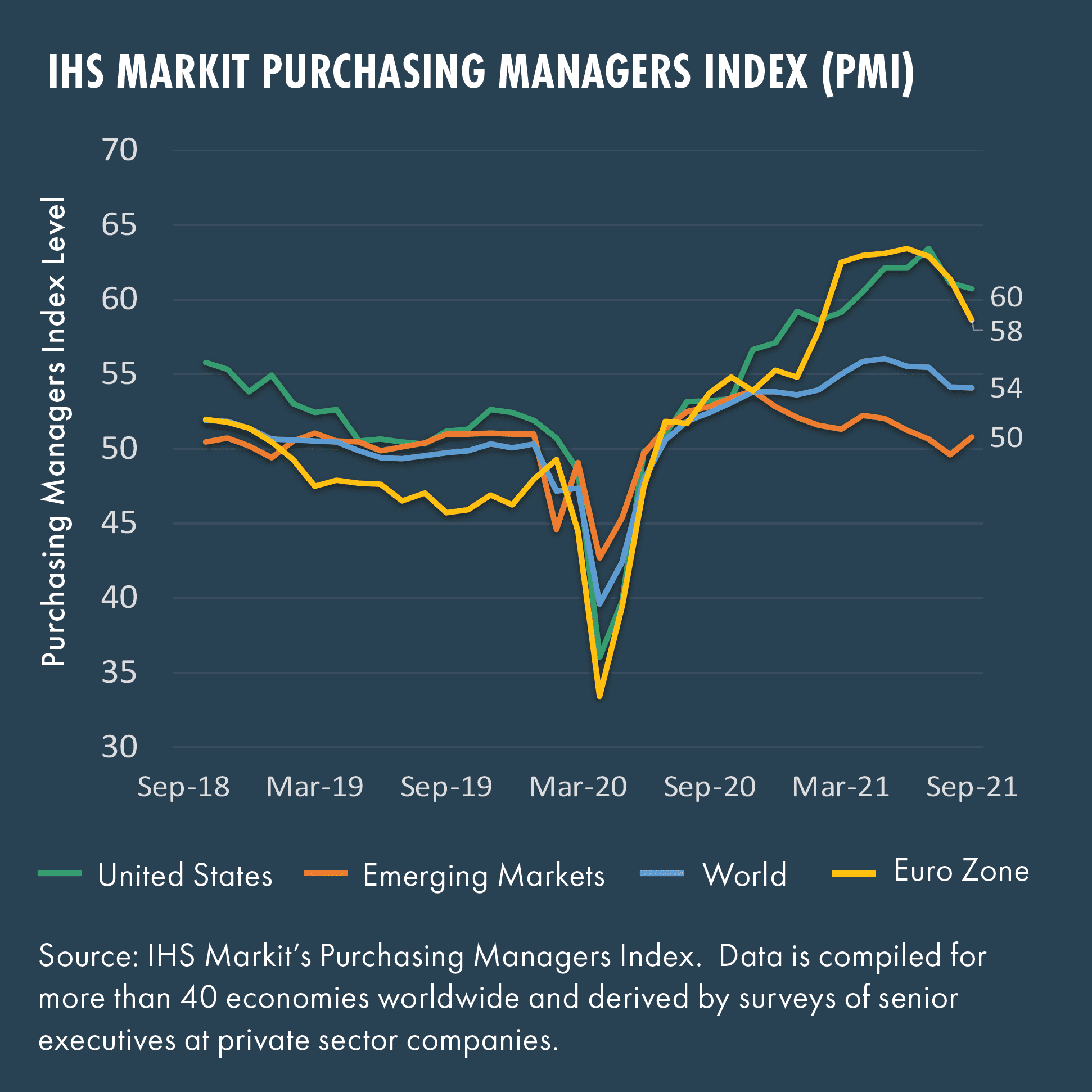

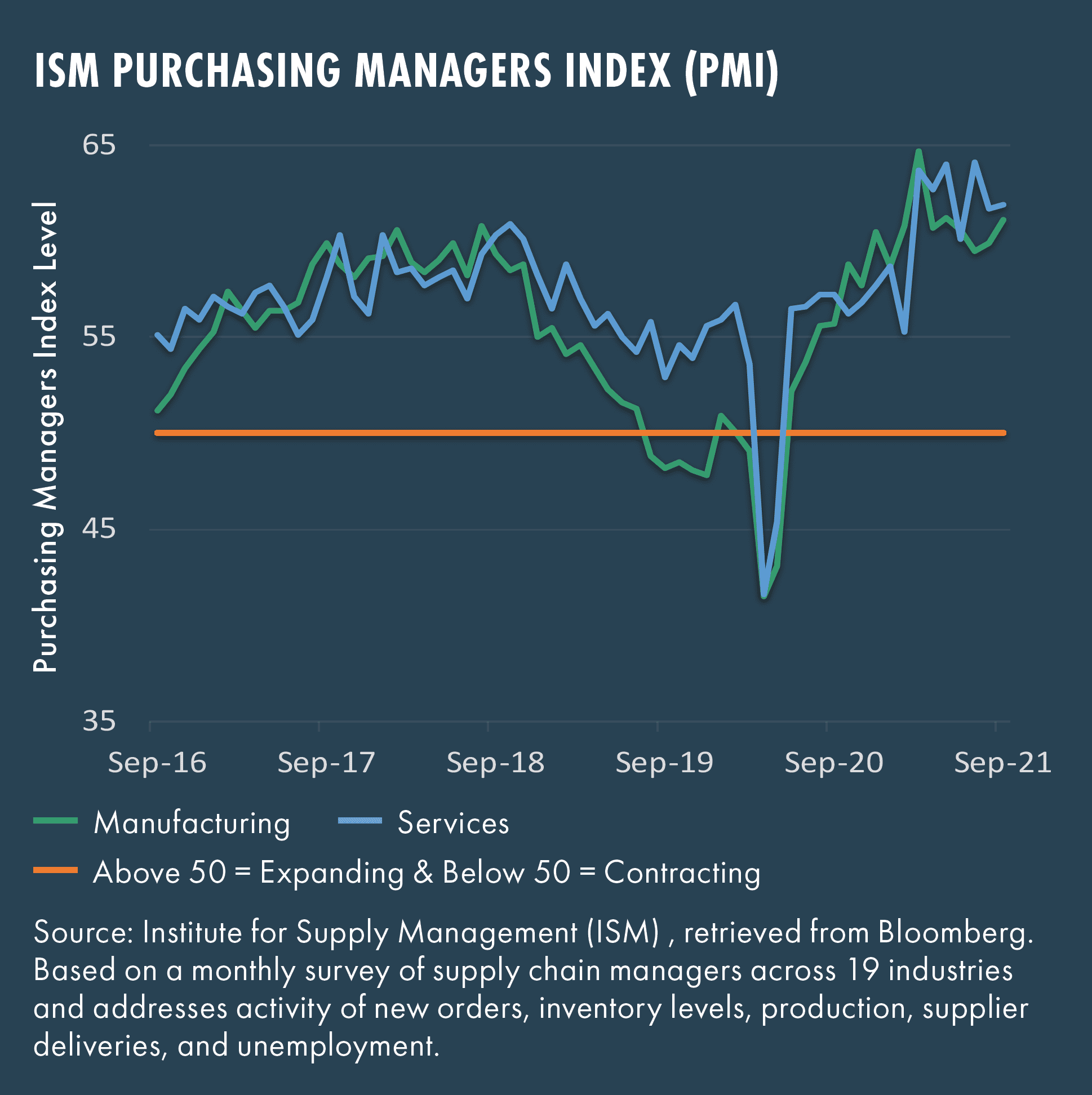

As the graphs below show, sentiment as measured by the Purchasing Managers Index has been somewhat volatile in the past few months.

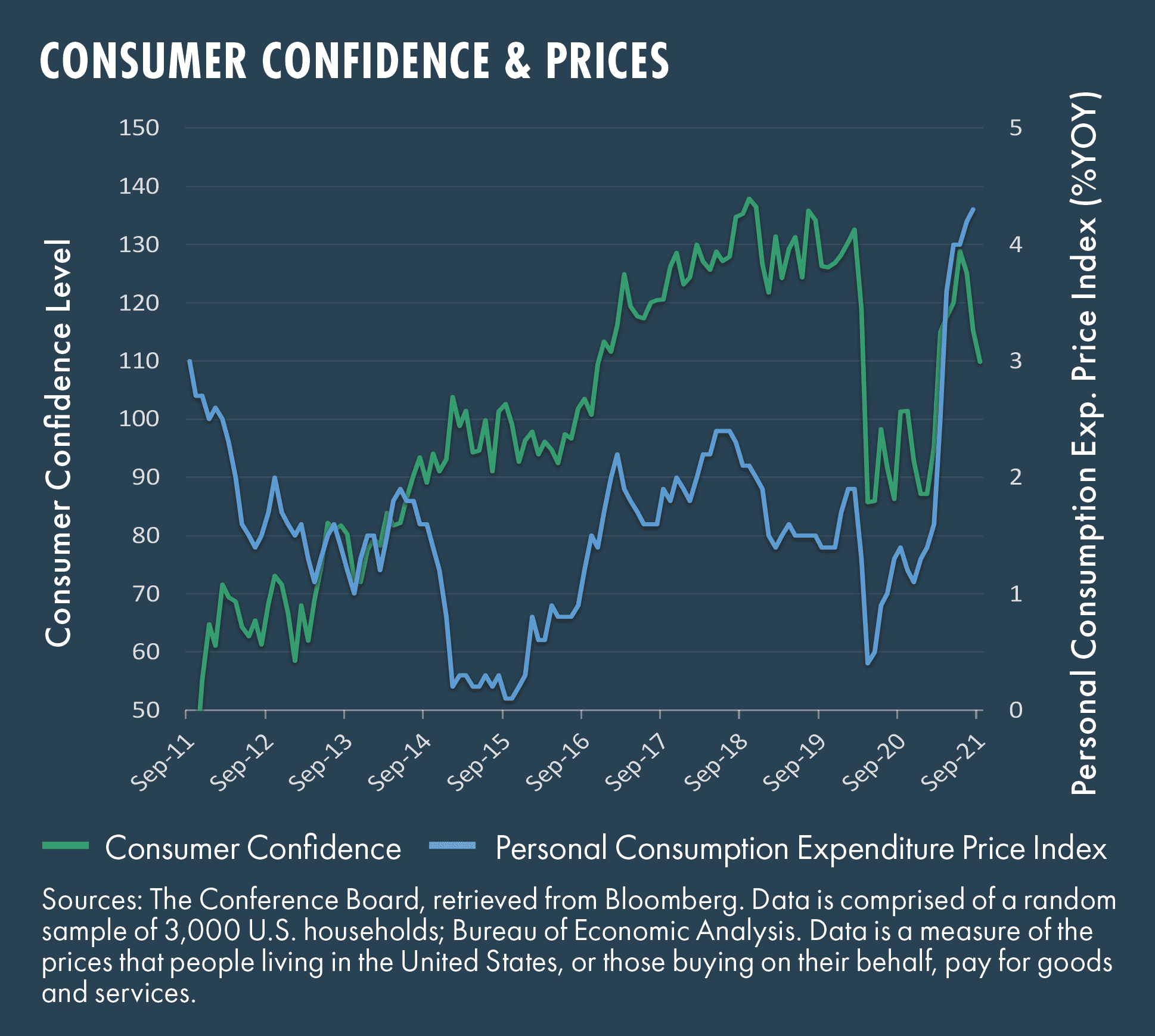

Consumer confidence remains similarly buoyant, although it has faltered occasionally in the last few months. Meanwhile, consumption is resilient, adding further fuel to inflationary pressures and accentuating some of the shortages currently plaguing certain supply chains.

The inflation levels reported over the summer touched highs not seen since 2008.

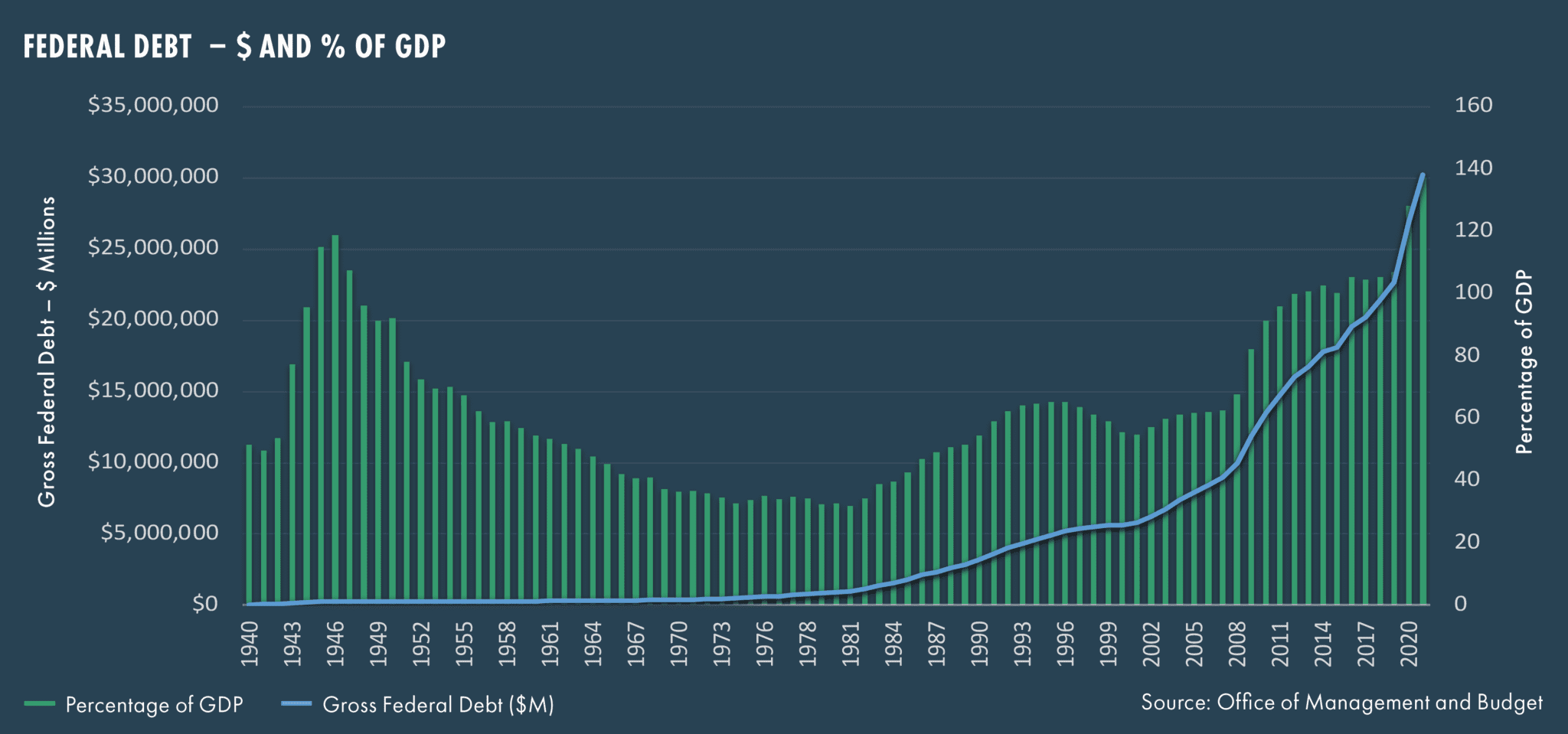

This all sits against a backdrop of rising government debt levels, which are regarded for some as a bearish indicator of a coming period of economic strain. As the chart below shows, the level of gross federal debt is rising starkly in both nominal terms and as a percentage of GDP; but this rise is probably somewhat distorted by the slump in GDP in 2020, and we can expect it to moderate as GDP recovers and returns to its previous levels of growth. The evidence of only muted market reaction to the raising of the debt ceiling and possible default does suggest, though, that markets are not too focused on these metrics. They seem to have faith that default will be avoided and debt levels will not jeopardize the narrative of the economic recovery.

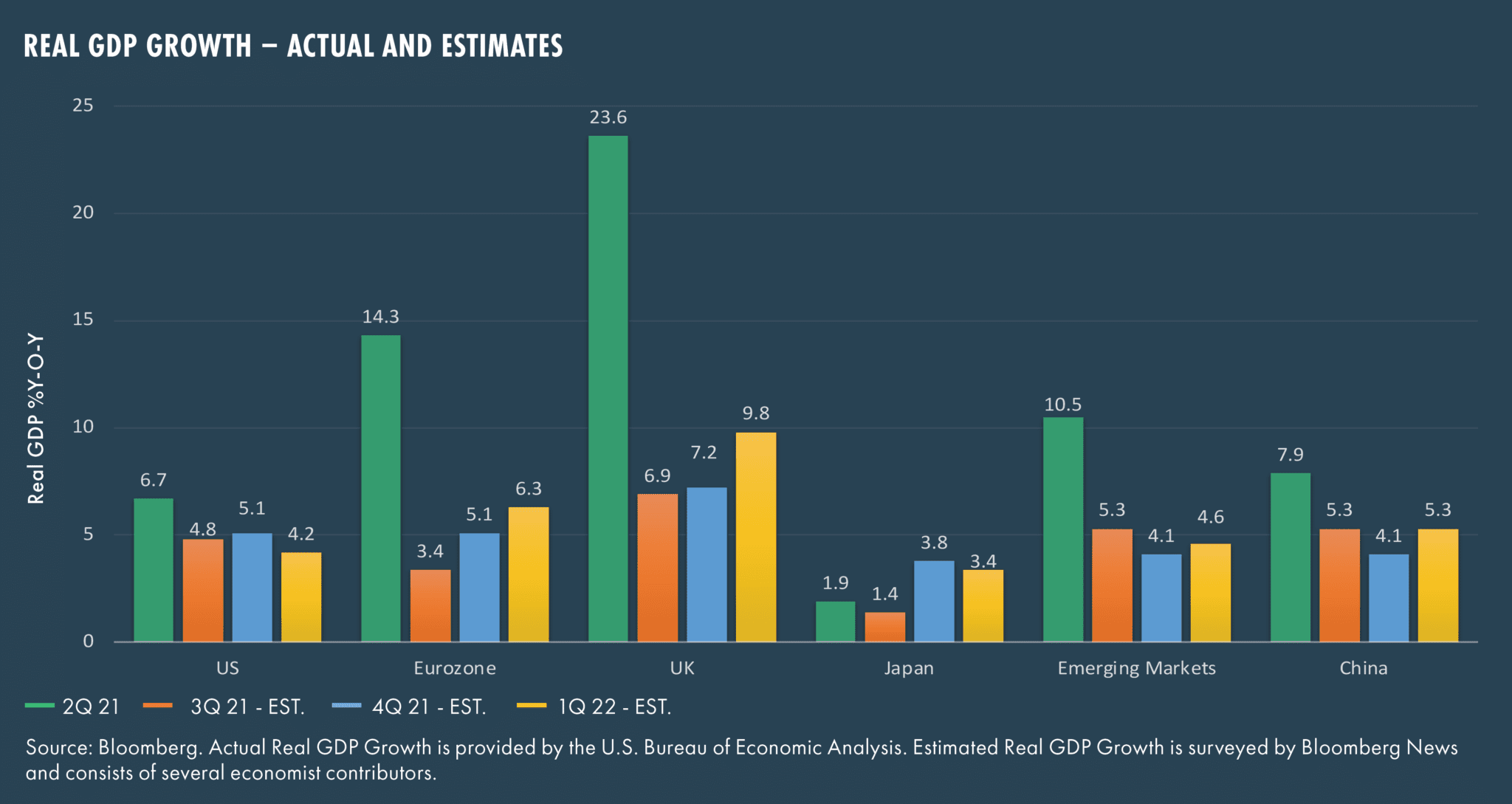

As the charts below show, real GDP remains in recovery mode globally, with all regions expected to show positive performance to year end – albeit more muted than the sizeable spike in the second quarter of this year.

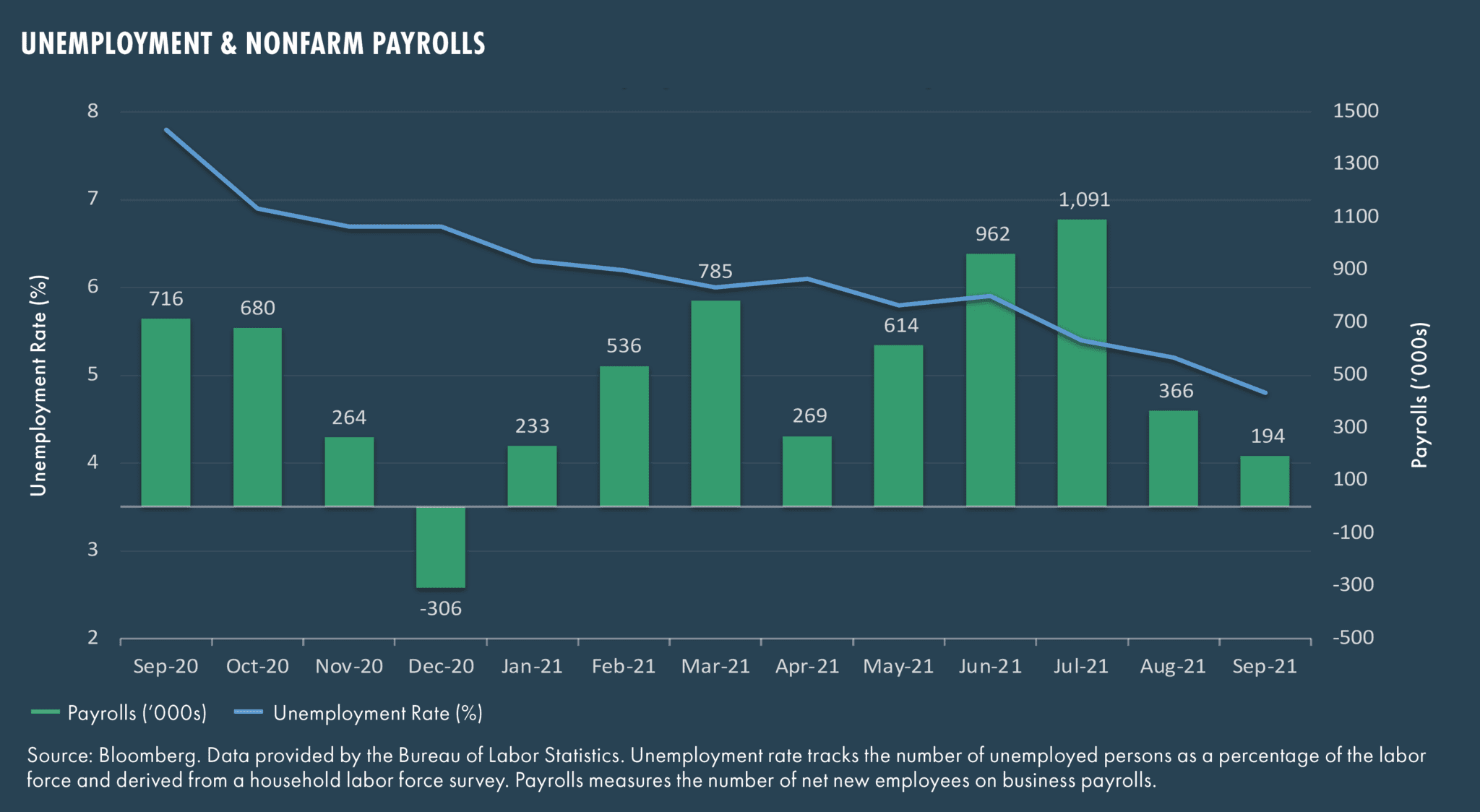

US unemployment continues to track downwards, although the monthly payrolls number has been less easy to predict given the unclear effects of lower workforce participation amid prolonged Covid disruptions.

China and Emerging Market performance lagged over the quarter as international investors reeled from surprise regulatory initiatives by Chinese regulatory authorities to curtail the business models of private education companies and video game manufacturers as limits on access were implemented. The default of Evergrande, the largest Chinese real estate developer, sent shockwaves through markets, which elevated expectations for a cascade of further defaults from other real estate developers and credit providers.

Energy prices remained firm over the quarter. With winter approaching, fears of supply constraints and even higher prices manifested in consumers panic buying fuel in countries such as the UK and price spikes globally, particularly in the case of natural gas. This had immediate ramifications for factories that depend on natural gas for input as well as energy supply companies. The quarter saw several factory closures in the UK as well as energy company bankruptcies. In the US, energy prices, together with the rising price of labor, looked poised to squeeze company margins – although, the backward-looking earnings revealed so far remained relatively robust, and margin squeezes did not yet seem to be significant.

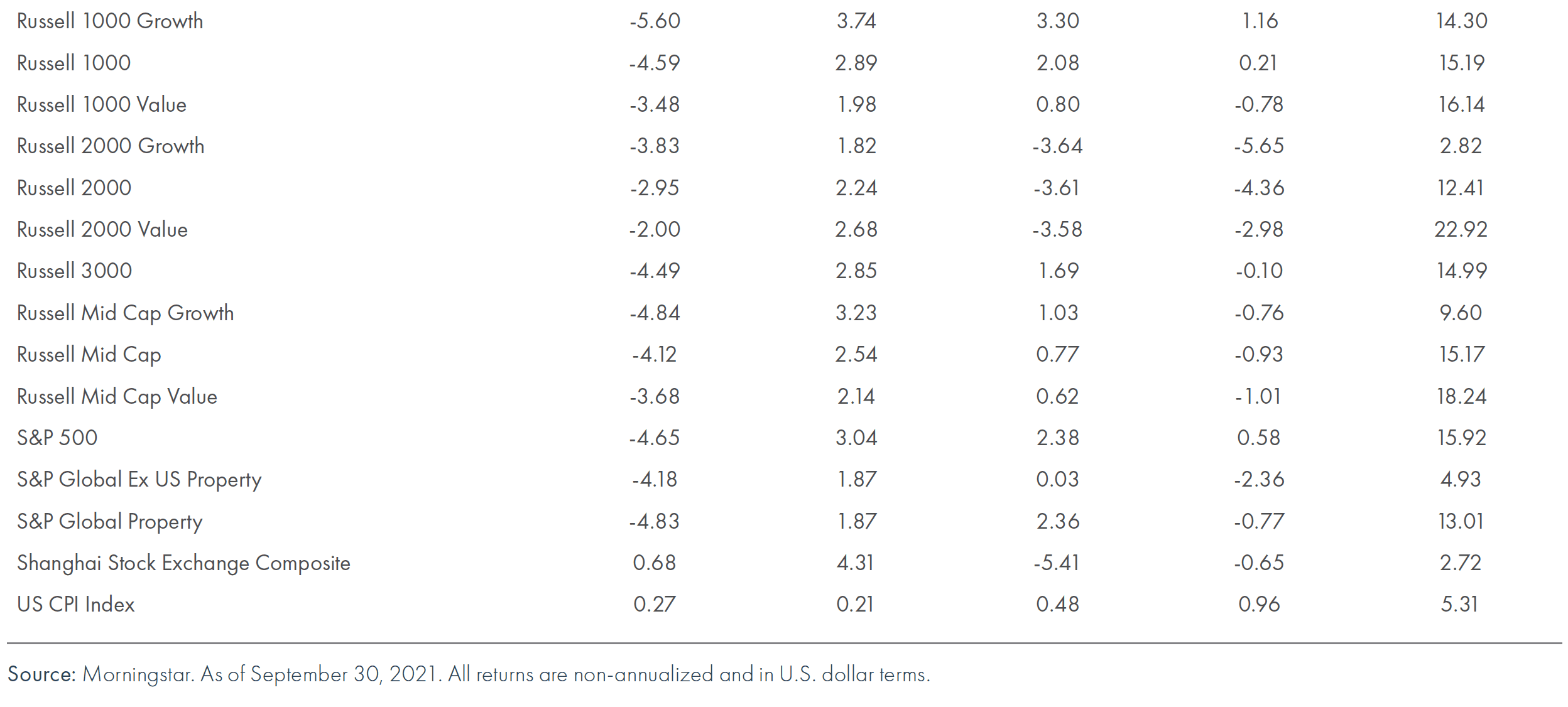

Asset Class Performance

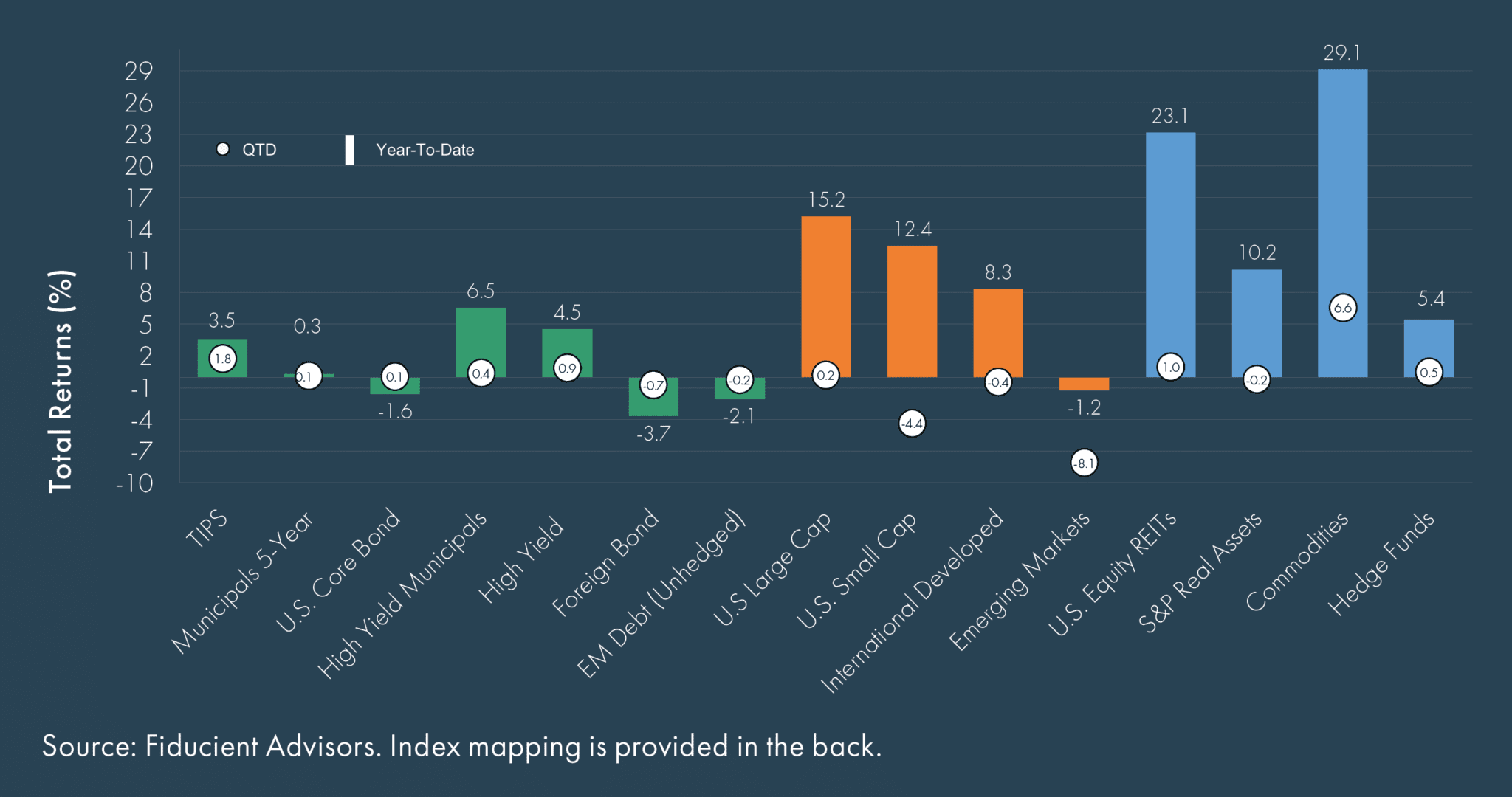

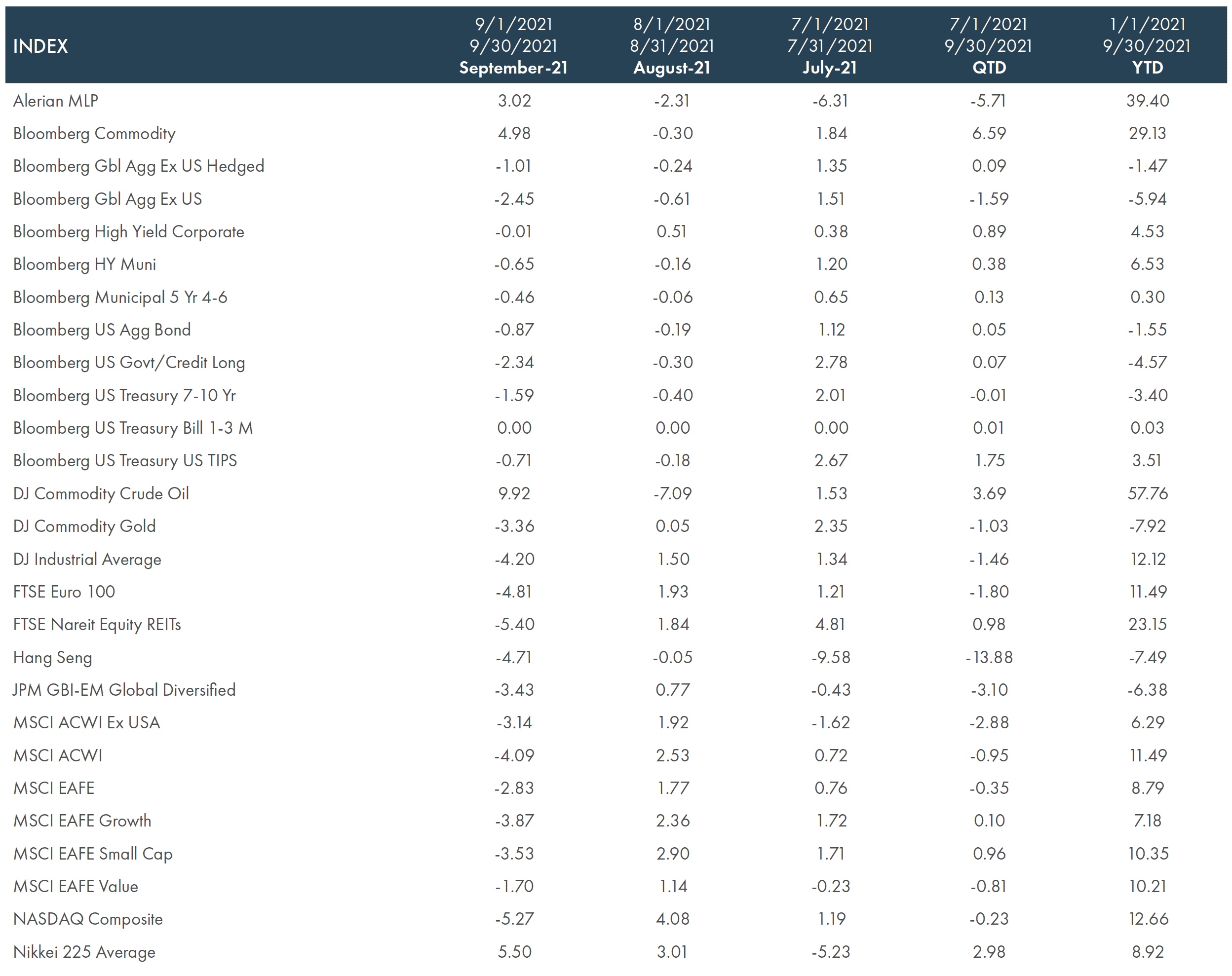

The third quarter was lack-luster for asset returns as the chart below shows, with every asset class in either flat to slightly negative territory except for US equity REITS (+1%), Commodities (+6.6%), US Small-Cap Equities (-4.4%) and Emerging Markets (-8.1%). This quarterly number marks reasonable intra-quarter volatility. Most US indices made significant gains in July and August – as sentiment was buoyant during the summer months – only to see September undo all of the gains.

The Alerian MLP index lost 5.7% on the quarter, which is unusual given the strength in energy indices. This must be read in the context of its 39.4% year-to-date return.

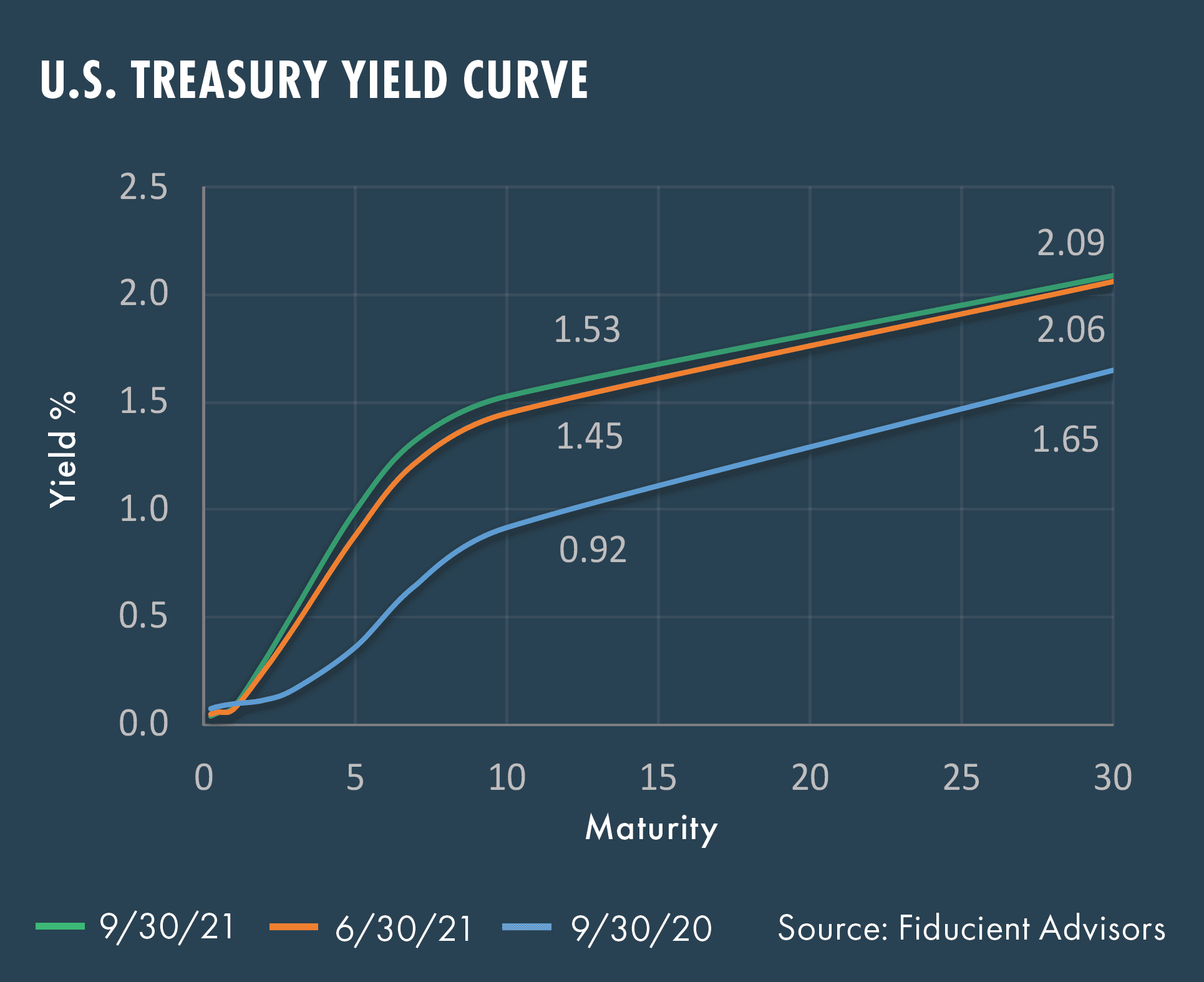

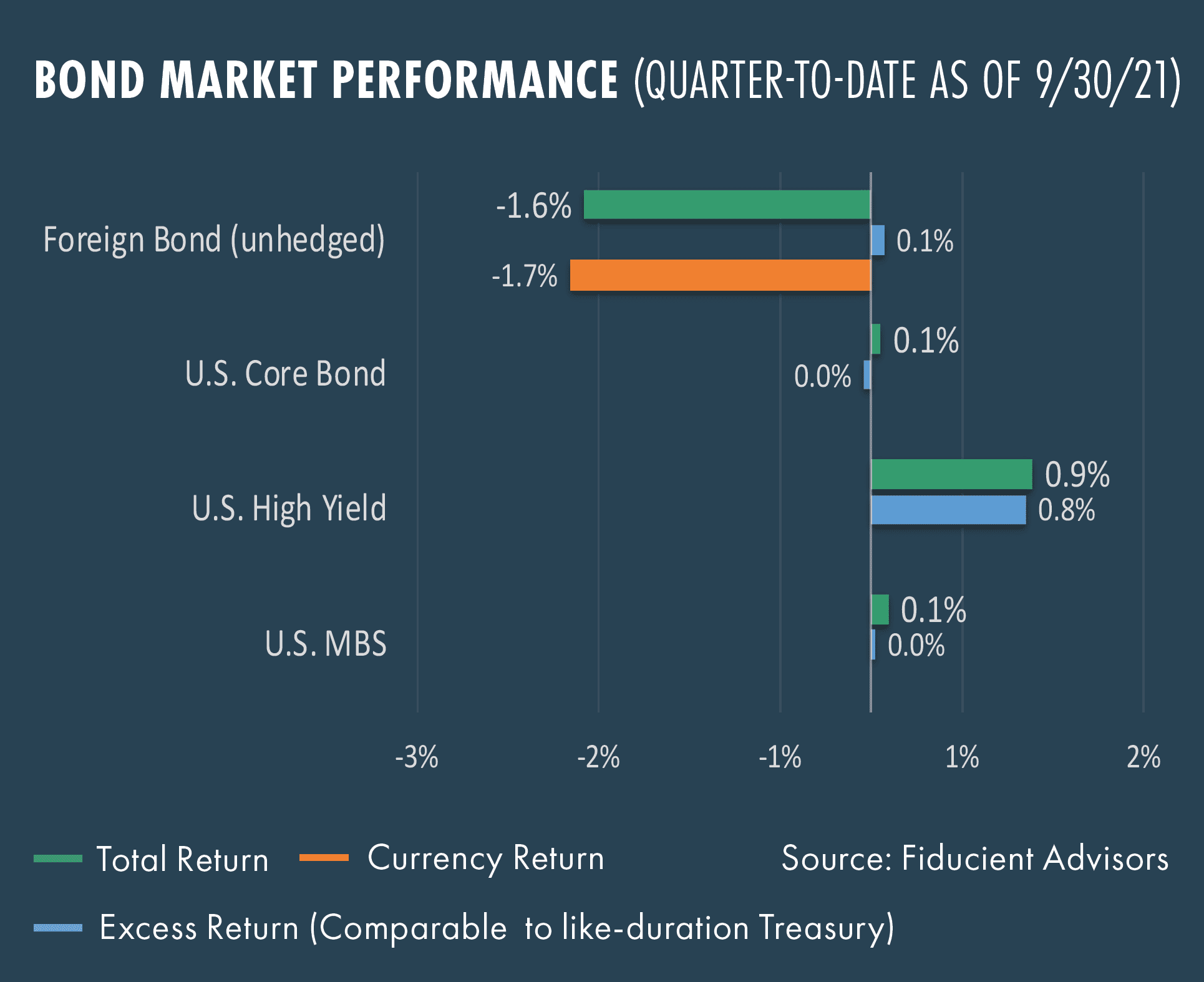

Moving to fixed income, per the chart below, the US Treasury yield curve was slightly flatter by the end of the quarter, indicating expectations of a shorter time frame until rate increases, but a slightly more lackluster long-term outlook. Yields overall are higher than the mid-point of 2020 – as we might expect with more risk appetite in evidence – but still low by historical standards. Overall, the quarter was a flat one for the fixed income asset class with core bonds eking out a very modest return and high-yield returns just shy of 1%. With the persistent strength in the dollar, non-US dollar denominated bonds continued to suffer from currency declines.

Outlook

- As we write, political maneuvering persists around the two elements of the President’s Build Back Better agenda: the $1 trillion infrastructure deal that has bipartisan support and the spending bill that is still to be determined. Markets seem to be unmoved by these developments for the most part, although the specter of a debt default did briefly lead to some market jitters in mid-September.

- Earnings season is in full flow as we write, and earnings have surprised on the upside to date. As of October 28, about half of the S&P 500 companies have reported earnings with 82% beating expectations. With banks reporting strong trading and M&A volume, the essential scaffolding of commerce appears to be intact and this has boosted confidence in the economic recovery. As we move towards the end of the year, we will continue to focus on earnings, the effect that rising costs and supply chain pressures have on margins, consumer demand over a more open holiday season than last year’s and whether the buoyant equity market returns will lead to some profit taking by year end.

- Internationally, representatives from more than 195 nations will gather to discuss policy changes to address the threat of climate change at the UN Conference of the Parties in Glasgow on October 31(COP26). We can expect to see the further promotion of renewable energy investments, renewed focus on a net-zero carbon target and the generation of more incentives around “green finance.” On a global level, we can expect shareholder pressure on companies to intensify – leading to enhanced decarbonization initiatives and commitments to the energy transition away from fossil fuels. Continued investment in these initiatives is likely.

Asset Class Performance

1. https://www.aljazeera.com/economy/2021/10/13/pain-in-the-wallet-us-inflation-hits-another-13-year-high

©2021, Moneta Group Investment Advisors, LLC. These materials have been prepared for informational purposes only based on materials deemed reliable, but the accuracy

of which has not been verified. Past performance is not indicative of future returns. You cannot invest directly in an index. These materials do not constitute an offer or

recommendation to buy or sell securities, and do not take into consideration your circumstances, financial or otherwise. You should consult with an appropriately credentialed

investment professional before making any investment decision.